Trading¶

Exchanges Today¶

Modern financial exchanges are typically electronic communications networks or ECNs.

- They consist of large warehouses, populated by computer servers that electronically match orders.

- These are referred to as matching engines.

- Since order execution speed is so important, many traders co-locate their trading computers with the matching engines.

Major U.S. Exchanges¶

- The NYSE Arca matching engine is located in Mahwah, NJ.

- The Electronic Broking System (EBS) currency exchange is located in Secausus, NJ.

- The Chicago Board Option Exchange (CBOE) has co-located with EBS in Secaucus.

- The Nasdaq matching engine is located in Carteret, NJ.

- The CME Group matching engine is located in Aurora, IL.

Exchanges Today¶

Exchanges Today¶

Exchanges Today¶

Market Makers¶

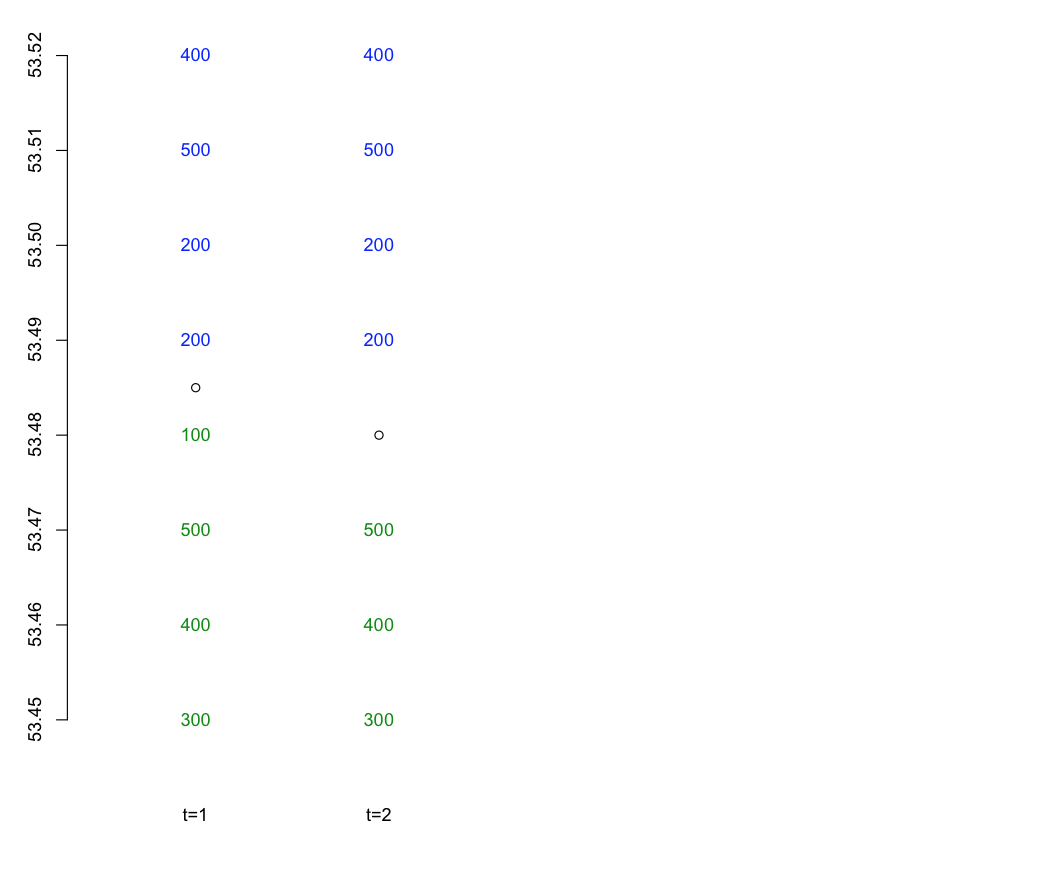

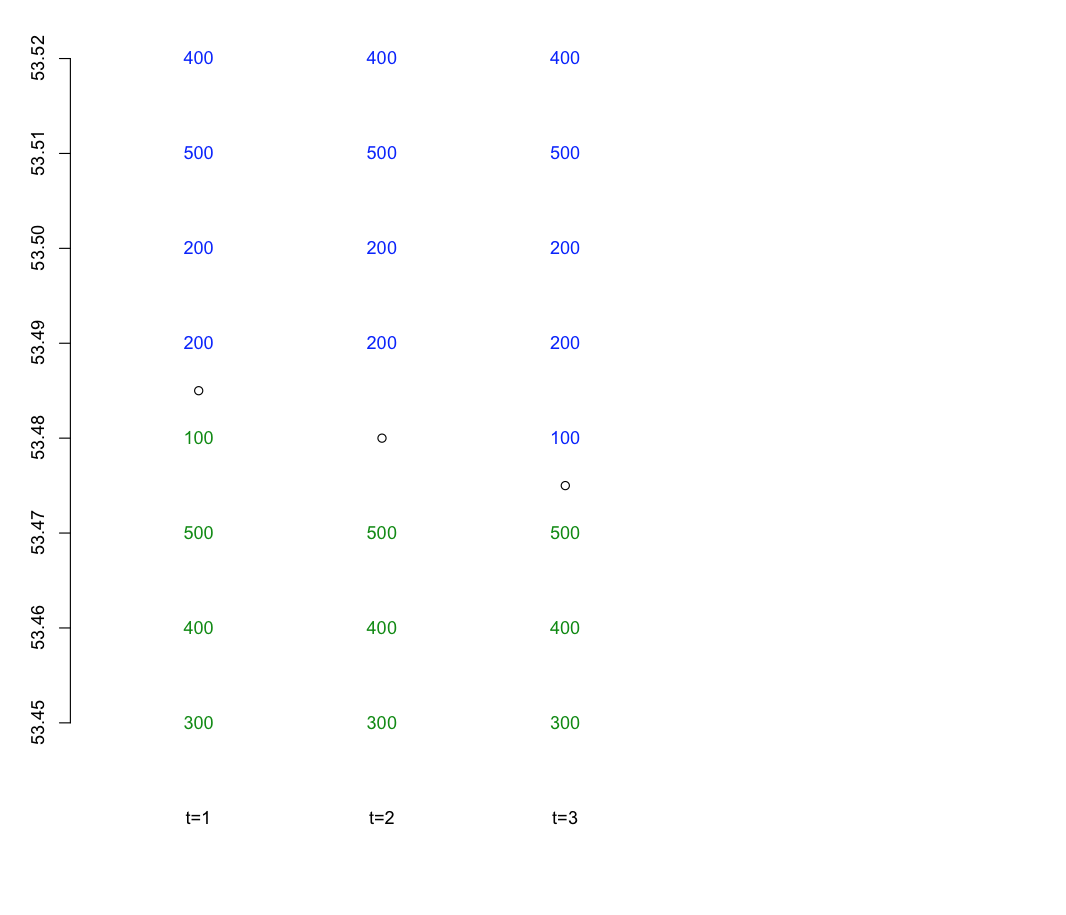

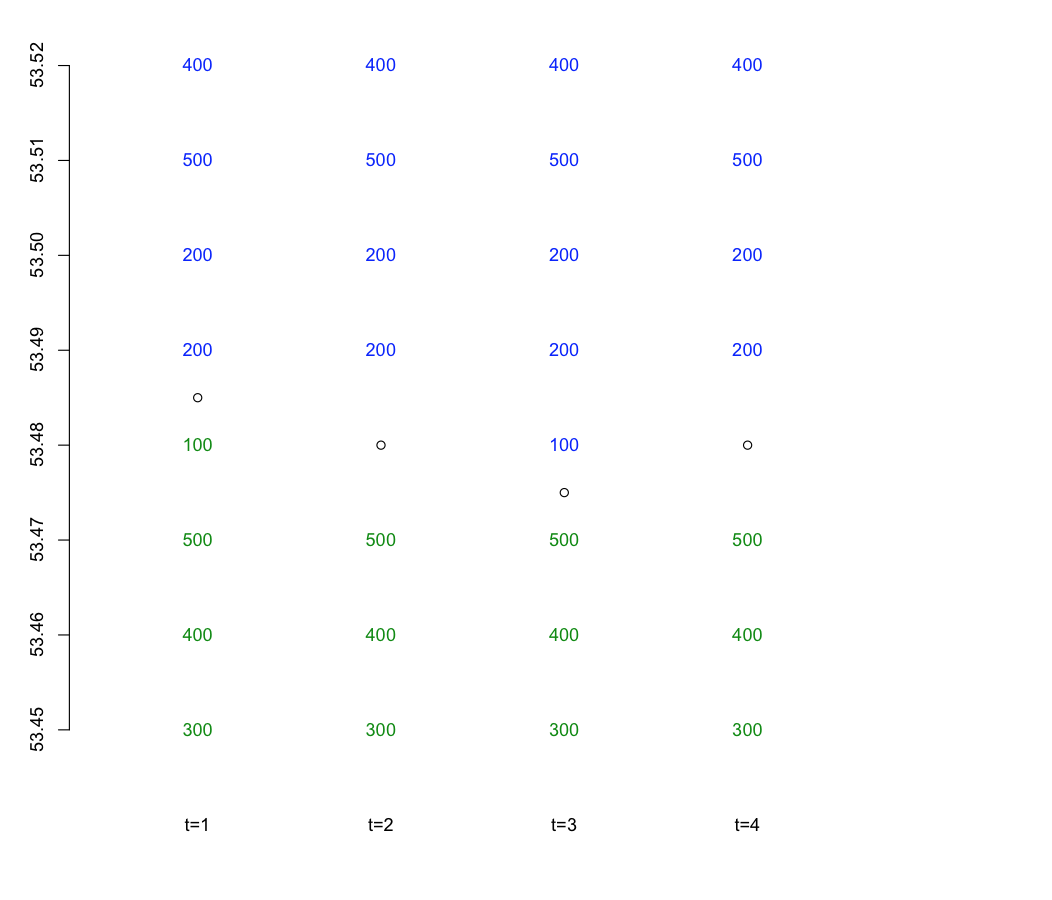

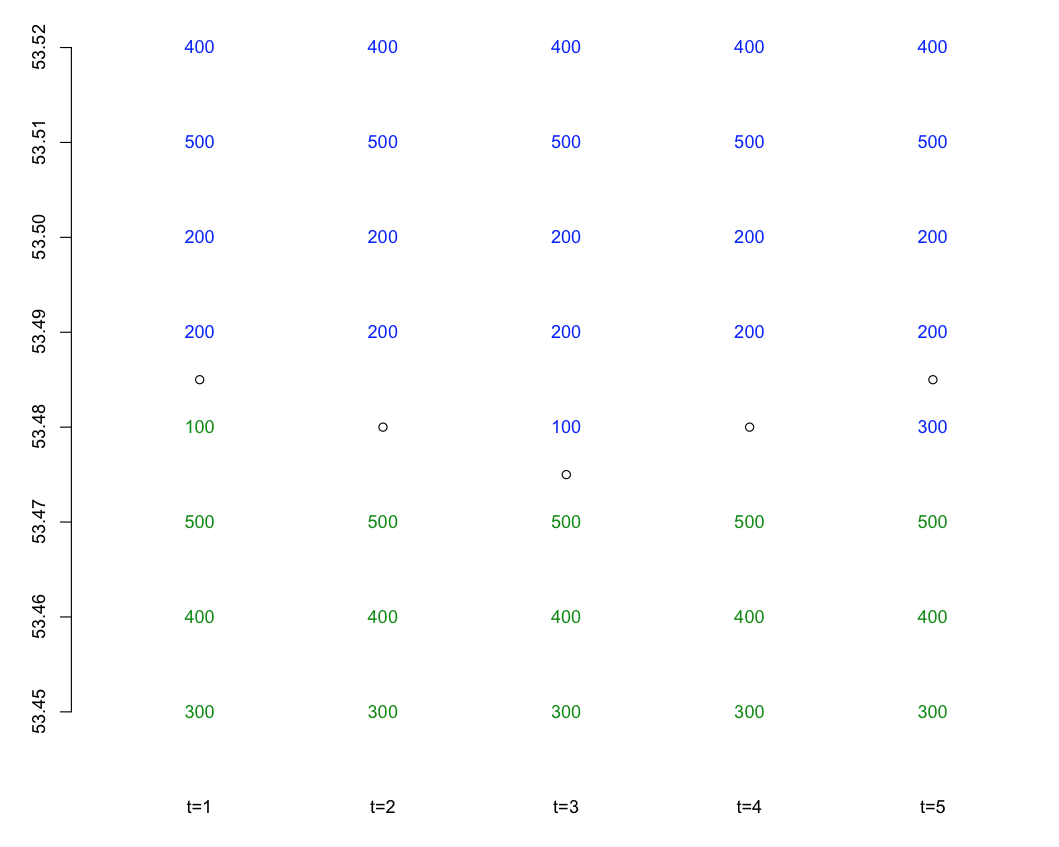

Participants on exchanges include makers and takers.

- Makers are required to post both quotes to buy and sell assets on the exchange.

- Quotes to buy are called bids.

- Quotes to sell are called offers.

- Typically there are many bids and offers posted on the exchange at different prices.

- Market makers are compensated for providing quotes (also referred to as providing liquidity).

Takers¶

Takers actively take orders that have been passively posted by market makers.

- When a taker wants to buy the asset, they buy at the lowest posted offer quote.

- When a taker wants to sell an asset, they sell at the highest posted bid quote.

- The difference between the highest bid quote and lowest offer quote is known as the spread.

Order Book Example: time 1¶

Order Book Example: time 2¶

Order Book Example: time 3¶

Order Book Example: time 4¶

Order Book Example: time 5¶

Information Flows¶

Conventional wisdom is that information flows from the futures market to the equities (cash) market.

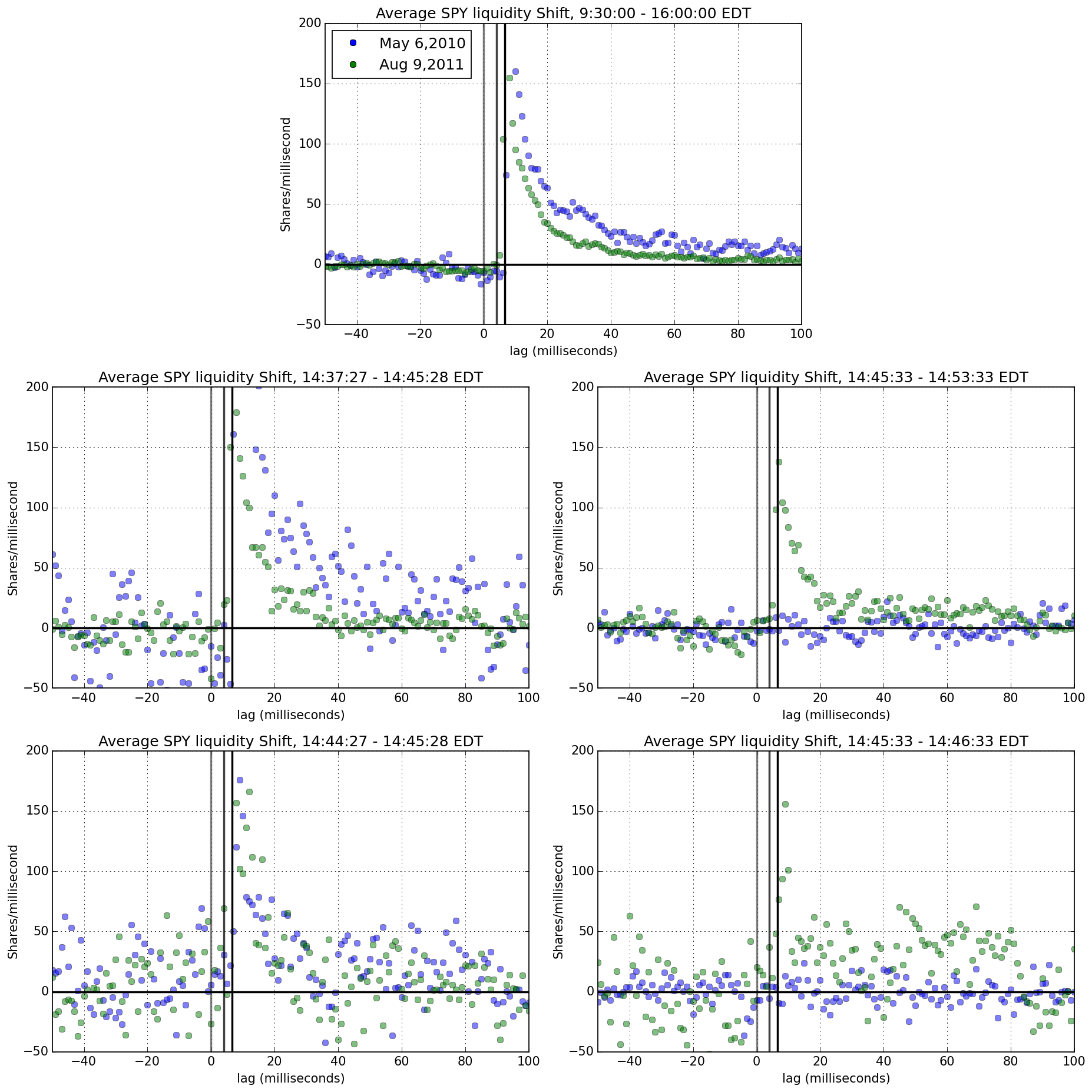

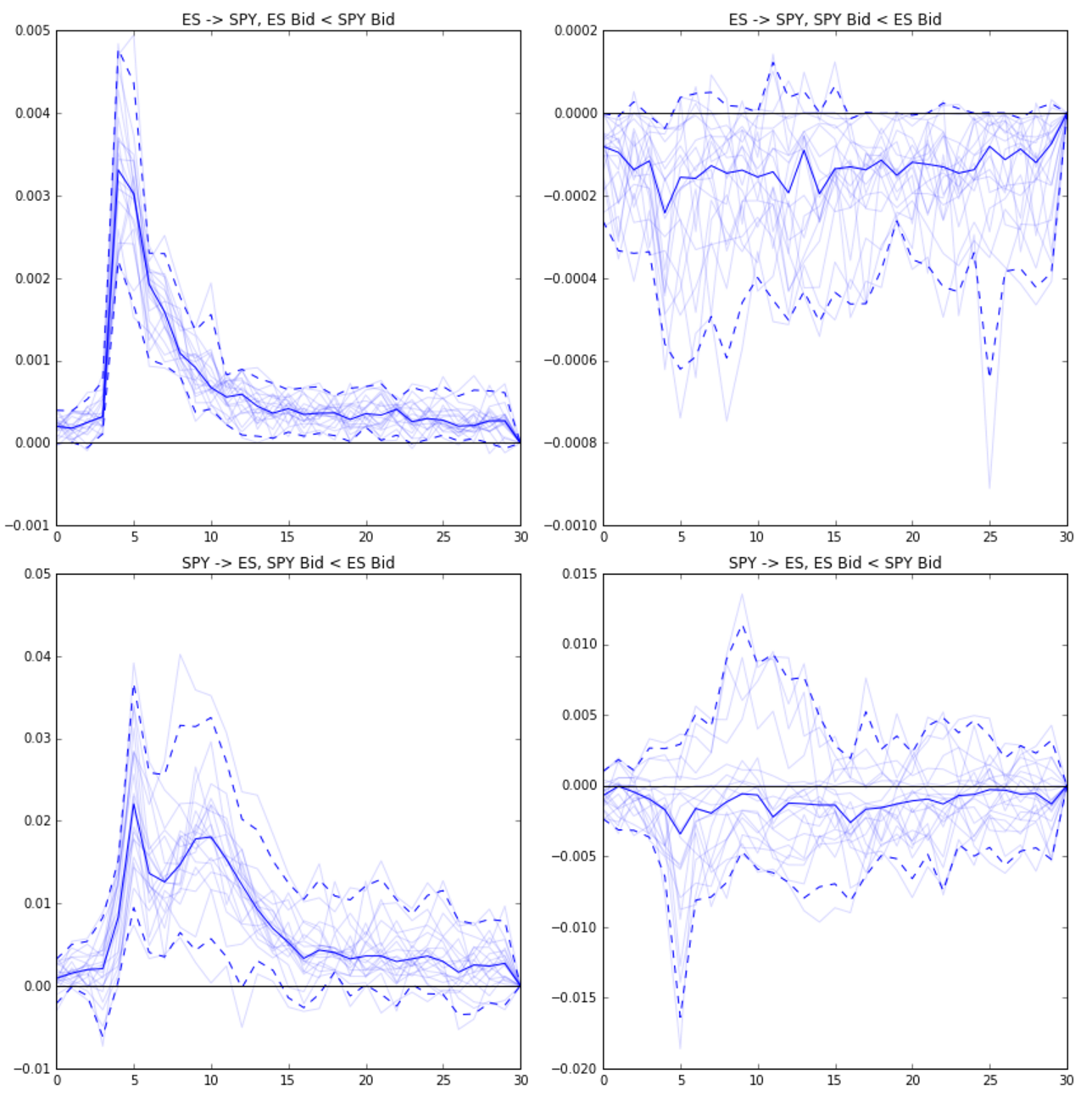

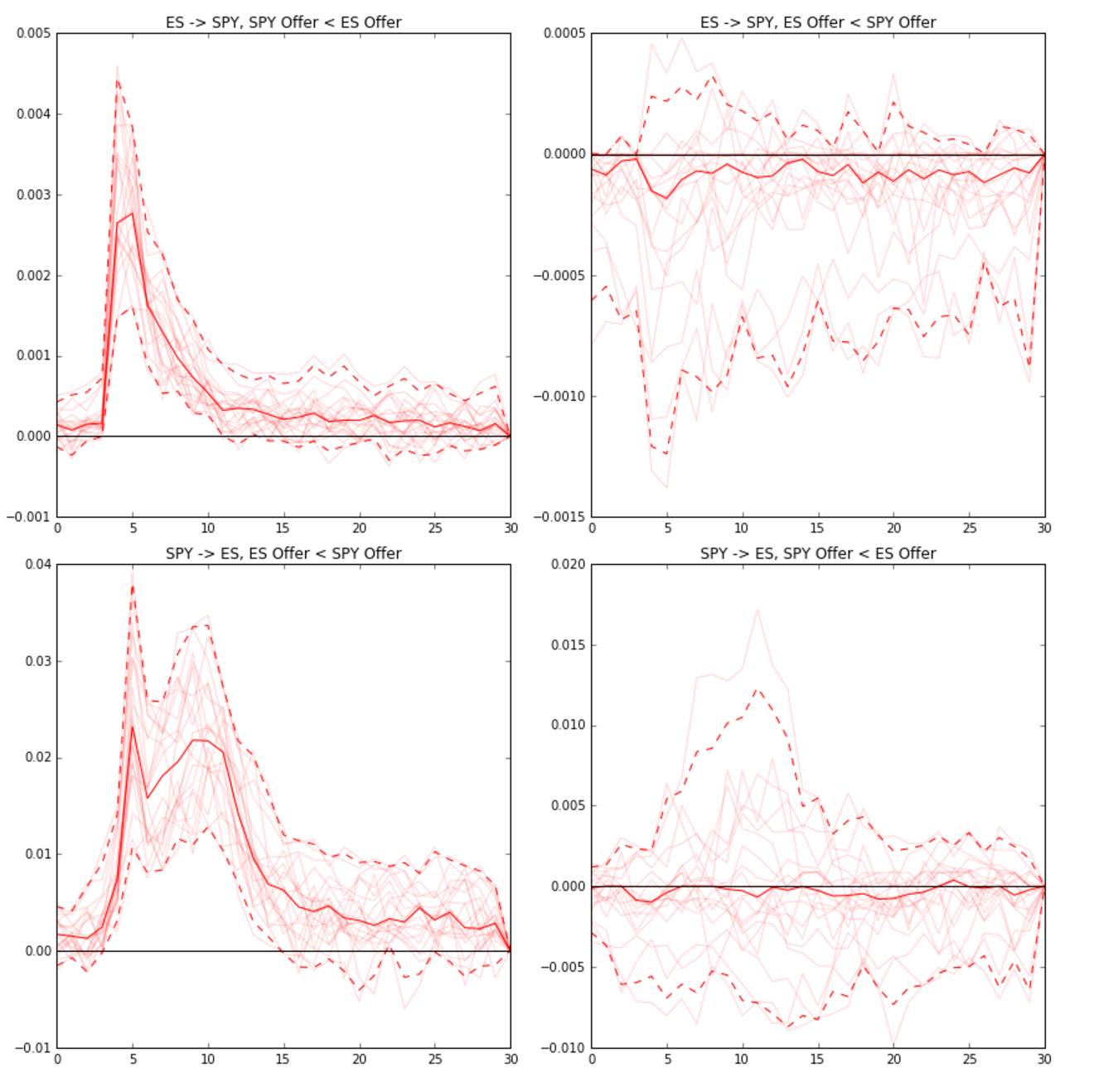

SPY Liquidity Response to ES¶

The following figure shows average net SPY liquidity response (shares added to offer minus shares added to bid) in each millisecond following ES liquidity change.

Reasons for Information Flow¶

- The standard explanation is leverage.

- Informed traders will first trade where they can obtain highest leverage.

- The data also suggests that relative price increment is an important determinant.

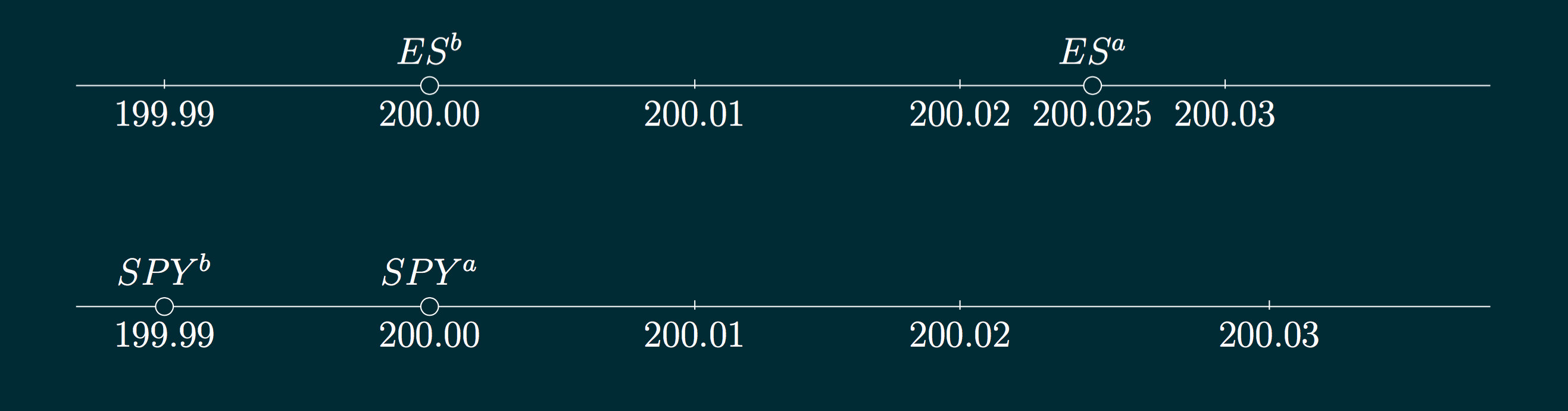

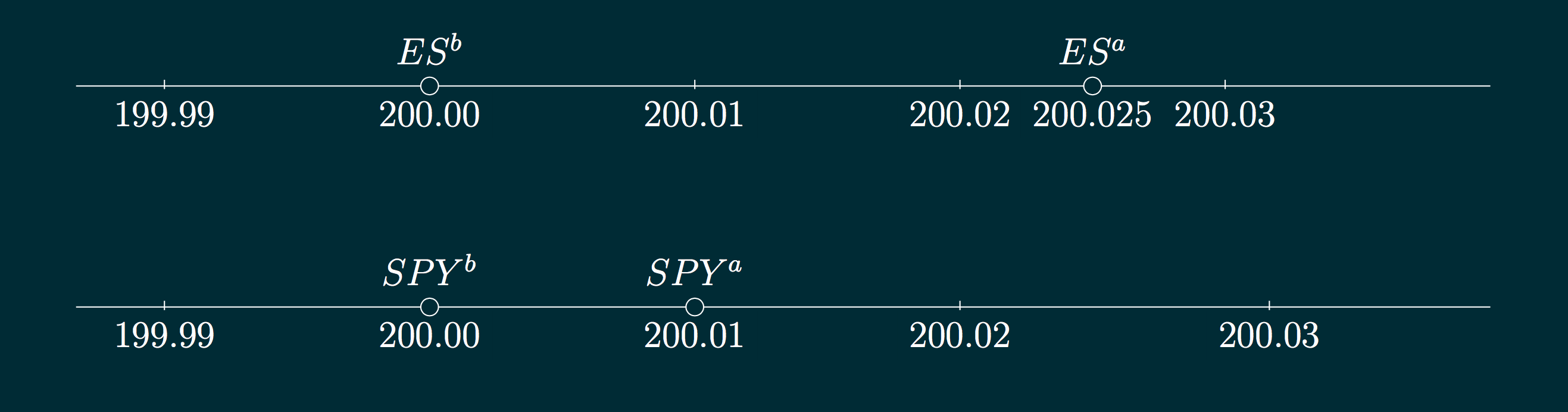

SPY/E-mini Contract Specs¶

E-mini:

- Quoted in S&P 500 index points.

- Notional value of one contract is 50x the index.

- Minimum price increment is 0.25 index points.

SPY:

- Quoted at 1/10th the value of the S&P 500 index.

- Notional value is equal to the price quotes.

- Minimum price increment is $0.01.

- Equivalent to 0.10 index points.

E-mini tick size is 2.5x SPY tick size.

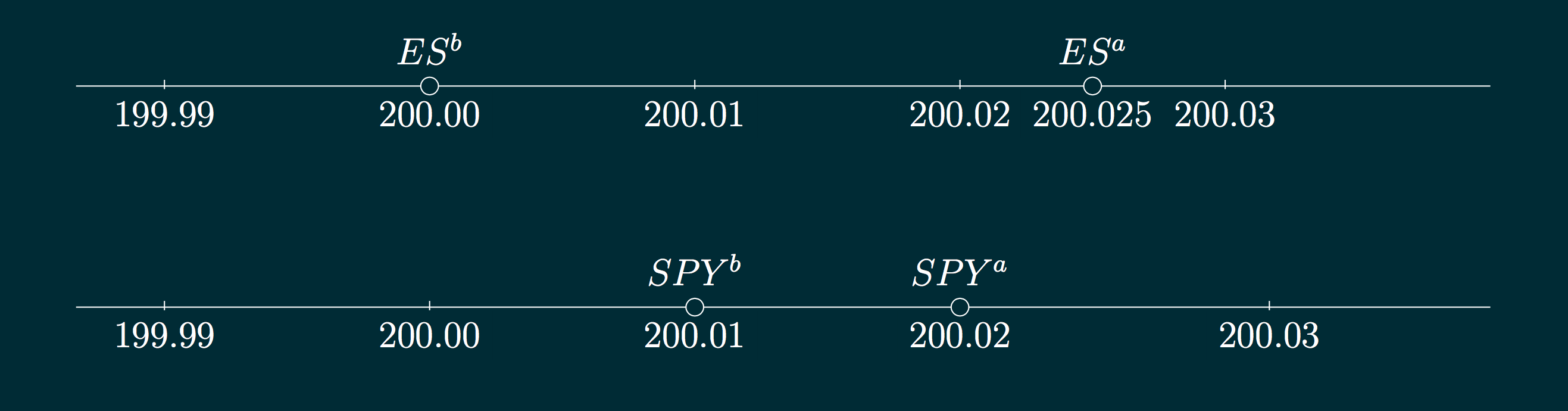

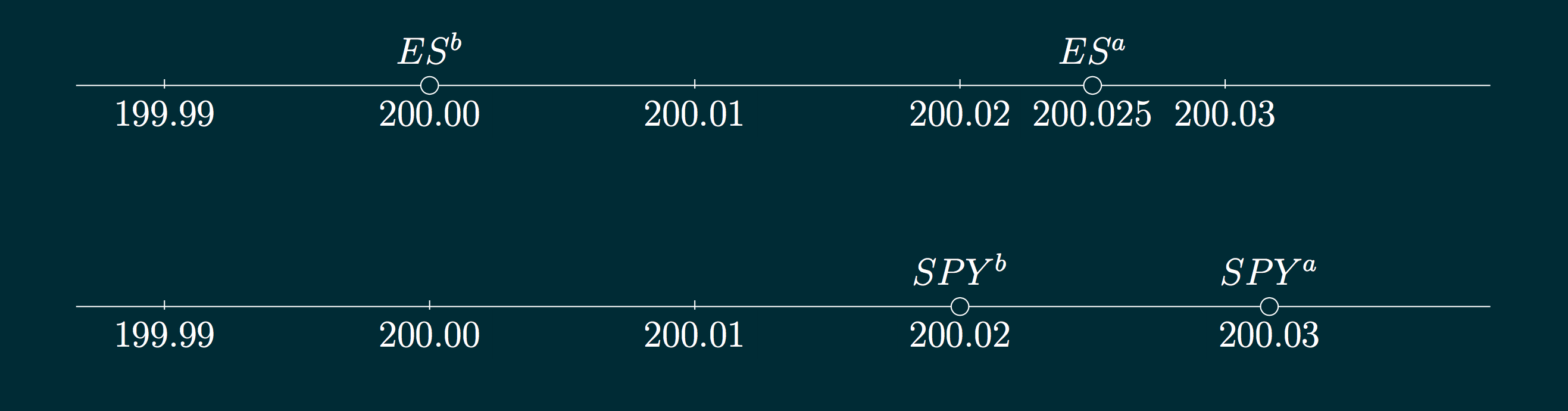

E-mini/SPY Spreads¶

E-mini/SPY Spreads¶

E-mini/SPY Spreads¶

E-mini/SPY Spreads¶

Spread and Information Flow¶

Differences in spreads creates arbitrage opportunities.

- The size of the spread differences determines size and frequency of arbitrages.

- Large ES spread relative to SPY spread means big arbs most of the time when a market maker is filled at CME.

- Less frequently, the SPY bid or offer will allow an arb in the reverse direction.

Implications¶

- If maker is filled at ES bid and ES bid < SPY bid: sell at SPY bid.

- SPY market responds to ES market.

- If maker is filled at ES offer and ES offer > SPY offer: buy at

SPY offer.

- SPY market responds to ES market.

- If maker is filled at SPY bid and SPY bid < ES bid: sell at ES bid.

- ES market responds to SPY market.

- If maker is filled at SPY offer and SPY offer > ES offer: buy at

ES offer.

- ES market responds to SPY market.

Empirical Results¶

Empirical Results¶

Notes on Results¶

- The previous results are base on the trading record from Aug 2015.

- The data strongly support the model predictions.

- There are typically 10 times as many ES events as SPY events.

- Each SPY event is 10 times more influential than an ES event.

- What does this mean if you are designing and exchange?