Hedging with Futures¶

Long and Short Hedges¶

A hedge is an investment that limits the risk of another risky investment. It typically consists of an offsetting position.

- Futures are used to hedge against price fluctuations of an asset that must be bought or sold at a future date.

- A long hedge is used when you will purchase an asset in the future.

- A short hedge is used when you will sell an asset in the future.

Short Hedge Example¶

Suppose it is May 15th and an oil producer has negotiated to sell 1 million barrels of crude oil on Aug 15. \(\smash{S_0 = \$80}\) and \(\smash{F_0 = \$79}\).

- The producer will gain/lose $10,000 for each 1 cent increase/decrease in the spot price.

- A hedge would consist of shorting 1000 futures contracts (for 1000 barrels each) with expiration as close to Aug 15th as possible.

- Suppose \(\smash{S_T = \$75}\) on Aug 15 - what are total profits for the producer?

- Suppose \(\smash{S_T = \$85}\) on Aug 15 - what are total profits for the producer?

Note that the producer will not want to deliver the barrels for the futures contract, but will close out early.

Long Hedge Example¶

Suppose it is Jan 15th and a copper producer has negotiated to buy 100,000 pounds of copper on May 15. \(\smash{S_0 = 340}\) cents and \(\smash{F_0 = 320}\) cents.

- The producer will gain/lose $1000 for each 1 cent decrease/increase in the spot price.

- A hedge would consist of buying 4 CME Group futures contracts (for 25,000 pounds each) with expiration as close to May 15th as possible.

- Suppose \(\smash{S_T = 320}\) cents on May 15 - what is the total cost for the producer?

- Suppose \(\smash{S_T = 305}\) cents on May 15 - what is the total cost for the producer?

Note that the producer will not want to take delivery for the futures contract, but will close out early.

Imperfect Hedging¶

It is typically difficult for an investor to exactly hedge a position.

- A futures contract may not exist for the exact asset to be hedged.

- E.g. VIX futures.

- The expiration of the futures may not coincide with the end of the termination of the position in interest.

- The termination date of the underlying position may be unknown.

Basis¶

For traders, the basis is defined as the difference between the futures and spot prices.

- Traditional definition: \(\smash{b_t = S_t - F_t}\).

- For financial assets: \(\smash{b_t = F_t - S_t}\).

- Recall

- Note that the basis can be positive or negative.

Basis Fluctuation¶

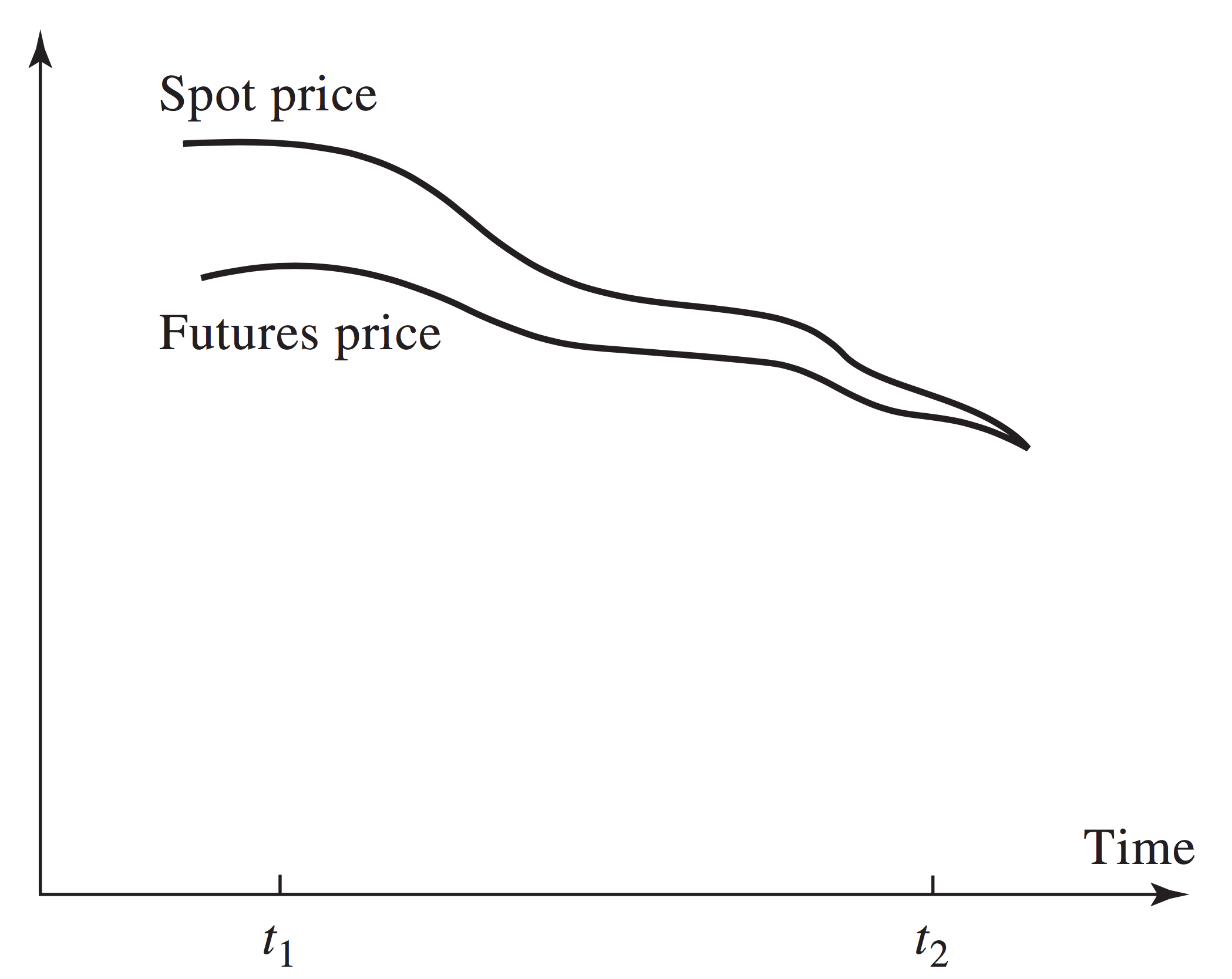

The basis can fluctuate through time.

- The futures price should converge to the spot price at expiry. This is a deterministic change in the basis related to shortening time window \(\smash{T-t}\).

- The basis may also fluctuate due to random variation in the cost of

carry, \(\smash{c}\).

- This is caused by random fluctuations in \(\smash{r}\), \(\smash{r_f}\), dividends, storage costs, etc.

Stylized Basis Fluctuation¶

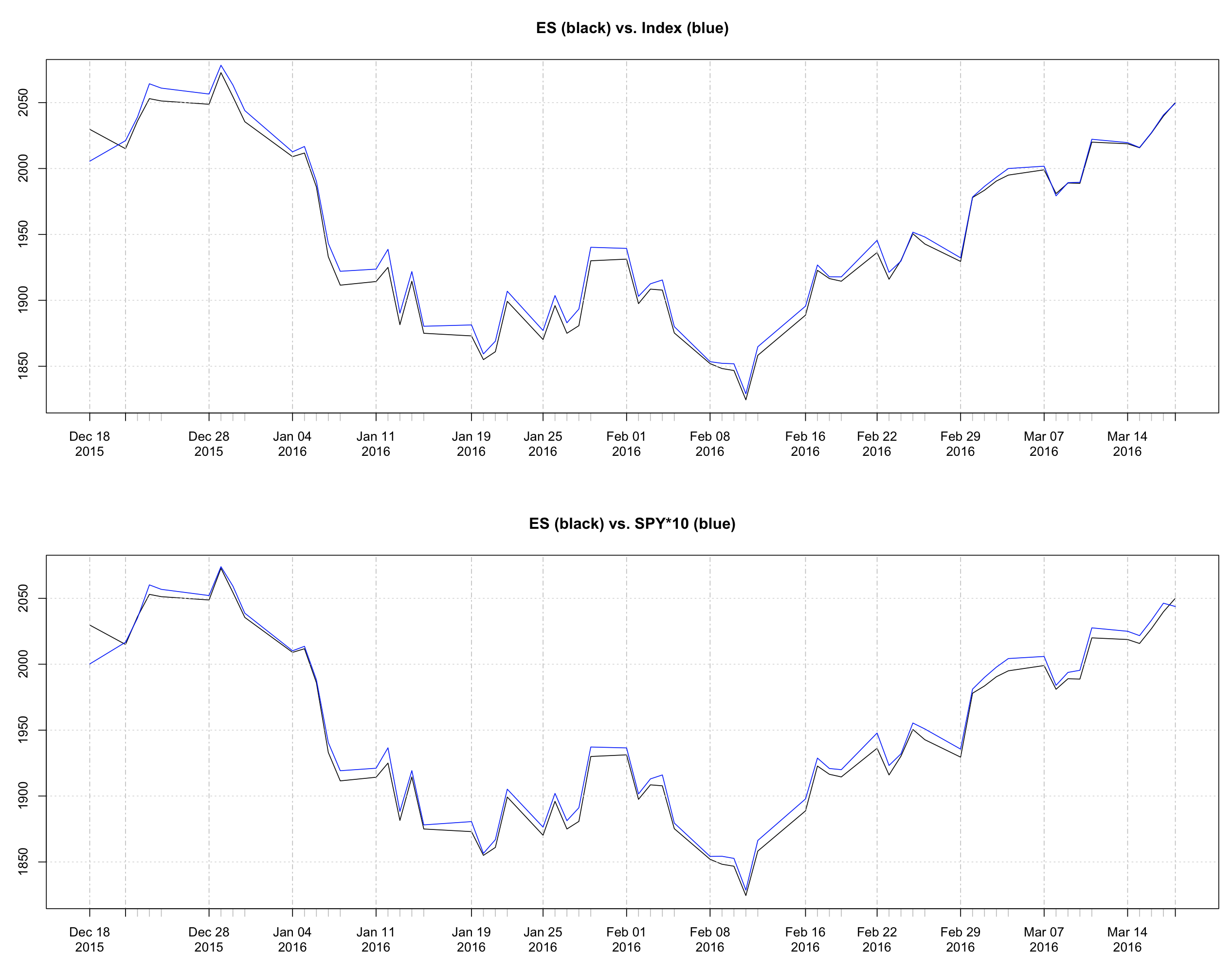

Actual Basis Fluctuation¶

Hedging and Basis¶

Consider an arbitrary asset with the following spot and futures prices at \(\smash{t_1}\) and \(\smash{t_2}\): \(\smash{S_1 = \$2.50}\), \(\smash{F_1 = \$2.20}\), \(\smash{S_2 = \$2.00}\) and \(\smash{F_2 = \$1.90}\).

- \(\smash{b_1 = \$0.30}\) and \(\smash{b_2 = \$0.10}\).

- If you hold the asset and plan to sell at \(\smash{t_2}\), how can you hedge?

- Profit: \(\smash{S_2 + F_1 - F_2 = F_1 + b_2 = \$2.30}\).

- If you need to purchase the asset at \(\smash{t_2}\), how can you hedge?

- Cost: \(\smash{S_2 + F_1 - F_2 = F_1 + b_2 = \$2.30}\).

Basis Risk¶

Note that the profit/cost of the hedging strategies above is \(\smash{F_1 + b_2}\).

- If \(\smash{b_2}\) is known at \(\smash{t_1}\), then a perfect hedge could be designed.

- Basis change due to \(\smash{t_2-t_1}\) is perfectly foreseeable.

- Basis fluctuation due to random variations in \(\smash{c}\) is not perfectly foreseeable.

Contract Choice¶

Perfect hedges typically don’t exist. Important decisions for the hedge include:

- An asset with a futures contract that closely approximates the asset to be hedged.

- Expiry close to the necessary terminal date of the hedge.

- Typically, expiry is chosen to be a month following hedge termination so that delivery doesn’t occur and rolling is unnecessary.

Example: Hedging Yen¶

Suppose it’s March 1st and you will receive 50 million Yen at end of July. Yen futures contracts are for delivery of 12.5 million Yen in Mar/Jun/Sep/Dec.

- How can you hedge?

Assume the following spot and (Sep) futures prices (cents/Yen): \(\smash{F_1 = 0.9800}\), \(\smash{S_2 = 0.9200}\) and \(\smash{F_2 = 0.9250}\).

- What is the price you pay for Yen?

- \(\smash{F_1 + b_2 = 0.9800 + (0.9200 - 0.9250) = 0.9750}\) per Yen.

- For 50 million Yen: \(\smash{50,000,000 \times 0.9750 = 48,750,000}\) cents or \(\smash{\$487,500}\).

Cross Hedging¶

A cross hedge occurs when the asset being hedged is different from the asset underlying a futures contract.

- Since the two assets may not be perfectly correlated, an adjustment must be made to determine the optimal number of futures contracts to hold.

- The optimal number of futures is determined via the hedge ratio.

Hedge Ratio¶

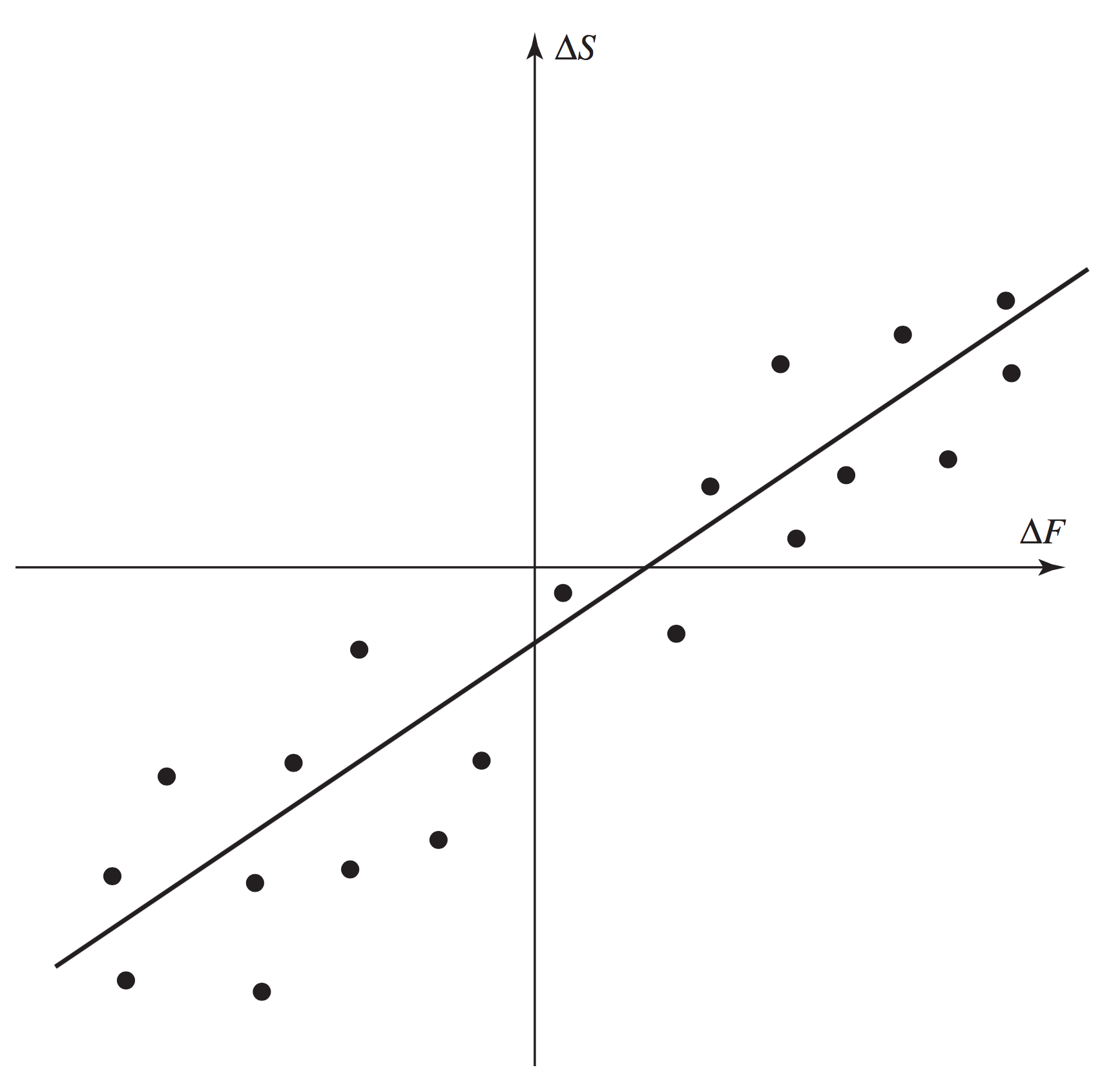

The optimal hedge ratio is defined as

- \(\smash{h^*}\) is the slope of a regression of \(\smash{\Delta S}\) on \(\smash{\Delta F}\).

- The hedge ratio is typically computed by estimating \(\smash{\rho}\), \(\smash{\sigma_S}\) and \(\smash{\sigma_F}\) with historical data.

Hedge Ratio with Returns¶

Note that

where \(\smash{r_S}\) and \(\smash{r_F}\) are returns (not price changes).

- An alternate definition of the hedge ratio is:

Hedge Ratio Regression¶

Hedge Ratio¶

Note that if the asset underlying the futures is identical to the asset being hedged:

- \(\smash{\rho = 1}\), \(\smash{\sigma_S = \sigma_F}\) and \(\smash{h^* = 1}\).

If \(\smash{\rho = 1}\) and \(\smash{\sigma_S = 2\sigma_F}\), you need to hedge with two futures.

- The assets are perfectly correlated, but price swings in the futures are only half as large as those for the asset being hedged.

Optimal Number of Contracts¶

The optimal number of contracts to purchase for a cross hedge is

where \(\smash{Q_S}\) is the size of the position being hedged, \(\smash{Q_F}\) is the size of a futures contract and \(\smash{V_S}\) and \(\smash{V_F}\) are their total valuations (shares times price).

Hedge Ratio Example¶

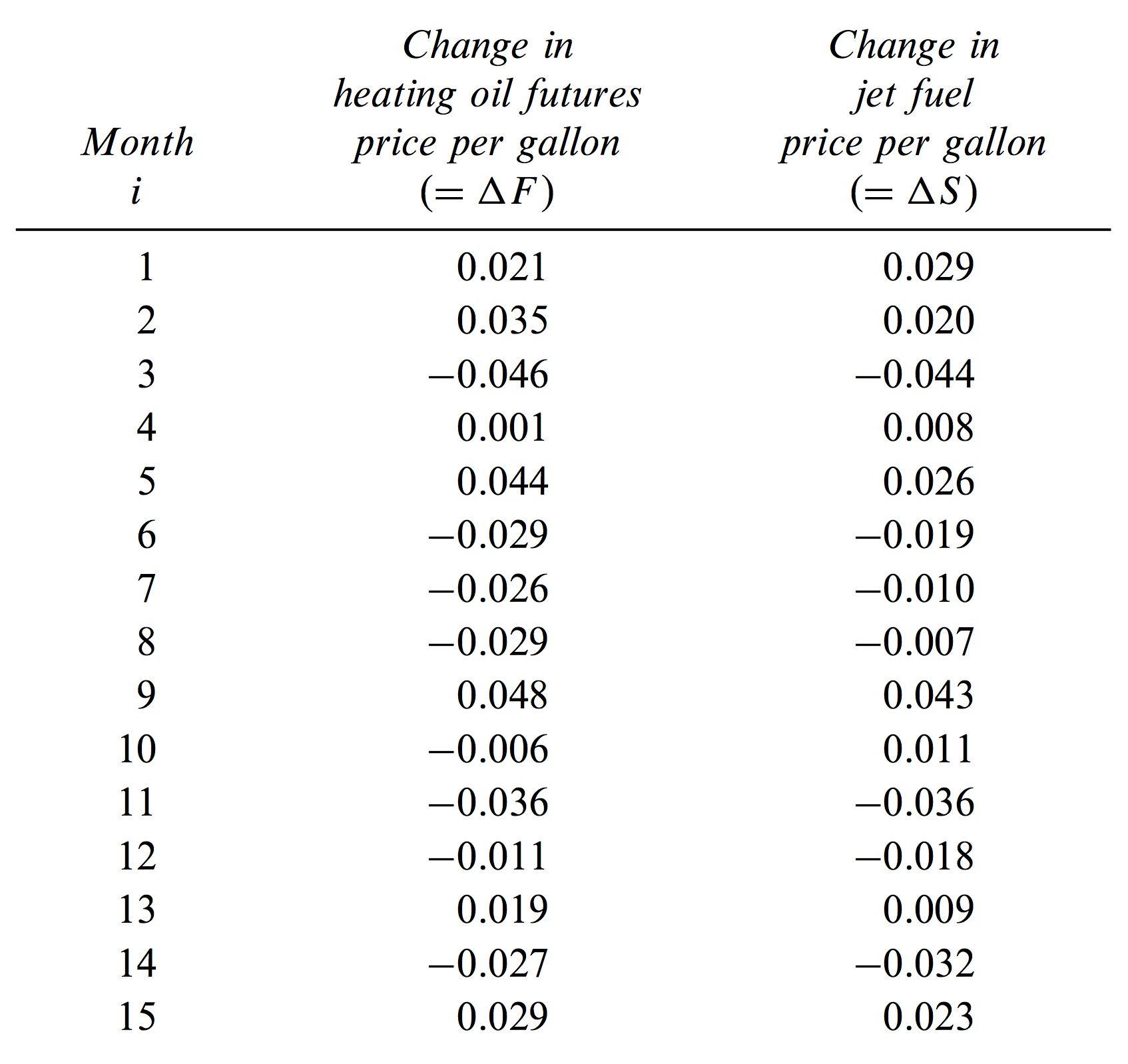

An airline company needs to purchase 2 millions gallons of jet fuel in 1 month.

- CME Group heating oil futures are the best contract to use as a hedge.

- One contract is for delivery of 42,000 gallons of heating oil.

- The table on the following slide has historical data to estimate the optimal hedge ratio.

Hedge Ratio Example¶

Hedge Ratio Example¶

Using the data:

- \(\smash{\hat{\rho} = 0.928}\), \(\smash{\hat{\sigma}_S = 0.0263}\) and \(\smash{\hat{\sigma}_F = 0.0313}\).

Hedging an Equity Portfolio¶

Suppose you want to hedge an equity portfolio which has some sensitivity to the market, \(\smash{\beta}\):

- \(\smash{r_p}\), \(\smash{r_I}\) and \(\smash{r_f}\) are the portfolio, market index (S&P 500) and risk-free returns, respectively.

- Since \(\smash{\beta}\) is the slope of the regression of excess returns, it is the hedge ratio, \(\smash{\tilde{h}}\).

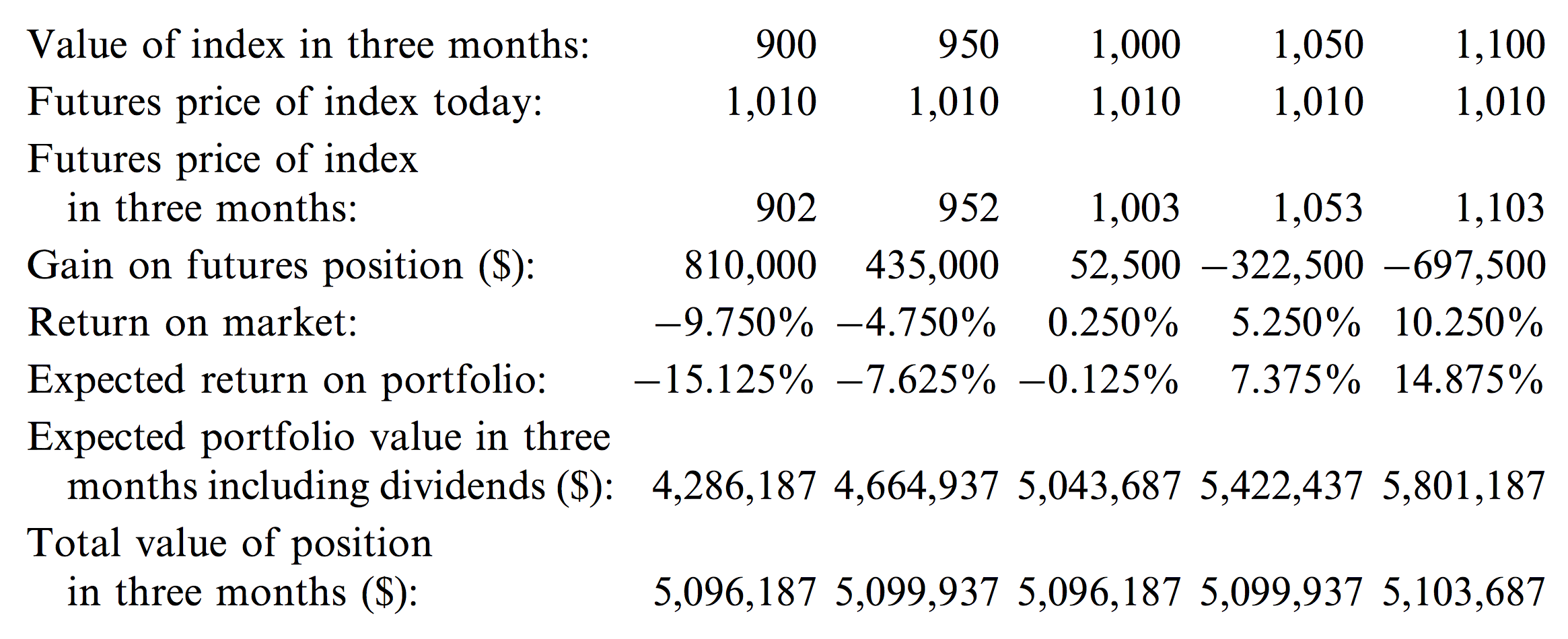

Hedging Equity Portfolio Example¶

Suppose:

- \(\smash{P_{SP500} = 1000}\).

- \(\smash{P_{ES} = 1010}\).

- Portfolio Value \(\smash{\$5,050,000}\).

- \(\smash{r_f = 0.04}\) per annum.

- Index dividend yield \(\smash{0.01}\) per annum.

- \(\smash{\beta = 1.5}\).

Hedging Equity Portfolio Example¶

Why Hedge?¶

Note that the index hedge results in a portfolio that earns grows at the risk-free rate.

- So why hedge?

- Perhaps you think your portfolio will earn positive non-market return (alpha) but don’t want to be exposed to the market.

- Perhaps you want to hold the portfolio for a long period of time, but need a brief reduction of risk exposure.

Changing Beta¶

A complete hedge (as above) makes the effective beta zero.

- Suppose you simply want to change the beta of your portfolio to a new value, \(\smash{\beta^*}\)?