Implied Volatility and the Volatility Term Structure¶

Implied Volatility¶

Let \(\smash{C_{mkt}}\) and \(\smash{P_{mkt}}\) denote the market prices of call and put options. Recall that the implied volatility for strike \(\smash{X}\) is defined as the value \(\smash{\sigma_{imp}}\) such that

\[\begin{split}\begin{align}

C_{mkt} & = S_0 \Phi(d_1) - X e^{-rT} \Phi(d_2) \\

P_{mkt} & = X e^{-rT} \Phi(-d_2) - S_0 \Phi(-d_1)\\

d_1 & = \frac{\log(S_0/X) + (r+\sigma_{imp}^2/2)T}{\sigma_{imp} \sqrt{T}} \\

d_2 & = \frac{\log(S_0/X) + (r-\sigma_{imp}^2/2)T}{\sigma_{imp} \sqrt{T}} = d_1

- \sigma_{imp} \sqrt{T}.

\end{align}\end{split}\]

- That is, \(\smash{\sigma_{imp}}\) is the value such that \(\smash{C_{mkt} = C_{bs}}\) and \(\smash{P_{mkt} = P_{bs}}\).

Put-Call Parity¶

Both the BSM and market prices satisfy put-call parity:

\[\begin{split}\begin{align}

C_{mkt} + X e^{r_f} & = S_0 + P_{mkt} \\

C_{bs} + X e^{r_f} & = S_0 + P_{bs}.

\end{align}\end{split}\]

- As a result \(\smash{C_{mkt} - C_{bs} = P_{mkt} - P_{bs}}\).

- Thus, the implied vol for a particular strike that sets \(\smash{C_{mkt} = C_{bs}}\) is also the implied vol that sets \(\smash{P_{mkt} = P_{bs}}\) (for the same strike).

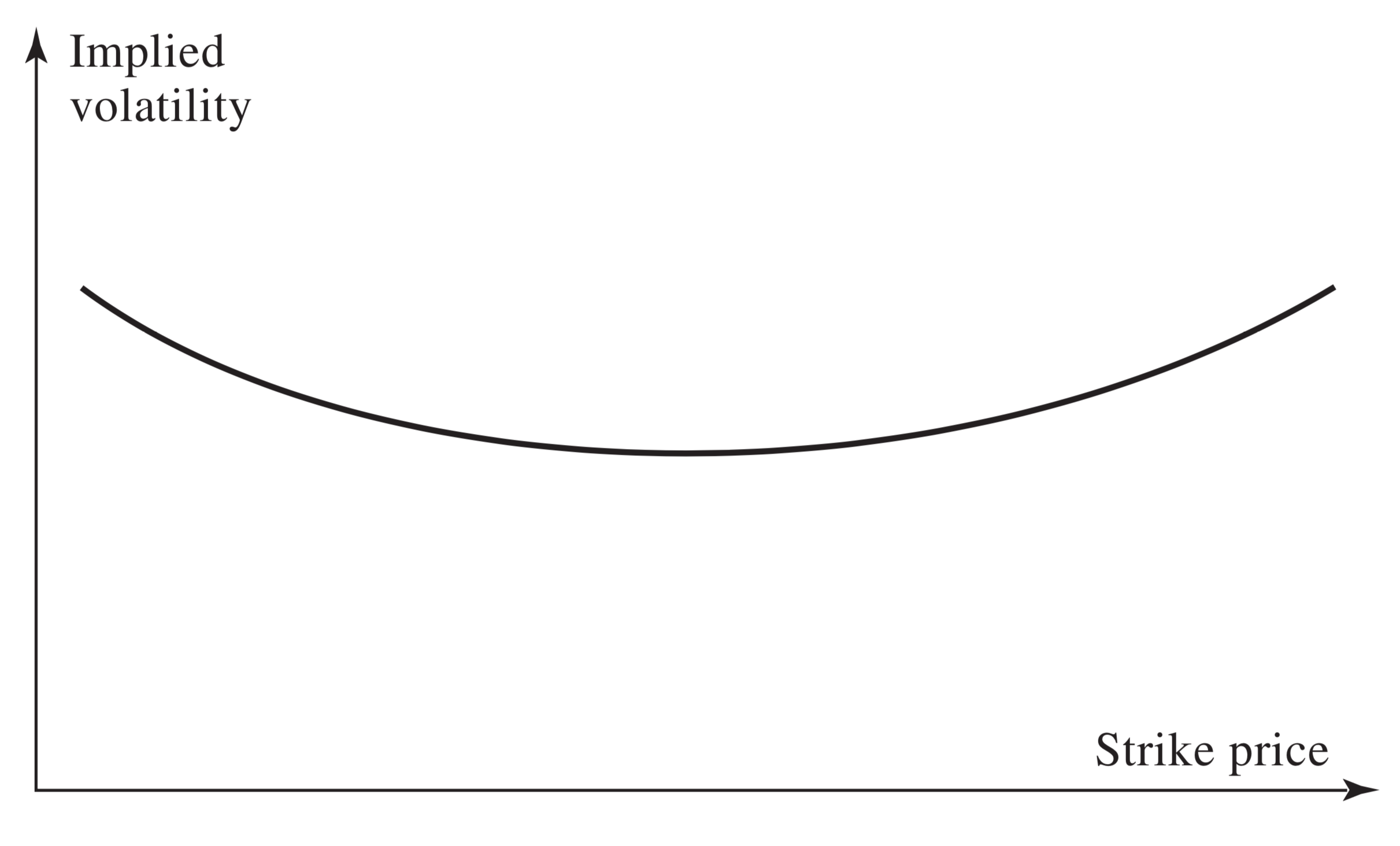

Foreign Exchange Vol Smile¶

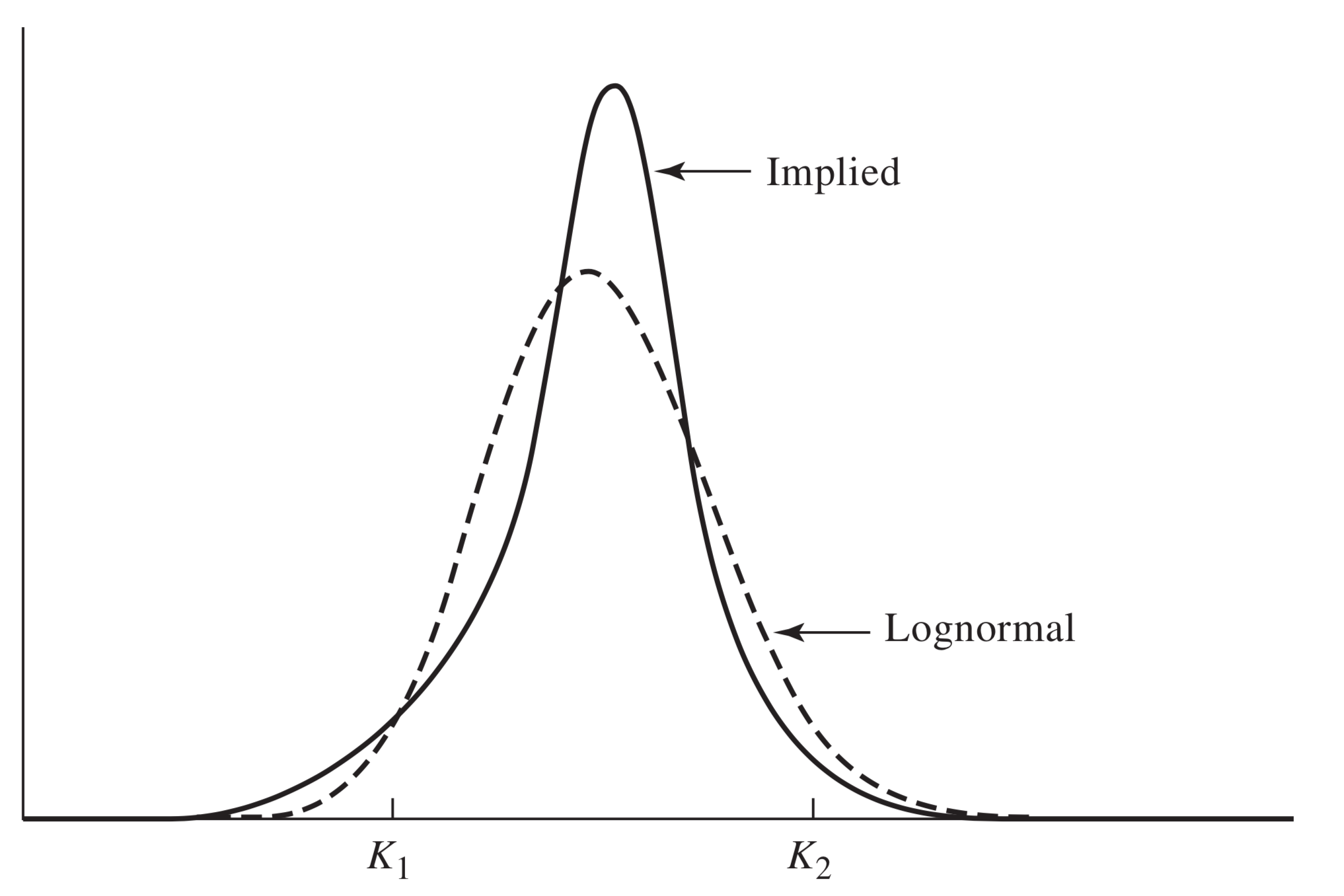

Foreign Exchange Implied Distribution¶

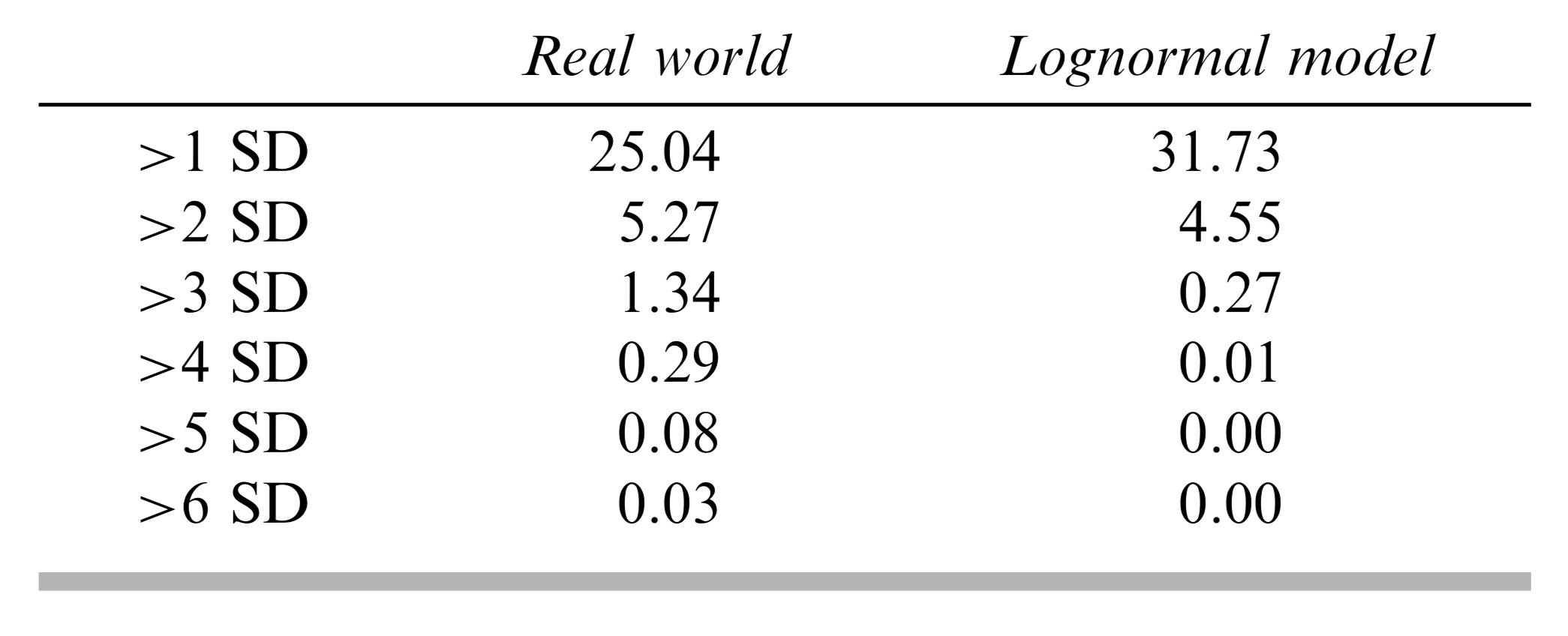

Evidence of Heavy Tails¶

The first column of the following table shows the fraction of times over a 10-year period that 12 currencies experienced a daily move that exceeded various thresholds. The second column compares the theoretical probabilities of a lognormal distribution.

Equities Exchange Vol Smile¶

Equities Implied Distribution¶

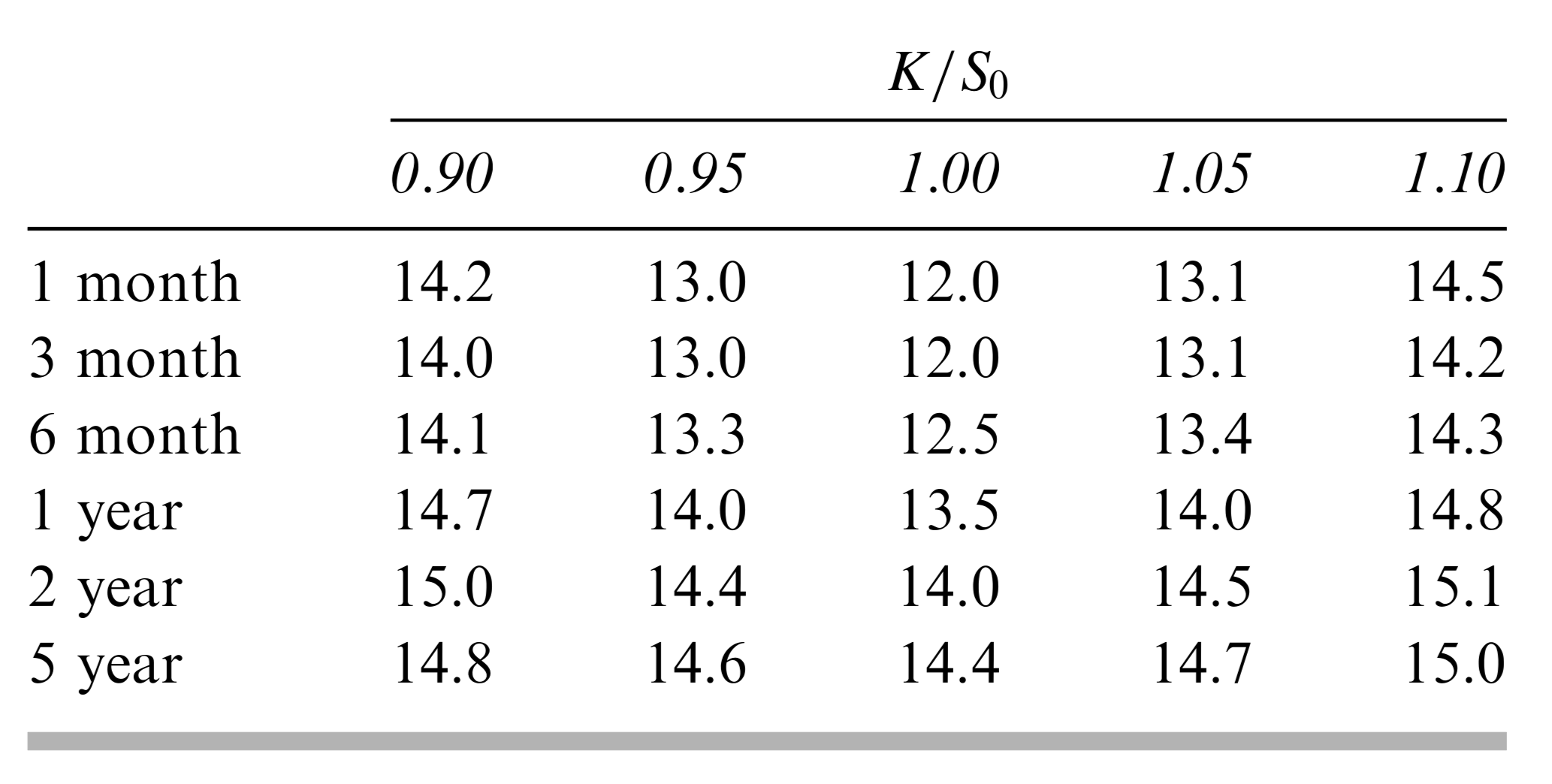

Volatility Surface¶