Forward Rate Agreements¶

Zero Rates¶

A zero rate for maturity \(\smash{T}\) is the annual rate of interest earned on a \(\smash{T}\) period investment.

- There is a single payment at the end of the investment (no intermediate payments).

- It is sometimes called the spot rate.

- It is equivalent to the yield on a zero-coupon bond.

Zero Coupon Bond¶

Suppose that the price of a 3-year zero-coupon bond is 97-05.

The continuously-compounded 3-year zero rate is

\[\begin{split}\begin{align} 97.15625 e^{r_3 3} & = 100 \\ \Rightarrow r_3 & = \frac{1}{3} \left(\log(100) - \log(97.15625)\right) \\ & = 0.00961656. \end{align}\end{split}\]

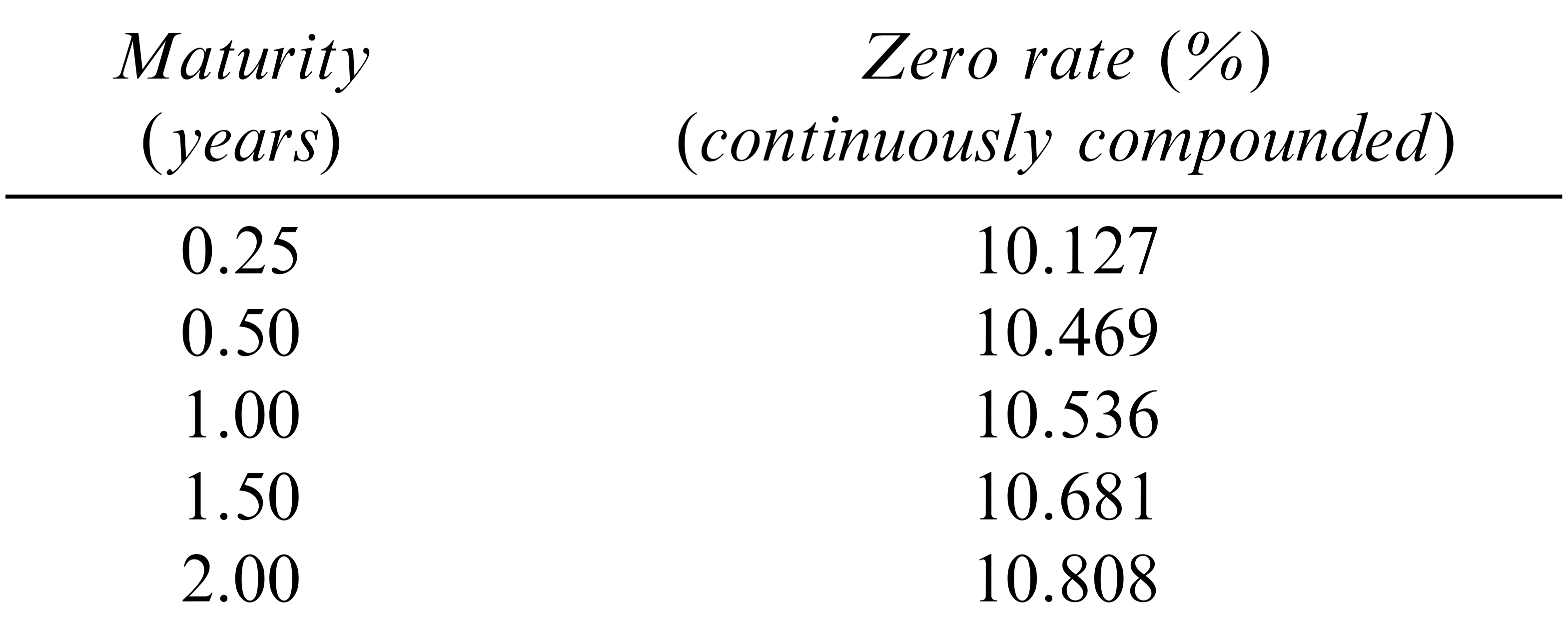

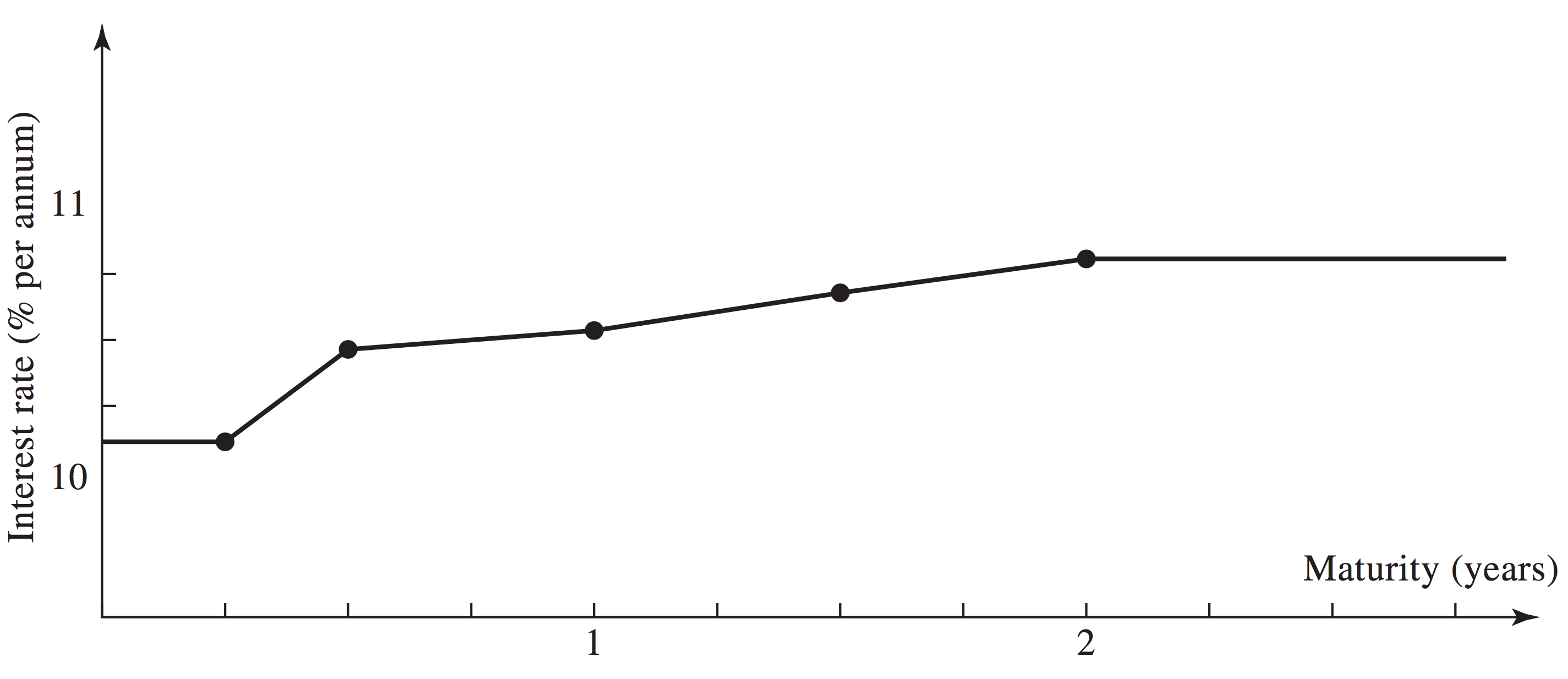

Zero Curve¶

Zero Curve¶

Forward Rates¶

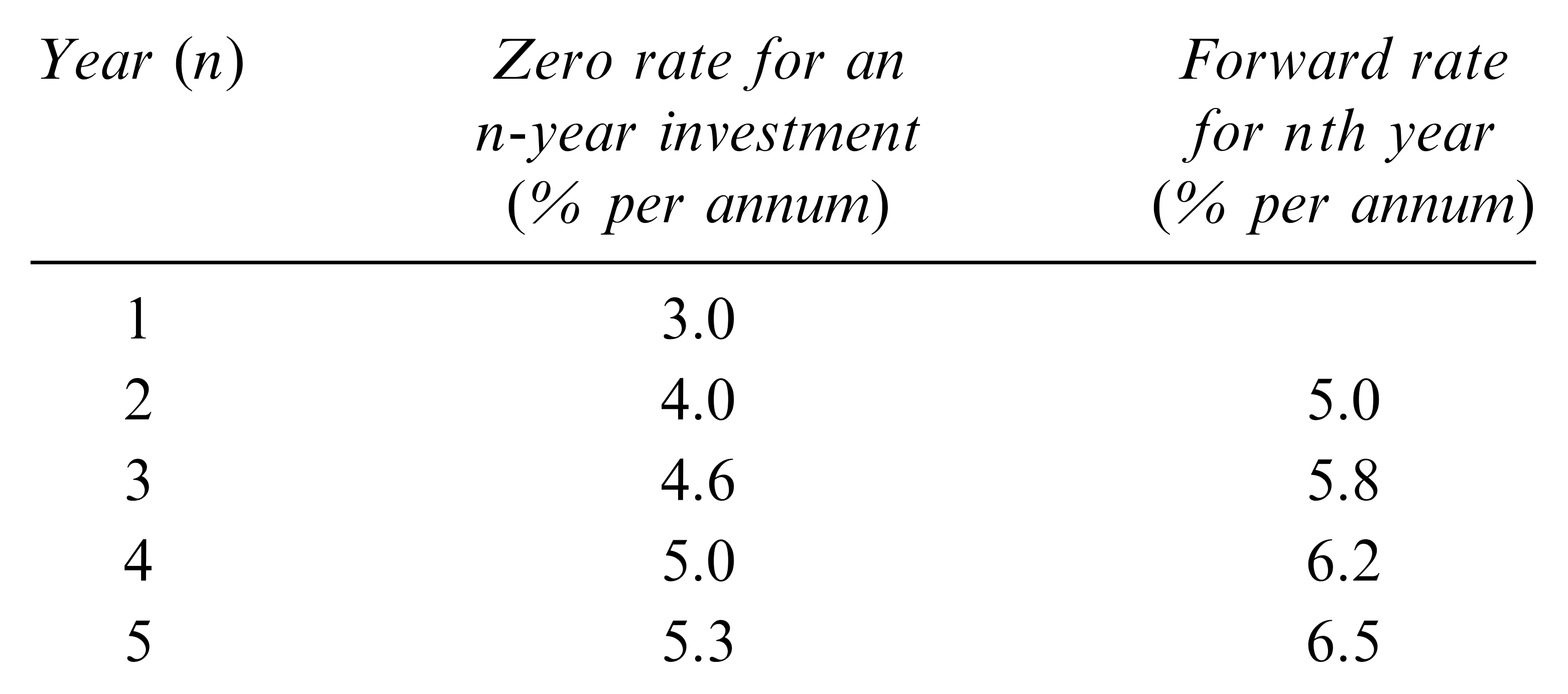

Forward rates are future spot rates implied by current spot rates. Consider two investments:

- Investment 1: At \(\smash{t_0}\) invest $100 in a \(\smash{t_2}\) year zero coupon bond, earning \(\smash{r_2}\) (continuously compounded).

- Investment 2: At \(\smash{t_0}\) invest $100 in a \(\smash{t_1}\) year zero coupon bond (where \(\smash{t_2 > t_1}\)), earning \(\smash{r_1}\), and at \(\smash{t_1}\) roll the proceeds into a \(\smash{t_2-t_1}\) year zero coupon bond.

- The forward rate is the spot rate that would have to prevail at \(\smash{t_1}\) for the investments to be equal.

Forward Rate Example¶

Forward Rates: Alternative¶

Rearranging the forward rate formula:

- If the zero-curve is upward sloping between \(\smash{t_1}\) and \(\smash{t_2}\), \(\smash{r_f > r_2 > r_1}\).

- If the zero-curve is downward sloping between \(\smash{t_1}\) and \(\smash{t_2}\), \(\smash{r_f < r_2 < r_1}\).

Notes on Forward Rates¶

- Spot rates are currently available interest rates for investments of different maturities.

- Forward rates are implied future spot rates for a single maturity.

- Forward rates are not the same as future spot rates.

- They are guaranteed rates for the future period, obtained by investing in current spot rates of differing maturities.

Forward Rate Agreements¶

A Forward Rate Agreement (FRA) is a contract to fix an interest rate for borrowing/lending on a specific principal amount for a specific period of time.

- The contract is over the counter.

- The benchmark interest rate is typically LIBOR.

- If LIBOR is below the contracted rate at maturity, the borrower pays the interest differential on the principal to the lender and vice versa.

- The principal and time period are variables.

- Interest is due at end of period, but present value typically paid at beginning.

FRA Example¶

A company enters into an FRA to receive 4% on $100m for a 3-month period starting in 3 years.

If LIBOR is 4.5% in 3 years, cash flow to the lender at 3.25 years is:

\[\smash{100,000,000 \times (0.04 - 0.045) \times 0.25 = -\$125,000.}\]

The present value is paid at year 3:

\[- \frac{125,000}{1+0.045 \times 0.25} = -123,609.\]

- Note that for FRAs, interest rates are typically not quoted with continuous compounding, but with compounding frequency equal to term of agreement.

FRAs vs Eurodollar Futures¶

FRAs and Eurodollar futures are similar.

- Both fix an interest rate for a future period of time, tied to LIBOR.

- Eurodollar futures are exchange traded, $1m principal and 3-month LIBOR.

- FRAs are over the counter, variable principal, variable term.

- Eurodollar futures commit to pay the difference of principal and interest payment at beginning of period.

- FRAs commit to pay interest differential on principal at end of period.

FRA Notation¶

Suppose an FRA is set so that company \(\smash{X}\) lends to \(\smash{Y}\) between \(\smash{T_1}\) and \(\smash{T_2}\).

- \(\smash{R_K}\): Fixed interest rate set in FRA.

- \(\smash{R_F}\): Forward LIBOR rate (determined today) between \(\smash{T_1}\) and \(\smash{T_2}\).

- \(\smash{R_M}\): Actual LIBOR observed at \(\smash{T_1}\).

- \(\smash{L}\): Principal.

FRA Cash Flows¶

At \(\smash{T_2}\) the cash flow from \(\smash{Y}\) to \(\smash{X}\) (possibly negative):

If settled at time \(\smash{T_1}\), the present value is:

FRA Valuation¶

An FRA is worth zero if \(\smash{R_K = R_F}\).

- At inception, \(\smash{R_K}\) is set equal to \(\smash{R_F}\) and the FRA has zero value.

- As time elapses, \(\smash{R_F}\) fluctuates and the value of the FRA changes.

Prior to \(\smash{T_1}\), the value of the FRA is computed by substituting \(\smash{R_F}\) for \(\smash{R_M}\) and computing the present value:

\[\smash{L(R_K-R_F)(T_2-T_1)e^{-R_2T_2}.}\]

- \(\smash{R_2}\) is the continuously compounded risk-free rate.

FRA Valuation Example¶

It is currently Jan 1, 2010.

- On Jan 1, 2009, a company entered into an FRA to receive 5.8% (semi-annual compounding) and pay LIBOR on $100m between July 1, 2011 and Dec 31, 2011.

- The current LIBOR forward rate for July 1 - Dec 31, 2011 is 5% (semi-annual compounding).

- The 2-year risk-free interest rate (continuous compounding) is 4%.

The value of the FRA on Jan 1, 2010 is:

\[\smash{100,000,000 \times(0.058 - 0.050) \times 0.5 \times e^{-0.04\times 2} = \$369,200.}\]