The Term Structure of Interest Rates¶

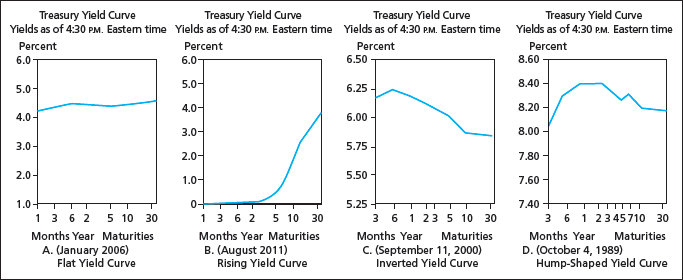

Yield Curve¶

Bonds of different maturities often have different yields to maturity.

- The relationship between yield and maturity is summarized graphically in the yield curve.

- Consider several examples below.

\(\qquad\)

Yield Curve Slope¶

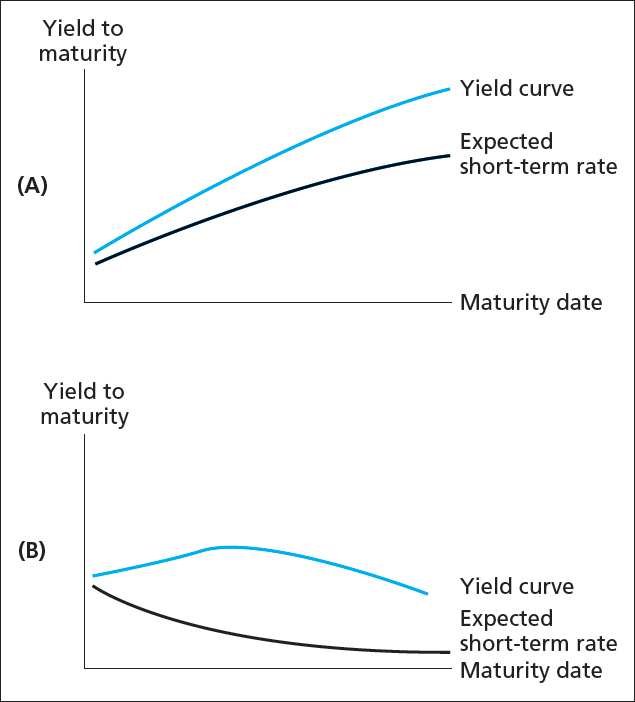

An upward sloping yield curve is evidence that short-term interest rates are going to rise.

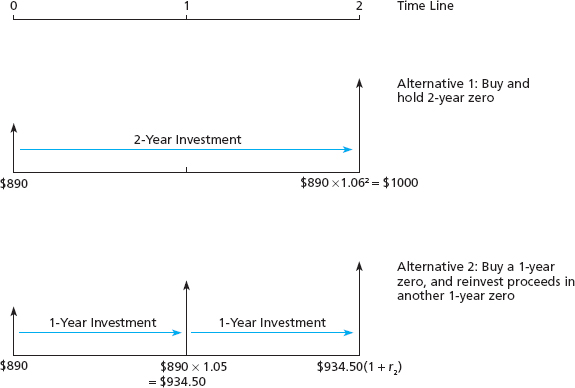

Consider two investment strategies.

- Buy and hold a two-year zero-coupon bond, offering 6% return each year.

- Buy a one-year bond today, offering a 5% return over the coming year, and roll the investment into another one-year zero-coupon bond a year from now, offering an interest rate of \(r_2\).

- These investments should be equivalent. Why?

Yield Curve Slope¶

Suppose you begin with $890 to invest (the price of a two-year zero-coupon bond with 6% YTM.

- Equating the returns to each strategy gives:

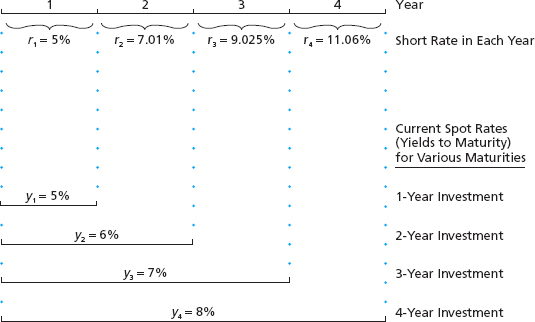

Spot Rates and Short Rates¶

We distinguish between two types of interest rates.

- Spot rate: the rate offered today on zero-coupon bonds of

different maturities.

- In the previous example, the one-year spot rate is 5% and the two year spot rate is 6%.

- Short rate: the rate for given time interval (one year) offered at

different points in time.

- In the previous example, the first-year short rate is 5% (same as the spot!) and the second-year short rate is 7.01%.

Spot Rates and Short Rates¶

The spot rate for a given period should be the geometric average of short rates over that interval.

- Let \(y_2\) be the two-year spot rate.

- Let \(r_1\) and \(r_2\) be the first-year and second-year short rates.

- Don’t forget that \(y_1 = r_1\).

Spot Rates and Short Rates¶

So, if the yield curve slopes up (\(y_2 > y_1 = r_1\)), we conclude that short-term rates will rise (\(r_2 > r_1\)).

- Reverse reasoning holds for a downward sloping yield curve.

Spot Rate and Short Rate Example¶

Assume the following spot rates and short rates:

- Spots: \(y_1 = 0.05\), \(y_2 = 0.06\) and \(y_3 = 0.07\).

- Shorts: \(r_1 = y_1\) and \(r_2 = 0.0701\).

- What is the three-year short rate, \(r_3\)?

Spot Rate and Short Rate Example¶

Buying a three-year zero-coupon bond should be identical to buying a two-year zero and rolling into a one-year zero.

Spot Rate and Short Rate Example¶

We know

So the full decomposition is

General Short Rates¶

We can generalize the previous results.

- Investing in an \(n\) period zero-coupon bond should be the same as investing in an \(n-1\) zero and rolling into a one-period zero at time \(n-1\).

Forward Rates¶

In the development above, we assumed no uncertainty.

- All future rates were known at time zero.

- In reality, we don’t have perfect knowledge of time \(n\) short rates at time zero.

Forward Rates¶

To distinguish between actual short rates that occur in the future, we define the forward rate to be

- The time \(t=n\) forward rate is the break-even interest rate that equates the returns of an n-period zero-coupon bond with an \((n-1)\) -period zero rolled into a one-period zero.

- It may not be equal to the expected future short rate.

Expectations Hypothesis¶

The Expectations Hypothesis of the yield curve says that expected short rates equal forward rates:

- If the yield curve slopes upward, short rates are expected to rise: \(E[r_n] > E[r_{n-1}] > r_1 = y_1\).

- If the yield curve slopes downward, short rates are expected to fall: \(E[r_n] < E[r_{n-1}] < r_1 = y_1\).

Liquidity Preference Theory¶

According to the Liquidity Preference Theory of the yield curve, investors must be compensated for holding longer-term bonds.

- Longer-term bonds are subject to greater risk, and so investors should demand a premium for holding them.

- In reality, a premium means that investors will only buy them for a lower price (which means greater yield).

Liquidity Preference Theory¶

The Liquidity Preference Theory can be expressed as forward rates being equal to expected short rates plus a premium, \(\phi\):

- According to this theory, expected short rates can be constant if the yield curve is upward sloping.

- If the yield curve is downward sloping, expected short rates must be falling. Why?

Liquidity Preference Example¶

Suppose you buy a two-year bond and that

- Short rates for the next two years are constant at 8%: \(r_1 = E[r_2] = 0.08\).

- The liquidity premium for year two is 1%: \(\phi = 0.01\).

Liquidity Preference Example¶

What is the yield to maturity of the two year bond?

- So the yield curve slopes up (\(y_2 > y_1\)) even though expected short rates are constant.

Expectations Hypothesis Example¶

However, if there is no liquidity premium

- Now the yield curve is flat.

Implications of the Theories¶

The slope of the yield curve always determines whether forward rates are rising or falling.

- \(y_2 > y_1\) means \(f_2 > f_1\) (by the definition of forward rates!).

- If the Expectations Hypothesis holds, \(E[r_2] = f_2\), so \(y_2 > y_1\) means \(E[r_2] > r_1 = f_1 = y_1\).

Implications of the Theories¶

If the Liquidity Preference Theory holds, we have no guarantee that \(E[r_2] > r_1\) if \(y_2 > y_1\).

- Short rates could be constant with a moderate liquidity premium.

- Short rates could be rising some, with a small liquidity premium.

- Short rates could be falling, with a large liquidity premium.

- What about if \(y_2 < y_1\)?