Kernel Density Estimation¶

Data Samples¶

Suppose we are presented with a set of data observations \(y_1, y_2, \ldots, y_n\).

- In this course we will often assume that the observations are realizations of random variables \(Y_1, Y_2, \ldots, Y_n\), where \(Y_i \sim F\), \(\forall i\).

- That is, we will assume \(Y_i\) all come from the same distribution.

- In the case of financial data, we will also view the observations \(y_1, y_2, \ldots, y_n\) as being ordered by time.

- This is referred to as a time series.

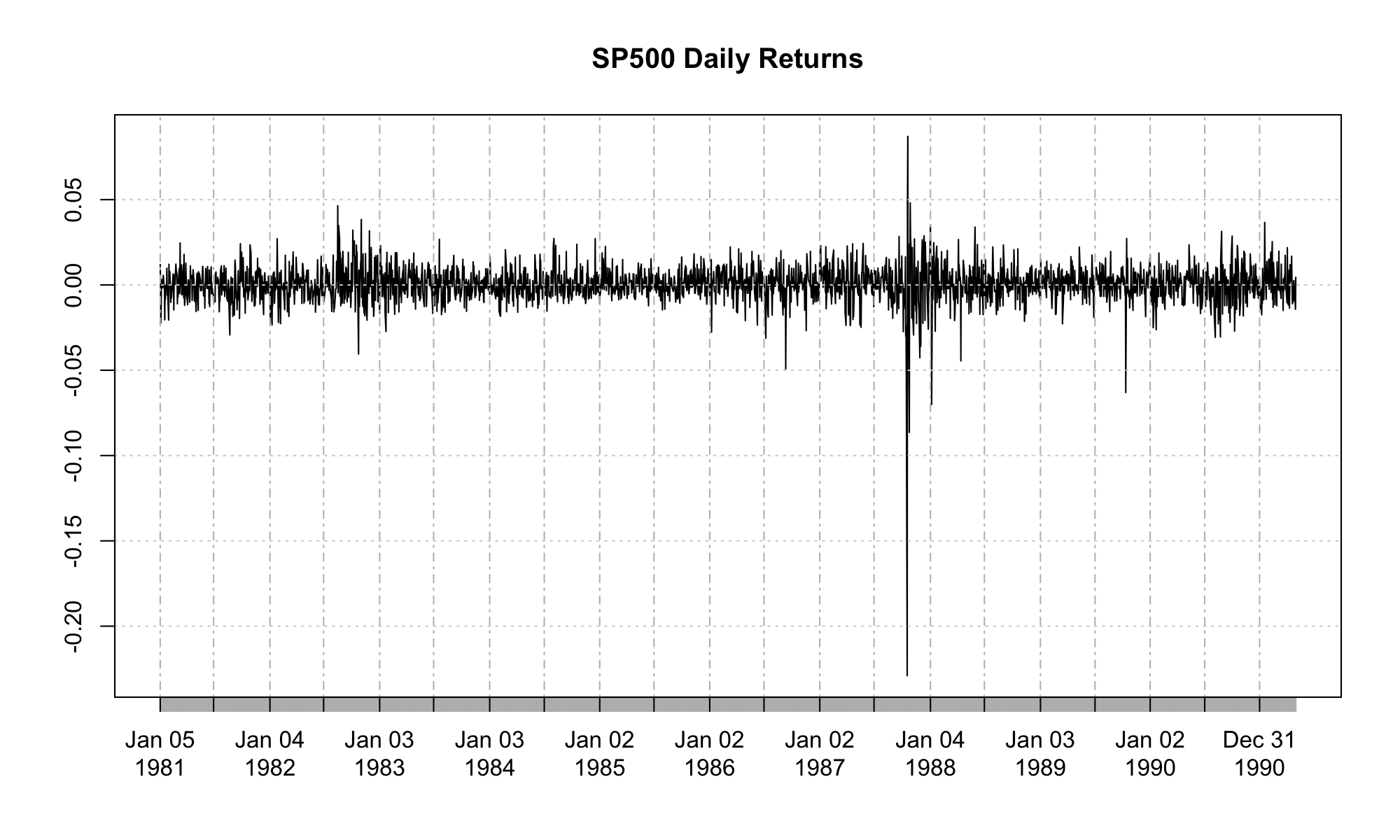

Time Series Data Example¶

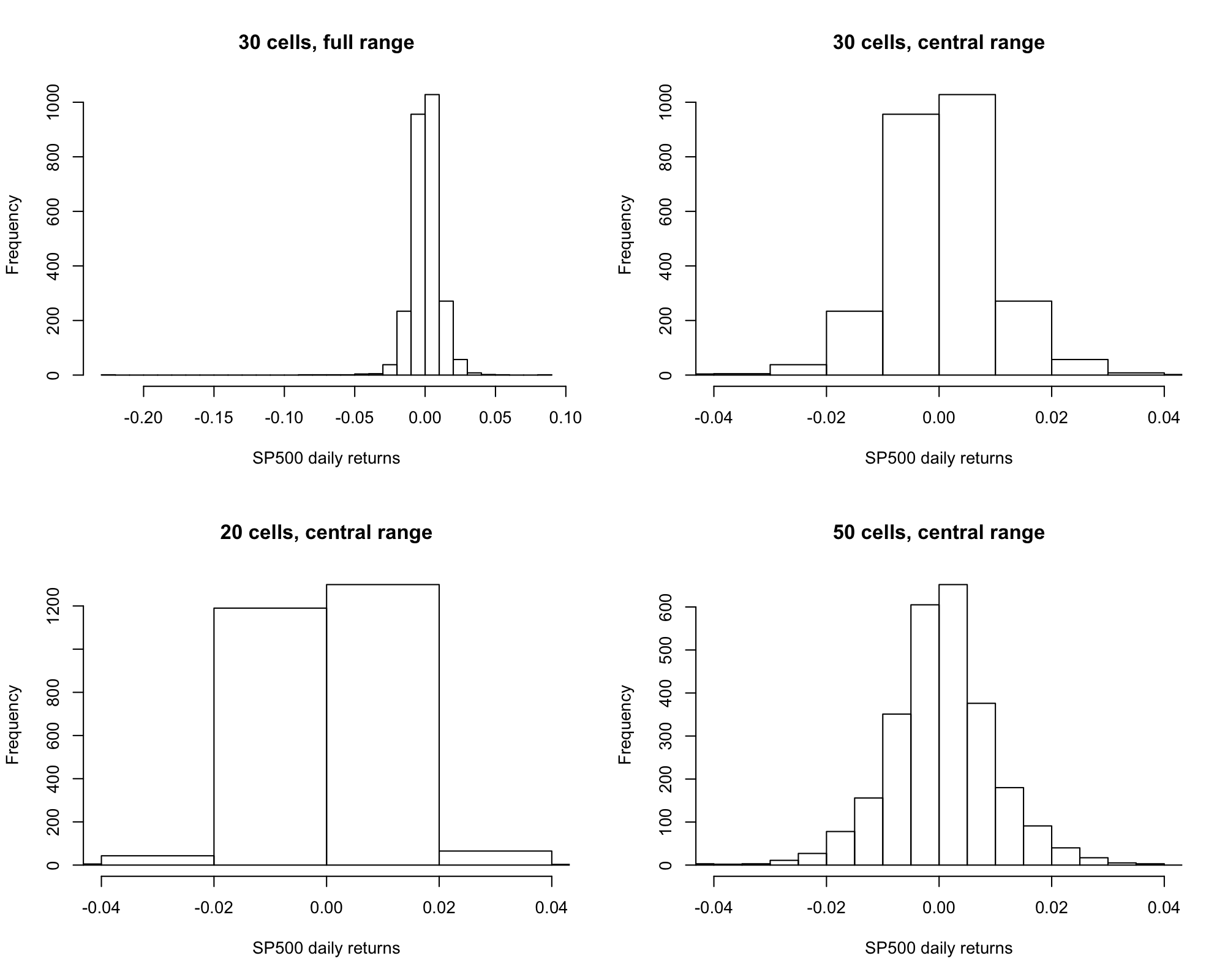

Histogram¶

Suppose we have dataset \(y_1, y_2, \ldots, y_n\) drawn from the same distribution \(F\).

- We typically don’t know \(F\) and would like to estimate it with the data.

- A simple estimate of \(F\) is obtained by a histogram.

A histogram:

- Divides the possible values of the random variable(s) \(y\) into \(K\) regions, called bins.

- Counts the number of observations that fall into each bin.

Histogram of SP500 Daily Returns¶

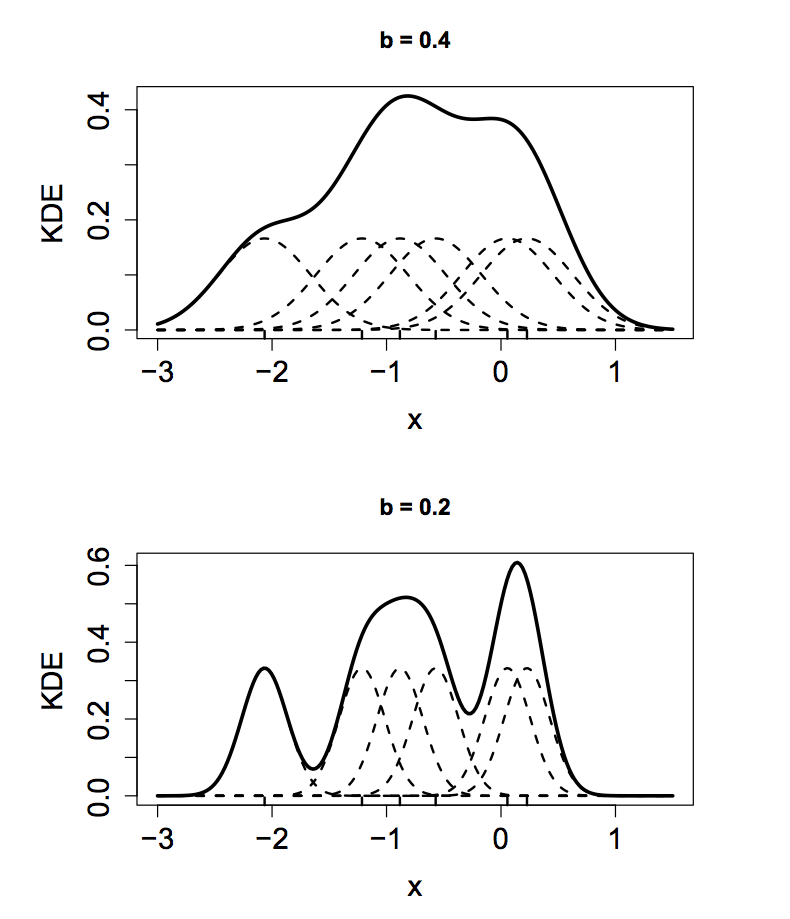

Kernel Density Estimation¶

Histograms are crude estimators of density functions.

- The kernel density estimator (KDE) is a better estimator.

- A KDE uses a kernel, which is a probability density function symmetric about zero.

- Often, the kernel is chosen to be a standard normal density.

- The kernel has nothing to do with the true density of the data (i.e. choosing a normal kernel doesn’t mean the data is normally distributed).

Kernel Density Estimation¶

Given random variables \(Y_1, Y_2, \ldots, Y_n\), the KDE is

Kernel Density Estimation¶

The KDE superimposes a density function (the kernel) over each data observation.

- The bandwidth parameter \(b\) dictates the width of the kernel.

- Larger values of \(b\) mean that the kernels of adjacent observations have a larger effect on the density estimate at a particular observation, \(y_i\).

- In this fashion, \(b\) dictates the amount of data smoothing.

Kernel Density Bandwidth¶

Choosing \(b\) requires a tradeoff between bias and variance.

- Small values of \(b\) detect fine features of the true density but permit a lot of random variation.

- The KDE has high variance and low bias.

- If \(b\) is too small, the KDE is undersmoothed or overfit - it adheres too closely to the data.

Kernel Density Bandwidth¶

- Large values of \(b\) smooth over random variation but obscure fine details of the distribution.

- The KDE has low variance and high bias.

- If \(b\) is too large, the KDE is oversmoothed or underfit - it misses features of the true density.

KDE of S&P 500 Daily Returns¶

KDE of S&P 500 Daily Returns¶

The KDE of the S&P 500 returns suggests a density that resembles a normal distribution.

- We can compare the KDE with a normal distribution with \(\mu = \hat{\mu}\) and \(\sigma^2 = \hat{\sigma}^2\), where

KDE of S&P 500 Daily Returns¶

- We can also compare the KDE with a normal distribution with \(\mu = \tilde{\mu}\) and \(\sigma^2 = \tilde{\sigma}^2\)

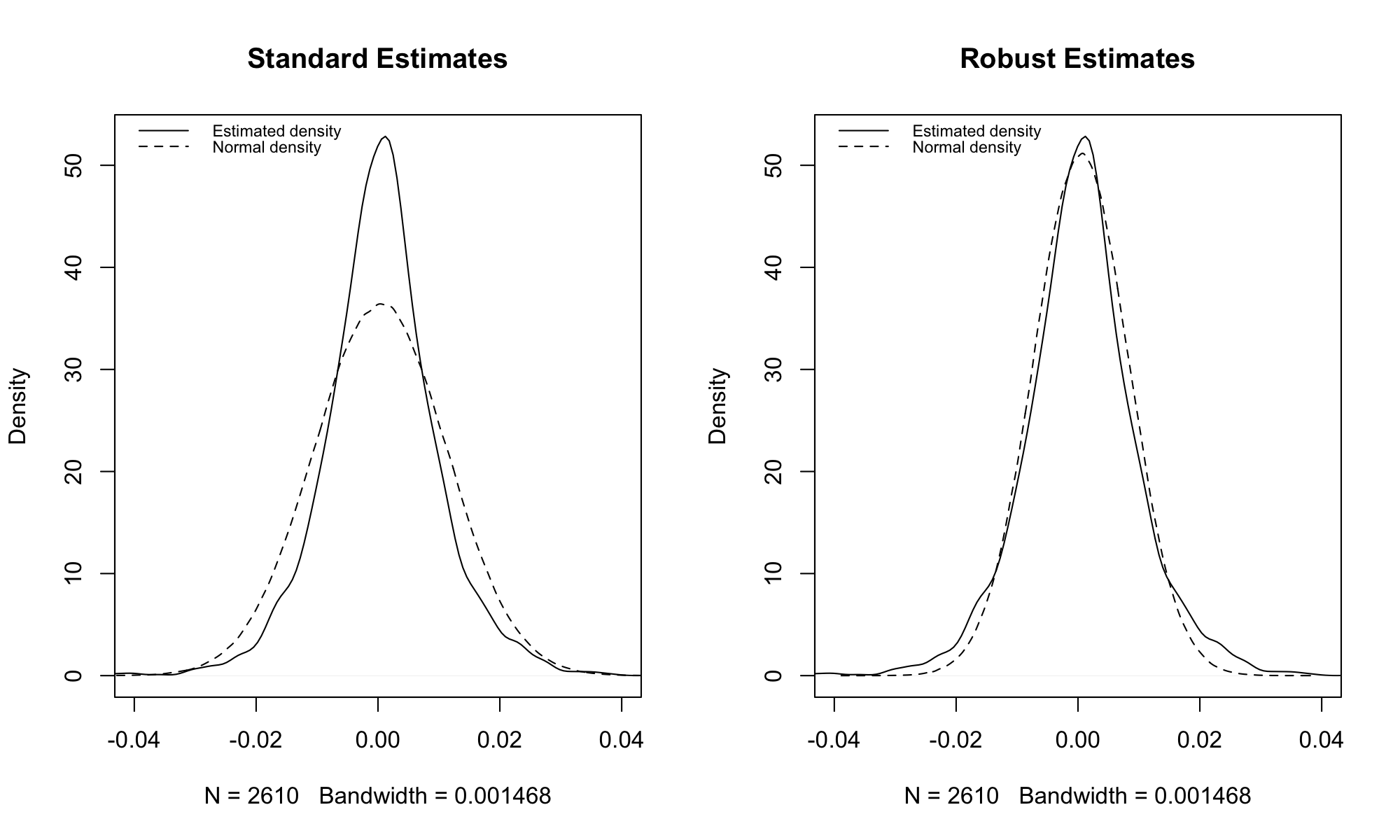

Comparison of KDE with Normal Densities¶

Comparison of KDE with Normal Densities¶

Outlying observations in the S&P 500 returns have great influence on the estimates \(\hat{\mu}\) and \(\hat{\sigma}^2\).

- As a result, a \(N(\hat{\mu}, \hat{\sigma})\) deviates substantially from the KDE.

The median, \(\tilde{\mu}\), and median absolute deviation, \(\tilde{\sigma}^2\), are less sensitive (more robust) to outliers.

- As a result, a \(N(\tilde{\mu}, \tilde{\sigma})\) deviates less from the KDE.

- The fit is still not perfect - asset returns are often better approximated with a heavy tailed distribution, like the \(t\).