Forward Contracts¶

Forward Contract Definition¶

Definition: A forward contract is an agreement to exchange an asset at a future date at a prespecified price.

- The contract settlement date is called the expiration date.

- The asset that is exchanged is called the underlying asset.

- The buyer holds the long position.

- The seller holds the short position.

- There is no initial payment or premium.

Delivery and Settlement¶

There are two types of forward contract settlements.

- Delivery: The long position pays the prespecified price to the short position, who delivers the asset.

- Cash settlement: The long and short positions pay the net cash value to the other.

Forward Example¶

Two parties contract to exchange a \(\smash{\$100}\) bond for \(\smash{\$98}\) at a future date.

- If the bond is worth \(\smash{\$98.25}\) at expiry, the short position pays \(\smash{\$0.25}\) to the long position at expiry.

- If the bond is worth \(\smash{\$97.50}\) at expiry, the long position pays \(\smash{\$0.50}\) to the short position at expiry.

- Cash-settled forwards are often called NDFs, or nondeliverable forwards.

- Usually, cash settlement is used for underlying assets that are difficult to exchange (think of a stock index).

Early Termination¶

Suppose one party in a forward contract wishes to terminate early.

- She could engage in another forward contract on the opposite side.

- Depending on market conditions, the new contract may be written at a new price.

Early Termination Example¶

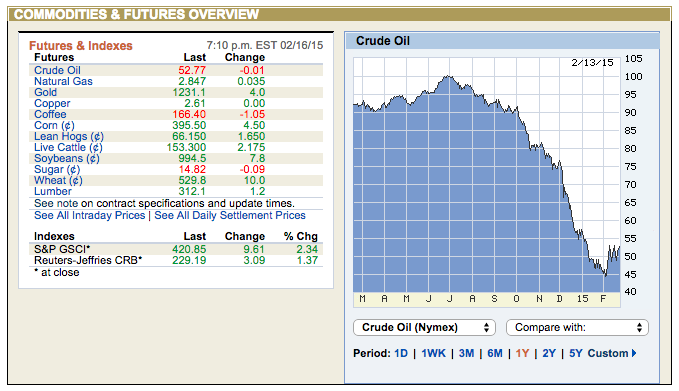

Suppose a trader enters a long forward contract position to exchange a barrel of crude oil on 13 Feb 2015 and decides to terminate the contract on 16 Feb 2015.

- On 13 Feb, the forward price is $52.78 per barrel.

- On 16 Feb, the forward price is $52.73 per barrel.

- She can write a forward contract for $52.73 on 16 Feb.

- Note that she takes a $0.05 loss and is still exposed to risk of default on two different contracts.

- Alternatively, she can ask her original counterparty to accept the present value of $0.05 to terminate.

Notation¶

We will use the following notation:

- \(\smash{S_0}\): Spot price of the underlying asset today.

- \(\smash{F_0}\): Forward price of the underlying asset today.

- \(\smash{T}\): Time until delivery.

- \(\smash{r}\): Risk-free rate of interest for maturity \(\smash{T}\).

Note that any units (minutes, hours, days, weeks, months, years) may be used for \(\smash{T}\), but that the interest rate, \(\smash{r}\), must be adjusted accordingly.

Forward Valuation¶

The price of a forward contract with maturity \(\smash{T}\) for an asset with price \(\smash{S_0}\) is:

- \(\smash{r}\) is the risk-free interest rate over period \(\smash{T}\).

- If \(\smash{r}\) is constant, \(\smash{F_0}\) is a deterministic function of the spot sprice, and has nothing to do with the unknown, future price of the asset.

- \(\smash{e^{rT}}\) is known as the basis.

- Intuition: the foward holder must pay the holder of the spot contract for interest that would have been earned.

Forward Valuation Example¶

Suppose you would like to purchase a 3-month forward contract on Coca-Cola (KO) stock on 1 Mar 2016. What is the value of the forward (assuming the stock never pays dividends)?

- Set \(\smash{T = 0.25}\) (i.e. time units of 1 year).

- Use Yahoo Finance to determine \(\smash{S_0 = \$43.35}\).

- Use Quandl to determine the (annualized) yield on the 3-month U.S. Treasury Bill: \(\smash{r = 0.0033}\).

Thus,

Forward Valuation with Income¶

Suppose the underlying asset provides income with present value \(\smash{I}\).

- This may be a single payment or a stream of payments, all appropriately discounted:

- This assumes \(\smash{m}\) equally spaced payments of equal size during interval \(\smash{T}\).

The value of a forward contract is now:

Forward Valuation with Yield¶

Suppose the underlying asset provides income yield (continuously compounded) \(\smash{q}\). Then:

- Intuition: the holder of the spot contract now pays interest (implicitly), but earns income. The foward holder must compensate the spot holder for interest, net of income earned over period \(\smash{T}\).

Forward Valuation with Yield Example¶

Reconsider the previous example for Coca-Cola stock.

- Now assume that KO has an annualized dividend yield of 3%.

The forward price is

Forward Valuation for Currency¶

Suppose the underlying asset is a currency, and that the risk-free interest rate in the foreign market is \(\smash{r_f}\). Then:

- The foreign interest is income and the rate is the income yield.

Curreny Forward Example¶

What is the value of a 6-month forward contract for Canadian dollars (CAD) on 1 Mar 2016?

- Set \(\smash{T = 0.5}\) (i.e. time units of 1 year).

- Use Quandl to determine the spot exchange rate for USD/CAD: \(\smash{S_0 = \$1.34}\).

- Use Quandl to determine the (annualized) yield on the 3-month Canadian Treasury Bill: \(\smash{r_f = 0.0047}\). We already determined that \(\smash{r = 0.0033}\).

Thus,

Forward Valuation for Commodities¶

Suppose that the underlying is a physical asset that must be stored. Then:

or

- \(\smash{U}\) is the present value of storage costs.

- \(\smash{u}\) is the annual storage cost expressed as a fraction of commodity value.

- Note that storage costs are like negative income.

Cost of Carry¶

The foregoing compounding rates are referred to as the cost of carry, \(\smash{c}\).

- The cost of carry includes interest rate and storage costs, minus income.

- For a stock index that pays a dividend yield, \(\smash{c = r-q}\).

- For a foreign currency, \(\smash{c = r - r_f}\).

- For a commodity that provides income, \(\smash{c = r - q + u}\).