Wiener Processes¶

Stochastic Processes¶

A stochastic process is a collection of random variables, indexed by time.

- More simply, it can be thought of as a single random variable that evolves dynamically with time.

- Stochastic processes can be discrete/continuous time: either they evolve discretely or continuously.

- They can be discrete/continuous value: at each time, they are drawn from either a discrete or continuous probability distribution.

- We will develop a continuous time/continuous value model for asset

prices.

- Note that we only observe discrete value and discrete time observations for actual asset prices.

Properties of Expected Value¶

Given random variables \(\smash{X}\) and \(\smash{Y}\), define a new random variable \(\smash{Z = X + Y}\). Then:

Suppose \(\smash{E[X] = E[Y] = \mu}\). Then:

Properties of Expected Value¶

Extending the prior result, given random variables \(\smash{\left\{X_i\right\}_{i=1}^n}\), define a new random variable \(\smash{Z = \sum_{i=1}^n X_i}\). Then:

Suppose \(\smash{E[X_i] = \mu, \,\, i=1,\ldots,n}\). Then:

Properties of Variance¶

Given random variables \(\smash{X}\) and \(\smash{Y}\), define a new random variable \(\smash{Z = X + Y}\). Then:

Suppose \(\smash{Var(X) = Var(Y) = \sigma^2}\) and that they are independent \(\smash{(Cov(X,Y)=0)}\). Then:

Properties of Variance¶

Extending the prior result, given random variables \(\smash{\left\{X_i\right\}_{i=1}^n}\), define a new random variable \(\smash{Z = \sum_{i=1}^n X_i}\). Then:

Suppose \(\smash{Var(X_i) = \sigma^2, \,\, i=1,\ldots,n}\) and that each random variable is independent of the others \(\smash{(Cov(X_i,X_j)=0, \,\, i \neq j)}\). Then:

Normal Random Variables¶

Suppose \(\smash{X_i \sim N(\mu,\sigma), \,\, i=1,\ldots, n}\).

- Define a new random variable \(\smash{Z = \sum_{i=1}^n X_i}\).

- We already know \(\smash{E[Z] = n\mu}\) and \(\smash{Sd(Z) = \sqrt{n} \sigma}\).

- However, the sum of Normals is also Normal: \(\smash{Z \sim N\left(n\mu, \sqrt{n} \sigma\right)}\).

Additive Normal Example¶

Suppose the monthly return on an asset is Normally distributed for each month over the next year.

We will assume the expected value is 1% and standard deviation is 5% and that returns across months are independent:

\[\begin{align} R_i \stackrel{i.i.d.}{\sim} N(0.01,0.05), \,\,\,\, i = 1,\ldots, 12. \end{align}\]

- The annual return is the sum of monthly returns: \(\smash{R_a = \sum_{i=1}^{12} R_i}\).

- The distribution of the annual return is \(\smash{R_a \sim N(0.12,0.1732)}\).

Additive Normal Example¶

Note that we can also work backwards.

- Suppose you know that the annual expected return is \(\smash{\mu_a = 0.12}\), the annual standard deviation is \(\smash{\sigma_a = 0.1732}\) and that monthly returns are independent.

The monthly expected return and standard deviation are:

\[\begin{split}\begin{align} \mu_m & = \frac{\mu_a}{n} = \frac{0.12}{12} = 0.01 \\ \sigma_m & = \frac{\sigma_a}{\sqrt{n}} = \frac{0.1732}{\sqrt{12}} = 0.05. \end{align}\end{split}\]

Wiener Process¶

A random variable \(\smash{Z(t)}\) follows a Wiener process if:

During a short time interval \(\smash{\Delta t}\),

\[\begin{split}\begin{align} \Delta Z(t) & = Z(t) - Z(t-\Delta t) = \varepsilon \sqrt{\Delta t}, \,\,\, \varepsilon \sim N(0,1). \end{align}\end{split}\]

- The values of \(\smash{\Delta Z(t)}\) for any two short intervals \(\smash{\Delta t}\) are independent.

- As \(\smash{\Delta t \to 0}\), we use the notation \(\smash{dZ = \varepsilon \sqrt{dt}}\).

Moments of the Wiener Process¶

What are the first two moments of \(\smash{\Delta Z(t)}\)?

Wiener Process Over Long Horizon¶

Consider the evolution of \(\smash{Z(t)}\) over a longer horizon \(\smash{T}\).

- Divide the time interval \(\smash{(0,T)}\) into \(\smash{N}\) small intervals of equal length \(\smash{\Delta t}\).

Then:

\[\begin{split}\begin{align} Z(T) - Z(0) & = \sum_{i=1}^N \varepsilon_i \sqrt{\Delta t}, \,\,\, \varepsilon_i \stackrel{i.i.d.}{\sim} N(0,1). \end{align}\end{split}\]

Wiener Process Over Long Horizon¶

The resulting moments are:

\[\begin{split}\begin{align} E\left[Z(T) - Z(0)\right] & = \sum_{i=1}^N \sqrt{\Delta t} E[\varepsilon_i] = 0 \\ Var\left(Z(T) - Z(0)\right) & = \sum_{i=1}^N \Delta t Var(\varepsilon_i) = T \\ Sd\left(Z(T) - Z(0)\right) & = \sum_{i=1}^N \sqrt{\Delta t} Sd(\varepsilon_i) = \sqrt{T}. \end{align}\end{split}\]

Wiener Process Sample Paths¶

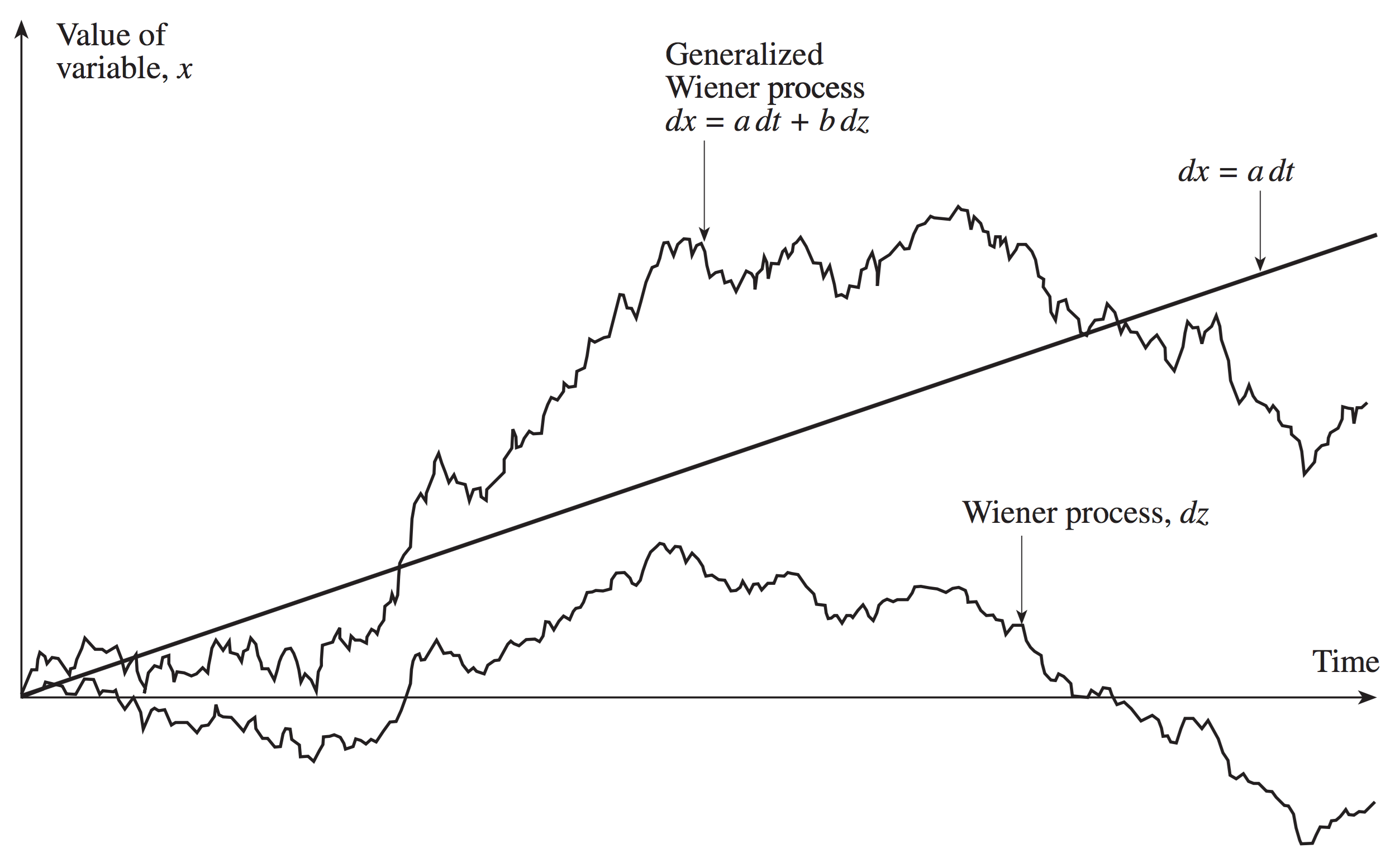

Generalized Wiener Process¶

Consider the generalized Wiener process:

- \(\smash{a}\) is the drift rate and \(\smash{b^2}\) is the variance rate.

- The basic Wiener process has drift rate zero and unit variance rate.

Generalized Wiener Process¶

In discrete time, the generalize Wiener process is

The moments are:

Wiener Process Comparison¶

Ito Process¶

An Ito process is a generalization of a generalized Wiener process:

- The drift rate and variance rate are functions of the process value and time - i.e. they are variable.

In discrete time:

- The discrete time analog requires an approximation: the drift and variance rate are constant over small intervals \(\smash{\Delta t}\).

Model for Asset Prices¶

We will use an Ito process as a model for asset prices.

- We think of percentage returns as being constant for a particular asset.

- This means that the size of the moves (the drift) changes with the level of the price.

- Variance also typically changes with the level of asset prices.

- This means an Ito process is a better model than a generalized Wiener process.

Model for Asset Prices¶

We will employ the following Ito process:

- The drift rate function takes the specific form:

\(\smash{a(S,t) = \mu S}\).

- The drift rate increases proportionally with the asset price and does not depend on time.

- The variance rate function takes the specific form:

\(\smash{b^2(S,t) = \sigma^2 S^2}\).

- The volatility, \(\smash{b(S,t) = \sigma S}\), increases proportionally with the asset price and does not depend on time.

- This form of an Ito process is known as geometric Brownian motion.

Geometric Brownian Motion¶

Geometric Brownian motion can also be written as:

- \(\smash{\frac{dS}{S}}\) is effectively the return.

- Note that returns evolve as a generalized Wiener process (constant drift and variance rates).

- \(\smash{\mu}\) and \(\smash{\sigma}\) are the expected return and volatility of the asset.

Geometric Brownian Motion¶

In discrete time, geometric Brownian motion is described as:

This means \(\smash{\frac{\Delta S}{S} \sim N(\mu \Delta t, \sigma \sqrt{\Delta t})}\).

Parameter Estimation¶

We can estimate the parameters \(\smash{\mu}\) and \(\smash{\sigma}\) from historical data.

- Set an interval of time, \(\smash{\Delta t}\) in years (days, weeks, months, etc).

- Collect \(\smash{n+1}\) price observations for the beginning and end of each interval.

- Compute \(\smash{n}\) returns for the invervals.

- Set \(\smash{\hat{\mu}}\) and \(\smash{\hat{\sigma}}\) to the sample mean and sample standard deviation of the returns.

- \(\smash{\hat{\mu}}\) is an estimate of \(\smash{\mu \Delta t}\), not \(\smash{\mu}\).

- \(\smash{\hat{\sigma}}\) is an estimate of \(\smash{\sigma \sqrt{\Delta t}}\), not \(\smash{\sigma}\).

Simulating Geometric Brownian Motion¶

Let’s estimate the daily mean and standard deviation of Lockheed Martin (LMT) returns using data prior to January 1, 2015:

> library(quantmod)

> getSymbols("LMT",src="yahoo", from="2010-01-01", to="2014-12-31")

> lmtRets = dailyReturn(LMT)

> mu = mean(lmtRets)

> sigma = sd(lmtRets)

> cat(mu,sigma)

0.0008037858 0.01122918

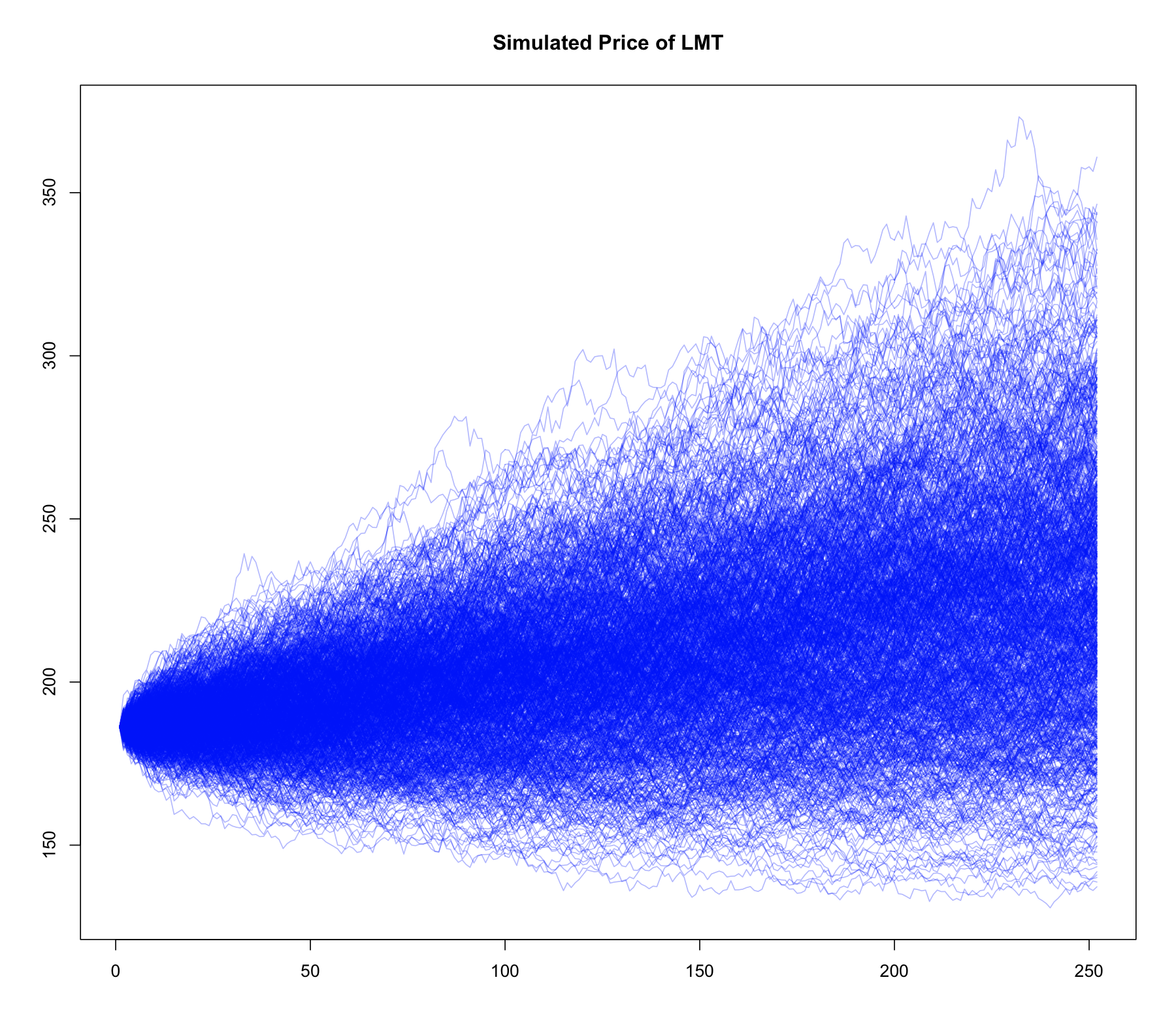

We now simulate 1000 price paths of one year (250 trading days) starting on Jan 2, 2015:

> nSim = 1000

> nDays = 252

> S0 = 186.21 # price on Jan 2, 2015

> S = matrix(0,nrow=nDays,ncol=nSim)

> for(ix in 1:nSim){

+ SVec = rep(0,nDays)

+ SVec[1] = S0

+ for(jx in 2:nDays){

+ DeltaS = mu*SVec[jx-1] + sigma*SVec[jx-1]*rnorm(1)

+ SVec[jx] = SVec[jx-1]+DeltaS

+ }

+ S[,ix] = SVec

+ }

> matplot(S,type='l',col=rgb(0,0,1,0.3),lty=1,ylab='',main='Simulated Price of LMT')

Ito’s Lemma¶

Suppose \(\smash{X}\) follows and Ito process:

For some function \(\smash{G(X,t)}\), Ito’s lemma says:

Ito’s Lemma¶

Ito’s lemma says that \(\smash{G(X,t)}\) is an Ito process with drift and variance rates

Ito’s Lemma for Geometric Brownian Motion¶

Recall our model for stock prices:

In this case, Ito’s lemma says that \(\smash{G(S,t)}\) follows:

Application to Forward Contracts¶

Recall the formula for the value of a forward contract (given current time \(\smash{t}\) and horizon \(\smash{T-t}\)):

- In this case \(\smash{F = G(S,t)}\).

The derivatives are

Application to Forward Contracts¶

Following Ito’s lemma,

Distribution of Prices¶

What is the distribution of \(\smash{S}\) if it follows geometric Brownian motion?

- We know that returns, \(\smash{\frac{dS}{S}}\), are Normal.

Let’s use Ito’s lemma to derive the law of motion of \(\smash{G(S,t) = \ln(S)}\):

- \(\smash{\ln(S)}\) follows a generalized Wiener process with drift rate \(\smash{\mu - \frac{\sigma^2}{2}}\) and variance rate \(\smash{\sigma^2}\).

Distribution of Prices¶

The discrete analog to the process for \(\smash{\Delta \ln(S)}\) is

For \(\smash{\Delta t = T}\), \(\smash{\Delta \ln(S) = \ln(S_T) - \ln(S_0)}\), which results in:

- This means that prices are lognormally distributed.

Lognormal Distribution¶

Suppose \(\smash{S_T \sim LN\left(\ln(S_0) + \left(\mu - \frac{\sigma^2}{2}\right)T, \sigma \sqrt{T}\right)}\).

- By defintion, this means \(\smash{\ln(S_T) \sim N\left(\ln(S_0) + \left(\mu - \frac{\sigma^2}{2}\right)T, \sigma \sqrt{T}\right)}\).

- It can be shown that the mean and variance of \(\smash{S_T}\) are

Simulation Distribution¶

We can check that our simulated geometric Brownian motion results in a lognormal distribution for LMT prices.

> lnMean = S0*exp(mu*nDays)

> lnSD = S0*exp(mu*nDays)*sqrt(exp((sigma^2)*nDays)-1)

> cat(lnMean,mean(S[nDays,]))

228.019 230.529

> cat(lnSD,sd(S[nDays,]))

40.97119 43.21174

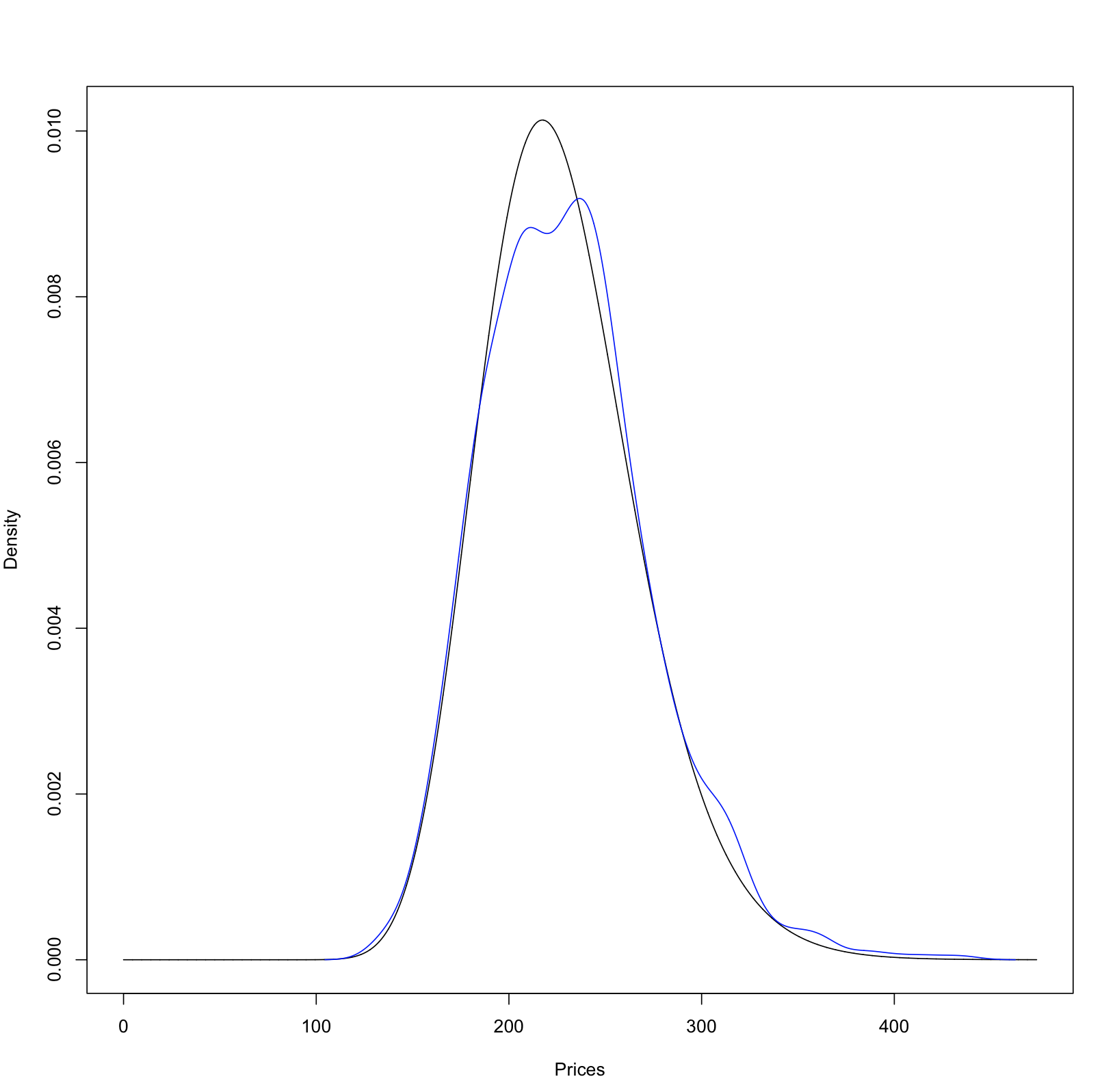

Simulation Distribution¶

We can also plot the theoretical lognormal and the empirical distribution of LMT prices.

> meanOfLog = log(S0) + (mu-(sigma^2)/2)*nDays

> sdOfLog = sigma*sqrt(nDays)

> priceGrid = seq(0,lnMean+6*lnSD,length=10000)

> theoreticalDens = dlnorm(priceGrid,meanOfLog,sdOfLog)

> empiricalDens = density(S[nDays,])

> plot(priceGrid,theoreticalDens,type='l',xlab='Prices',ylab='Density')

> lines(empricalDens,col='blue')