Trading¶

Exchanges¶

Many financial assets today are traded on exchanges.

- The first stock exchange, the Antwerp Bourse, was established in Antwerp, Belgium in 1460.

- Others were established throughout Europe in the 1500s.

- The oldest existing stock exchange is the Amsterdam Stock Exchange, which was established in 1602.

- The Amsterdam Stock Exchange merged with the Paris and Brussels exchanges in 2000 to form Euronext.

- Euronext merged with the New York Stock Exchange (NYSE) in 2007.

Early Trading¶

For centuries, trading of financial assets consisted of exchanging physical certificates.

- The New York Stock Exchange was Conceived in 1792 under a buttonwood tree on Wall Street.

- 24 brokers signed an agreement to exclusively deal with each other.

- They frequently met under the tree on Wall Street to conduct business.

Early Trading¶

Early Trading¶

Electronic Trading¶

In the 1990s, several electronic exchanges were developed.

- These are often referred to as Electronic Communication Networks or ECNs.

- Archipelago was developed at roughly the same time and was later purchased by NYSE (hence the name, NYSE Arca).

High-Frequency Trading¶

Originally electronic systems were simply used for quoting and displaying prices.

- Trades were still executed by hand on the trading floor.

- Eventually, traders started placing orders electronically.

- This led to algorithmic trading: traders not only submitted orders electronically, but wrote software algorithms that executed trades intelligently, depending on market conditions.

- Algorithmic trading has resulted in very fast execution, commonly referred to as high-frequency trading.

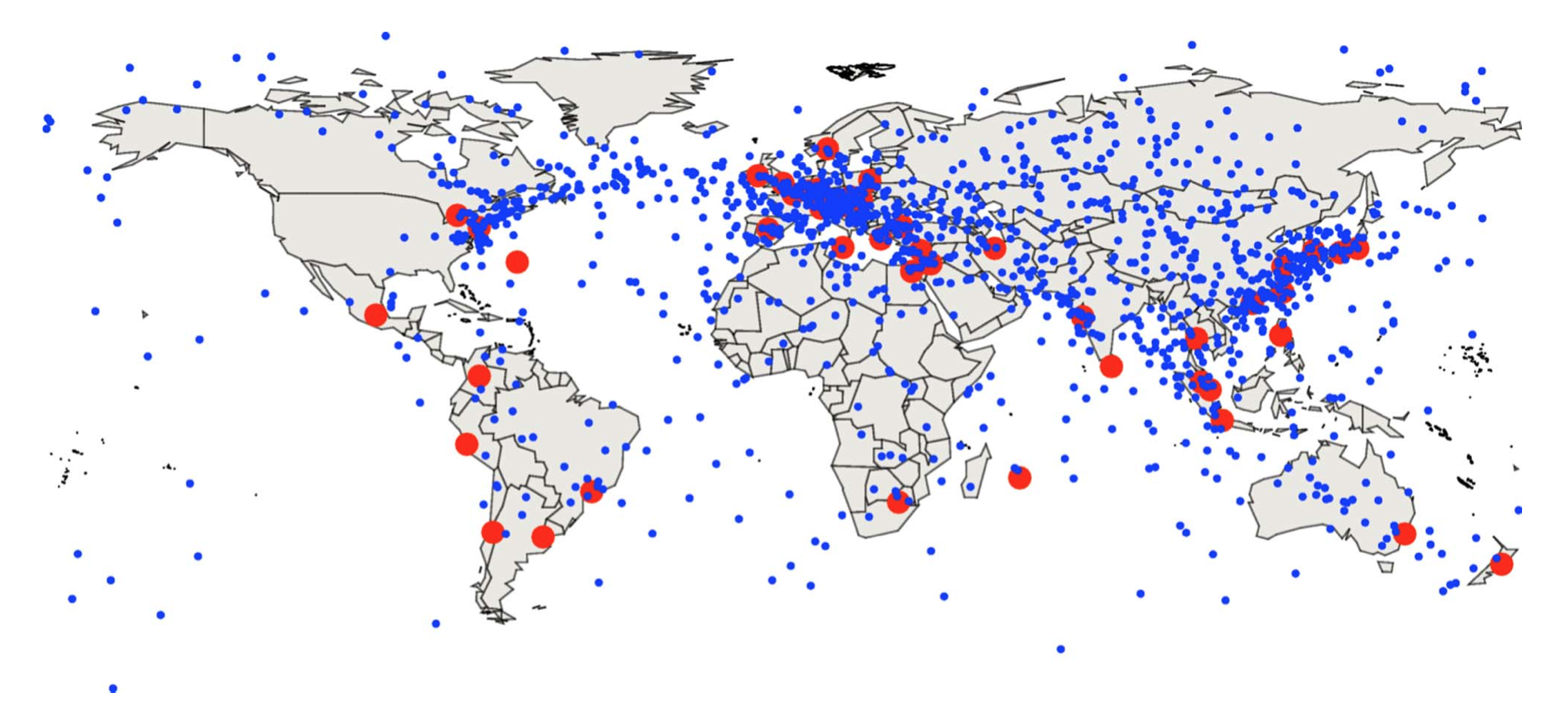

Exchanges Today¶

Exchanges today no longer consist of open floors populated by traders yelling at each other.

- They consist of large warehouses, populated by computer servers that electronically match orders.

- These are referred to as matching engines.

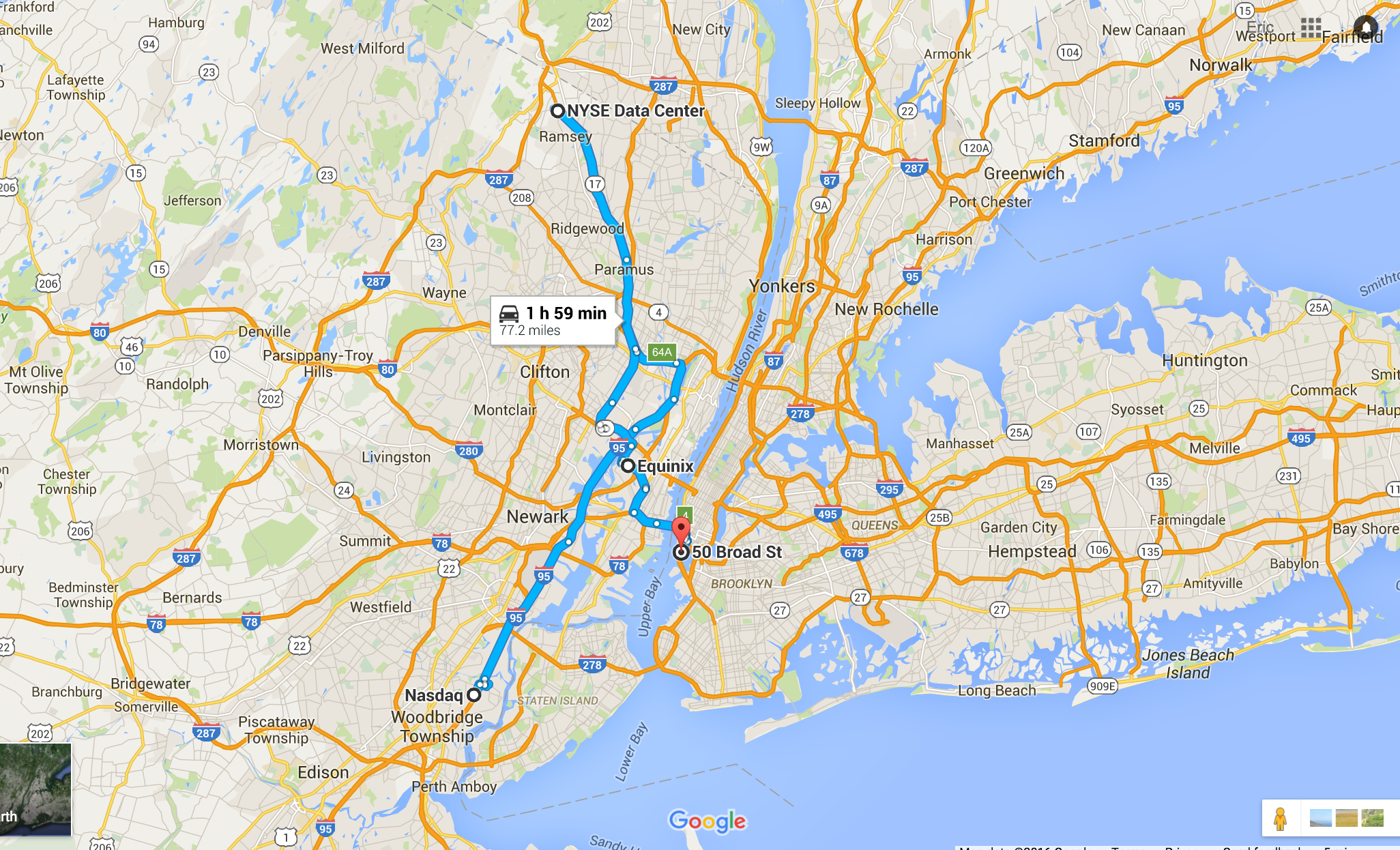

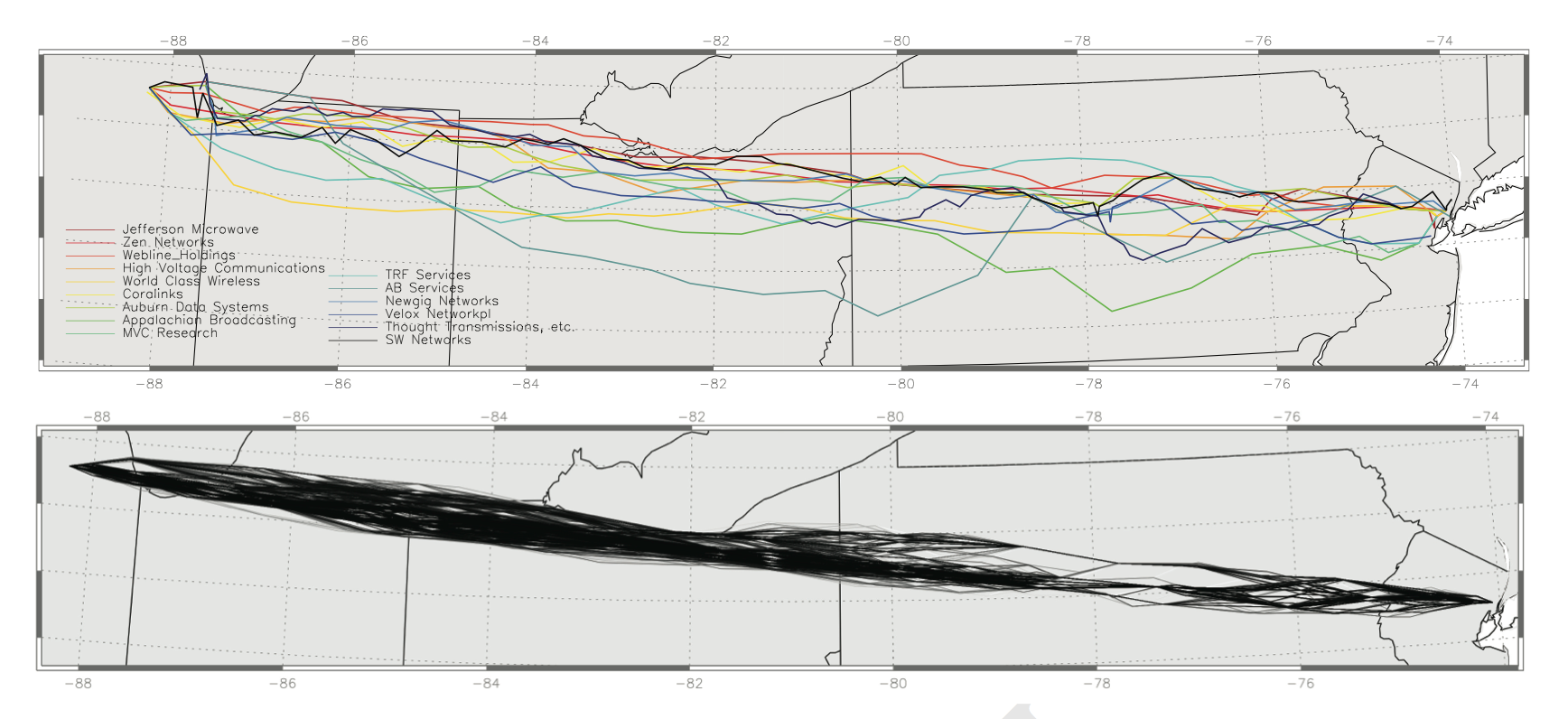

- Since order execution speed is so important, many traders co-locate their trading computers with the matching engines.

Major U.S. Exchanges¶

- The NYSE Arca matching engine is located in Mahwah, NJ.

- The Electronic Broking System (EBS) currency exchange is located in Secausus, NJ.

- The Chicago Board Option Exchange (CBOE) has co-located with EBS in Secaucus.

- The Nasdaq matching engine is located in Carteret, NJ.

- The CME Group matching engine is located in Aurora, IL.

Exchanges Today¶

Exchanges Today¶

Exchanges Today¶

Market Makers¶

Participants on exchanges include makers and takers.

- Makers are required to post both quotes to buy and sell assets on the exchange.

- Quotes to buy are called ‘bids’.

- Quotes to sell are called ‘offers’.

- Typically there are many bids and offers posted on the exchange at different prices.

- Market makers are compensated for providing quotes (also referred to as providing liquidity).

Takers¶

Takers actively take orders that have been passively posted by market makers.

- When a taker wants to buy the asset, the buy at the lowest posted offer quote.

- When a take wants to sell an asset, they sell at the highest posted bid quote.

- The difference between the highest bid quote and lowest offer quote is known as the spread.

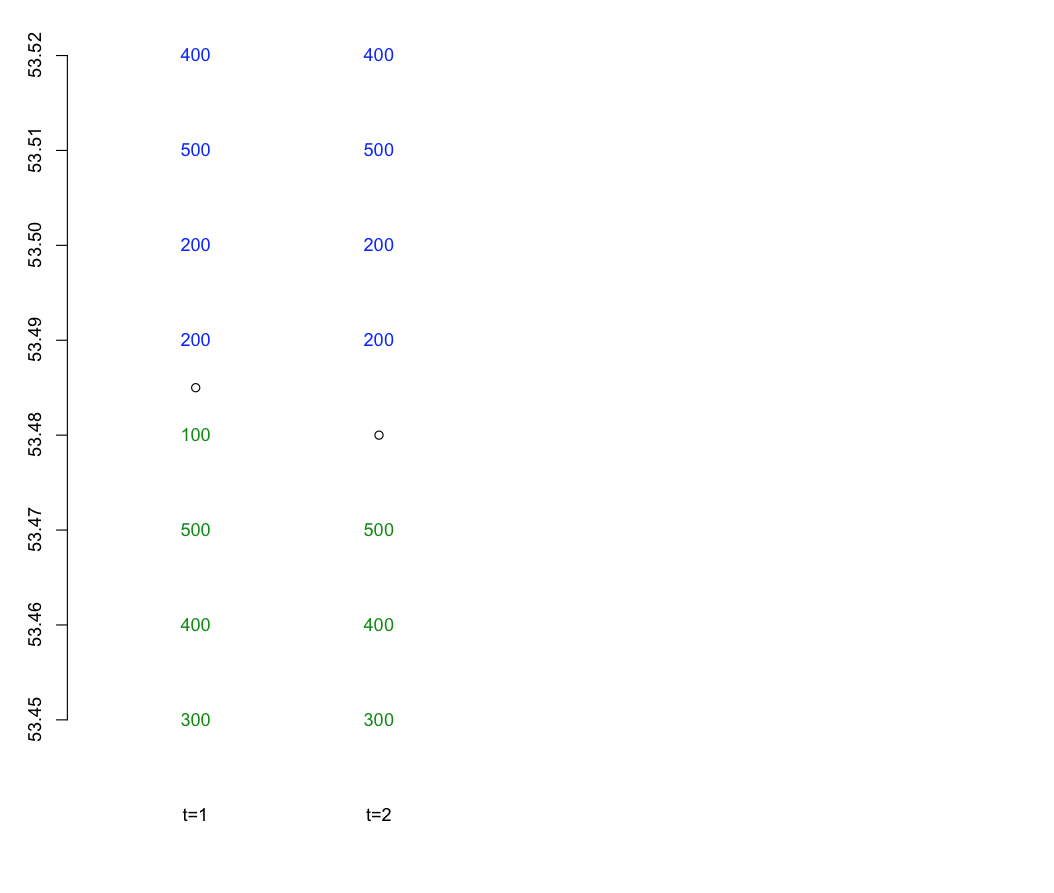

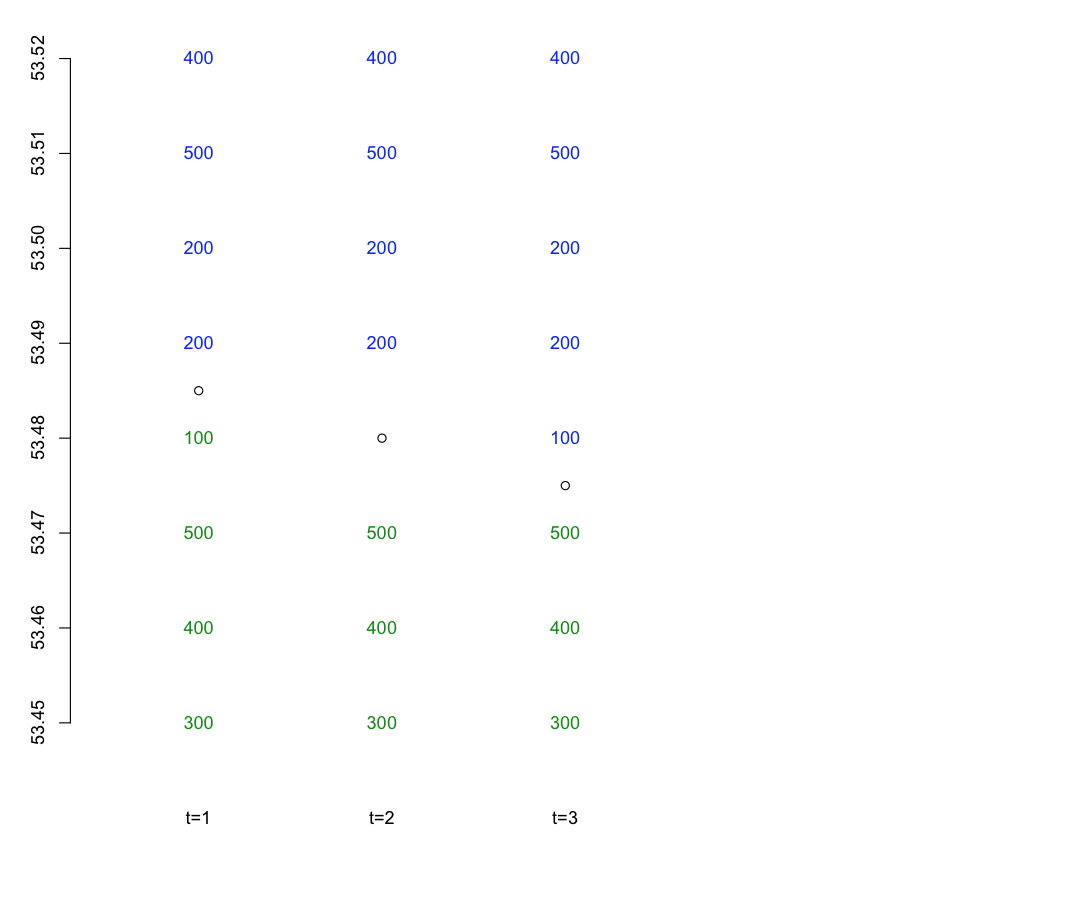

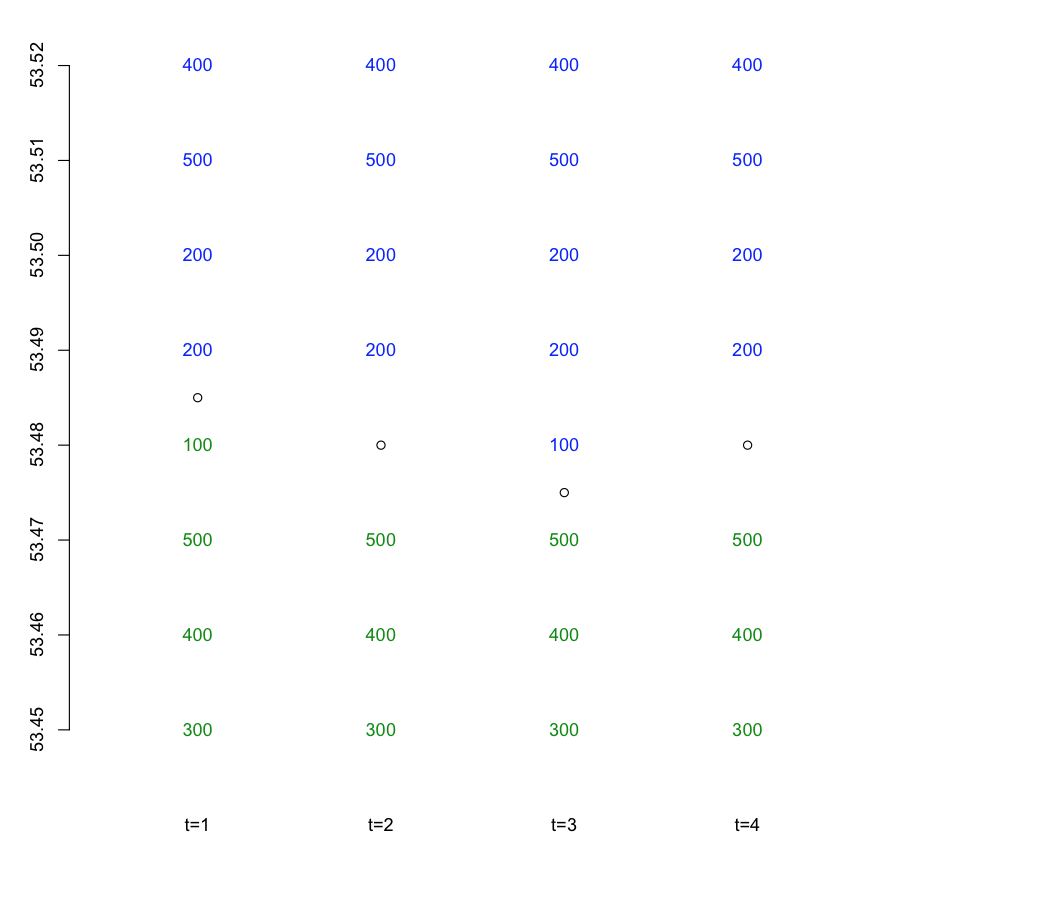

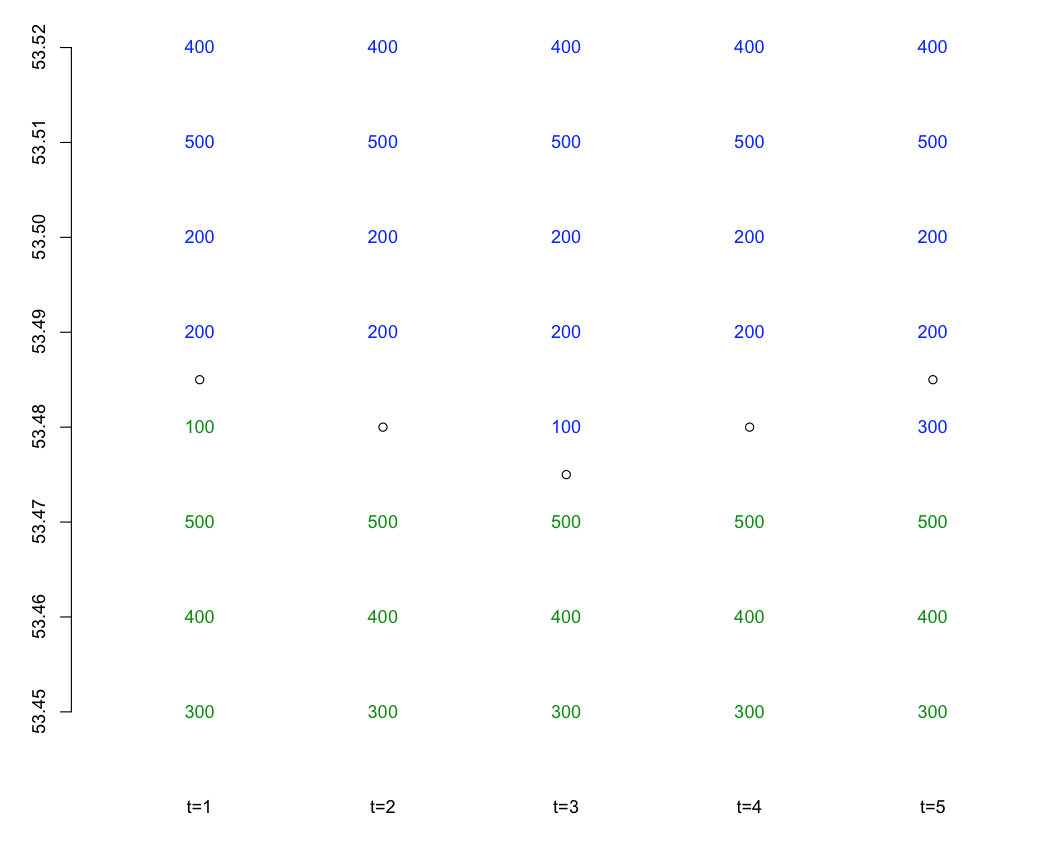

Order Book Example: time 1¶

Order Book Example: time 2¶

Order Book Example: time 3¶

Order Book Example: time 4¶

Order Book Example: time 5¶

Buying on Margin¶

When investors borrow money from a broker to purchase an asset, they are buying on margin.

- The margin is the proportion of the purchase price provided by the investor.

- The purchased securities are maintained in an account by the broker and are monitored.

- The Board of Governors has limited initial margins to be 50% of the initial purchase (i.e. investors must provide at least half of the funds for asset purchase).

Margin Example¶

Suppose an investor has $6000 and would like to buy 100 shares of asset \(W\), currently selling for $100.

- Since $10,000 is required for the purchase, the investor must borrow $4000 from a broker.

- The initial balance sheet would be

| Assets | Liabilities and Owners’ Equity |

|---|---|

| Value of Stock: $10000 | Loan from broker: $4000 |

| Equity: $6000 |

Thus, the initial margin is \(\frac{\$6000}{\$10000} = 0.6\).

Margin Example (Cont.)¶

If the stock price falls to $70 per share, the balance sheet becomes

| Assets | Liabilities and Owners’ Equity |

|---|---|

| Value of Stock: $7000 | Loan from broker: $4000 |

| Equity: $3000 |

The resulting margin is \(\frac{\$3000}{\$7000} = 0.43\).

Maintenance Margin¶

Brokers can set minimal margin requirements, known as maintenance margins.

- If the asset value in the account falls too low, relative to the loan from the broker, the broker can issue a margin call.

- This requires the investor to add cash to the account or liquidate some the stock.

- If the investor doesn’t act accordingly, the broker then has the right to sell some of the stock to pay off enough of the loan to restore the margin to an acceptable level.

Maintenance Margin¶

For example, if a broker has a maintenance margin of 30%, the lowest the price could fall before a margin call is

or P = $57.14.

Why Margins?¶

Margins have the ability to magnify upside returns.

- Suppose asset \(W\) is selling for $100 and an investor believes its price will increase to $120 next period.

- If the investor buys $10,000 worth of stock, she will realize a return of 20% on her money (after one period her net worth will be $12,000).

Why Margins?¶

- However, if the investor borrows an additional $10,000 at 5% interest, then she will earn a gross return of $4000 on the $20,000 invested.

- After repaying $10,500 (loan plus interest), her net return will be

- So the investor was able to increase her return from 20% to 35% by earning a return on borrowed money.

Why Margins?¶

While margins provide the ability to magnify returns, they also increase downside risk exposure.

- Suppose that after borrowing $10,000 from the broker, the price of asset \(W\) fell from $100 to $80.

- The investor’s gross return would be -$4000 on the $20,000 invested.

Why Margins?¶

- After repayment of the loan, the investor’s net return would be

- If the investor hadn’t borrowed money, she would have realized a net return of -0.2. So, by borrowing on margin she has magnified her loss from -20% to -45%.

Short Sales¶

Short sales allow investors to profit from declines in stock prices.

- To engage in a short sale, an investor borrows a share of a stock from a broker and sells it on the market.

- The investor is then obligated to replace the share at a later date.

- If the stock price falls, the investor benefits from selling at a high price and repurchasing at a low price.

- In between, the investor is responsible for paying the broker any dividends that are realized (since the broker would have received these if it hadn’t lent the stock).

Short Sales¶

- When an investor engages in a short sale, we say that they are ‘short’ the stock, or have taken the ‘short position’.

- Conversely, if an investor buys a stock (the usual transaction), we say they are ‘long’, or have taken the ‘long position’.

Short Sale Example¶

Suppose asset \(W\) is selling for $100 and you think its price will fall.

- You decide to borrow 1000 shares, selling them for $100 a piece, yielding a total sale value of $100,000.

- If the stock price falls to $80 per share next period, you can repurchase the 1000 shares for $80,000 and return them to the lender.

- You earn a total of $20,000 in the process.