Bond Prices and Yields¶

Bond Basics¶

A bond is a financial asset used to facilitate borrowing and lending.

- A borrower has an obligation to make pre-specified payments to the lender on specific dates.

Bonds are generally referred to as fixed-income securities.

- Historically, their payments have been fixed.

- In general, they can have variable payments, but those payments are determined by a formula.

- At the end of the bond’s maturity, the borrower pays the face value, or par value of the bond to the lender.

Coupons¶

Typical coupon bonds require the borrower to make semiannual coupon payments to the lender.

- The coupon rate is the total annual amount paid in coupons divided by the face value.

- Zero-coupon bonds pay no coupons - they simply pay the face value at maturity.

- The only way for such assets to be marketable is for their sale value to be below the face value.

Bond Example¶

Suppose a semiannual coupon bond has a face value of $1000 and a coupon rate of 8%.

- The total amount of coupons paid annually is

- Since coupons are paid semiannually, this amount is divided by two.

- So a $40 coupon is paid every six months and $1000 is paid at maturity.

Government Bonds¶

U.S. Government debt assets fall into three categories.

- Treasury bills (T-bills). These pay no coupons and mature in one year or less from the time of issue.

- Treasury notes. These typically pay semiannual coupons and mature in 2 to 10 years from the time of issue (typical maturities are 2, 5 and 10 years).

- Treasury bonds. These typically pay semiannual coupons and mature between 10 to 30 years from the time of issue.

Corporate Bonds¶

U.S. corporations also issue bonds in order to borrow money. These debt instruments are generally quite similar to their government counterparts.

Treasury Inflation Protected Securities¶

Typical bonds offer nominal returns that don’t account for inflation.

- TIPS are bonds whose face values (and hence their coupons) are indexed to the general level of prices.

- If inflation is equal to 2% over the course of a year, the face value of the bond will also rise by 2%.

- The result is a bond with no inflation risk and which should offer a rate of return that is equal to the real, risk-free rate.

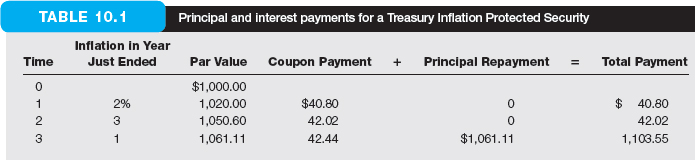

TIPS Example¶

Consider the following bond.

- Face value = $1000.

- Coupon rate = 4%.

- Annual coupon, with three years to maturity.

- Inflation will be 2%, 3% and 1% for the next three years.

TIPS Example¶

We can compute the nominal and real rates of return.

TIPS Example¶

TIPS Example¶

The real rate of return is simply equal to the coupon rate.

- Inflation has been eliminated since the bond’s face value has implicitly incorporated it into the value by tying its face value to increases in prices.

STRIPS¶

STRIPS stands for “Separate Trading of Registered Interest and Principle of Securities”.

- It is a U.S. Treasury program which identifies bond payments as a separate securities.

A coupon paying bond can be “stripped” into multiple assets - each coupon and the face value being marketed as individual zero-coupon bonds.

- A 10 year, semiannual bond is comprised of 20 coupon payments and a final payment of the face value.

- It could be stripped into 21 separate, zero-coupon assets with varying maturities.

Discounting Cash Flows¶

A bond’s value should be equal to the net present value of its cash flows.

- Each payment should be discounted by the product of interest rates over the period of interest.

- For a coupon payment in four years

- \(r_i\) is the interest rate over year \(i\).

Discounting Cash Flows¶

Assuming the interest rate is constant over all periods (\(r_i = r, \forall i\))

Geometric Series¶

The following mathematical result will be useful for deriving the value of a bond:

- For \(|x| < 1\),

Bond Pricing¶

Let \(F\) = Face Value, \(C\) = Coupon Payment and \(V\) = Bond Value.

- Then,

Bond Pricing¶

Bond Pricing¶

We made use of the geometric series result, recognizing \(0 < x = \frac{1}{1+r} < 1\).

Bond Value Formula¶

The bond price formula can be decomposed as

- \(\text{Annuity factor}(r,T)\) is the present value of a $1 annuity that lasts for \(T\) periods with interest rate \(r\).

- \(\text{PV factor}(r,T)\) is the present value of $1 paid in \(T\) periods.

Value vs. Price¶

So far we have only computed the present value of the bond.

- What is its price?

- The bond price should be equal to the present value of payments.

- If the price was lower, you could buy the bond for \(P < V\) and receive the promised cash flow: your net gain would be \(V - P\).

- If the price was higher, you could short the bond for \(P > V\) and pay the promised cash flow: your net gain would be \(P - V\).

Bond Pricing Example¶

Consider a bond with the following characteristics.

- \(F = \$1000\).

- 30 years to maturity.

- 8% coupon rate.

- Semiannual coupons.

Suppose the nominal interest rate is constant at 8% for the next 30 years. Note that

- The coupon payment is $40 every six months.

- There are 60, six-month time periods.

Bond Pricing Example¶

The bond price is

- If the annual interest rate equals the coupon rate, \(P = F\).

If \(r = 0.10\), then

Prices and Yields¶

The return for holding a bond is typically referred to as a yield.

- A central feature of bonds is that prices and yields are negatively related.

- Since a bond promises a fixed payment at maturity, you want to purchase for a very low price.

Prices and Yields¶

Think of a zero-coupon bond that costs \(P\) and pays \(F\) at maturity.

- The yield, \(y\), is the value such that \(P \times (1+y) = F\):

- Note that \(y\) is a net return (not gross).

- Since the bond price is in the denominator, \(y\) and \(P\) have an inverse relationship: higher prices mean lower yields.

- This relationship holds for coupon bonds as well (as seen in the bond pricing formula in Equation (1)).

Prices and Yields¶

Consider a zero-coupon bond with a face value of $1000 and one period until maturity.

- If \(P = \$990\), the yield is

- If \(P = \$995\), the yield is

Coupon Rate and Yield¶

We saw above that if the market interest rate \(r\) is equal to the coupon rate, \(P = F\).

- Consider two competing investments: put your money in a savings account that pays \(r\) each period, or buy a bond.

- If the coupon rate is exactly equal to \(r\), then the bond exactly compensates you for market return and does not need to provide price appreciation.

Coupon Rate and Yield¶

- If the coupon rate is less than \(r\), the bond does not compensate you enough - to be competitive, it must sell at a discount (less than the face value).

- If the coupon rate is greater than \(r\), the bond overcompensates you - to be competitive, it can sell at a premium (more than the face value).

Coupon Rate and Yield¶

Why would a borrower sell a bond at a discount when \(r\) is greater than the coupon rate?

- Because nobody would buy the bond unless the price formula holds.

Coupon Rate and Yield¶

Later, the bond price will fluctuate on the secondary market.

- If the market rate rises, investors will sell the bond (because of

its low coupon).

- The price will fall until the overall return is commensurate with the market return.

- If the market rate falls, investors will buy the bond

(because of its high coupon).

- The price will rise until the overall return is commensurate with the market return.

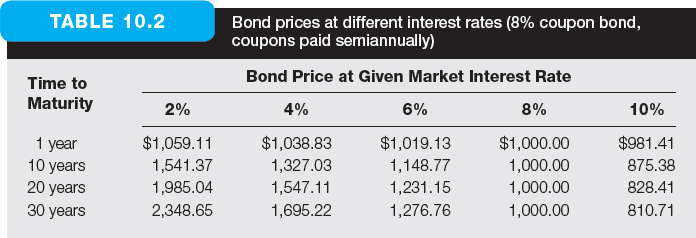

Interest Rate Risk¶

Unfortunately, interest rates don’t remain constant.

- Suppose you purchase a bond for the face value when the coupon rate and market interest rates are equal.

- If the market rate suddenly rises, you will have your money tied up in an investment paying a rate that is too low (opportunity cost).

- If you sell the bond on the secondary market, the price will be lower than the face (your purchase price) because \(r\) is greater than the coupon rate.

Interest Rate Risk¶

The opposite would be true if the market rate falls.

- As a result, bond holders are subject to interest rate fluctuations, or interest rate risk.

Maturity Risk¶

Interest rate risk is exacerbated over longer maturities.

- Suppose the market interest rate moves after you purchase two bonds with 10 and 30 years to maturity.

- If the market rate rises you will suffer a greater loss on the 30 year bond since your money is tied to it for a longer period.

- As a result, prices of longer maturity bonds are more sensitive to interest rate movements.

Bond Prices Over Time¶

As a bond approaches maturity, its price will approach the face value.

- Fewer payments are subject to interest rate fluctuations.

- This is true whether the bond sells at a premium or discount.

Bond Prices Over Time¶

Consider buying a bond the day before maturity.

- If a coupon is paid at maturity, you only receive a prorated share of the coupon (one day’s worth).

- Net of the prorated coupon, you should pay only the slightest discount to face value.

- The slight discount arises because you can invest your money overnight and earn a small amount of interest.