Heavy-Tailed Distributions¶

Heavy-Tailed Distributions¶

Observed data often do not conform to a Normal distribution.

- In many cases, extreme values are more likely than would be dictated by a Normal.

- This is especially true of financial data.

- In this lecture, we will study several examples of distributions with heavy tails, which assign higher probability to extreme values.

Generalized Error Distributions¶

Suppose that \(X\) follows a Generalized Error Distribution with shape parameter \(\nu: \,\, X \sim GED(\nu)\).

- Then for \(x \in (-\infty, \infty)\),

Generalized Error Distributions¶

- \(\lambda_{\nu}\) and \(\kappa(\nu)\) are constants and are chosen so that the density integrates to unity and has unit variance.

- The shape parameter \(\nu > 0\) determines tail weight.

Generalized Error Distributions¶

For many distributions, the scaling constants are simply a nuisance.

- We can focus attention on only the part of the function that relates to values of the random variable.

- Disregarding constants, we say that the density is proportional to:

- As \(x \to \infty\), \(-|x|^{\nu} \to -\infty\) faster for larger values of \(\nu\).

- This means that as \(x \to \infty\), \(f_{X}(x|\nu) \to 0\) faster for larger values of \(\nu\).

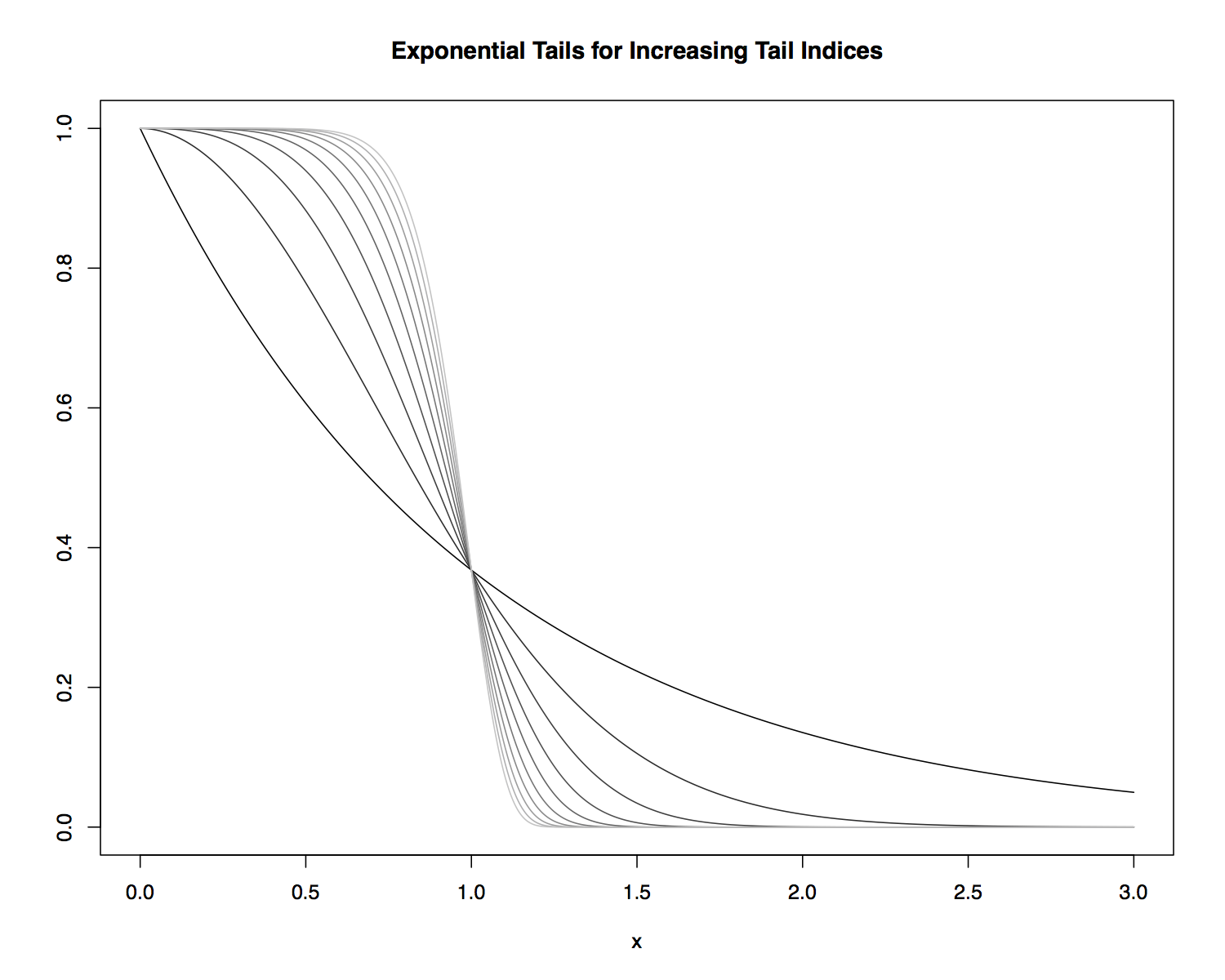

Exponential Tails¶

For generalized error distributions, larger values of \(\nu\) correspond to lighter tails and smaller values to heavier tails.

- We say that the generalized error distribution has exponential tails, since the tails diminish exponentially as \(x \to \infty\) and \(x \to -\infty\).

Exponential Tails¶

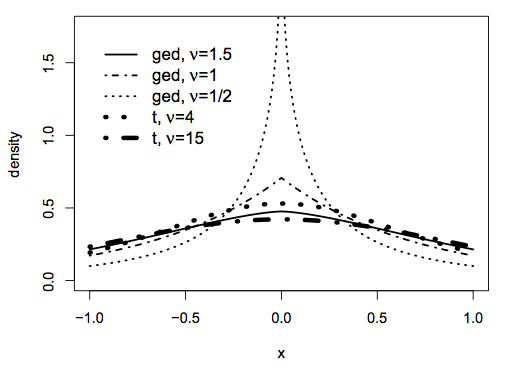

Generalized Error Distribution Examples¶

Special cases of generalized error distributions:

- \(\nu = 2\): \(\mathcal{N}(0,1)\).

- \(\nu = 1\): Double-exponential distribution.

- The double-exponential distribution has heavier tails than a standard normal since its shape parameter is smaller.

- Heavier tails that the double-exponential are obtained with \(\nu < 1\).

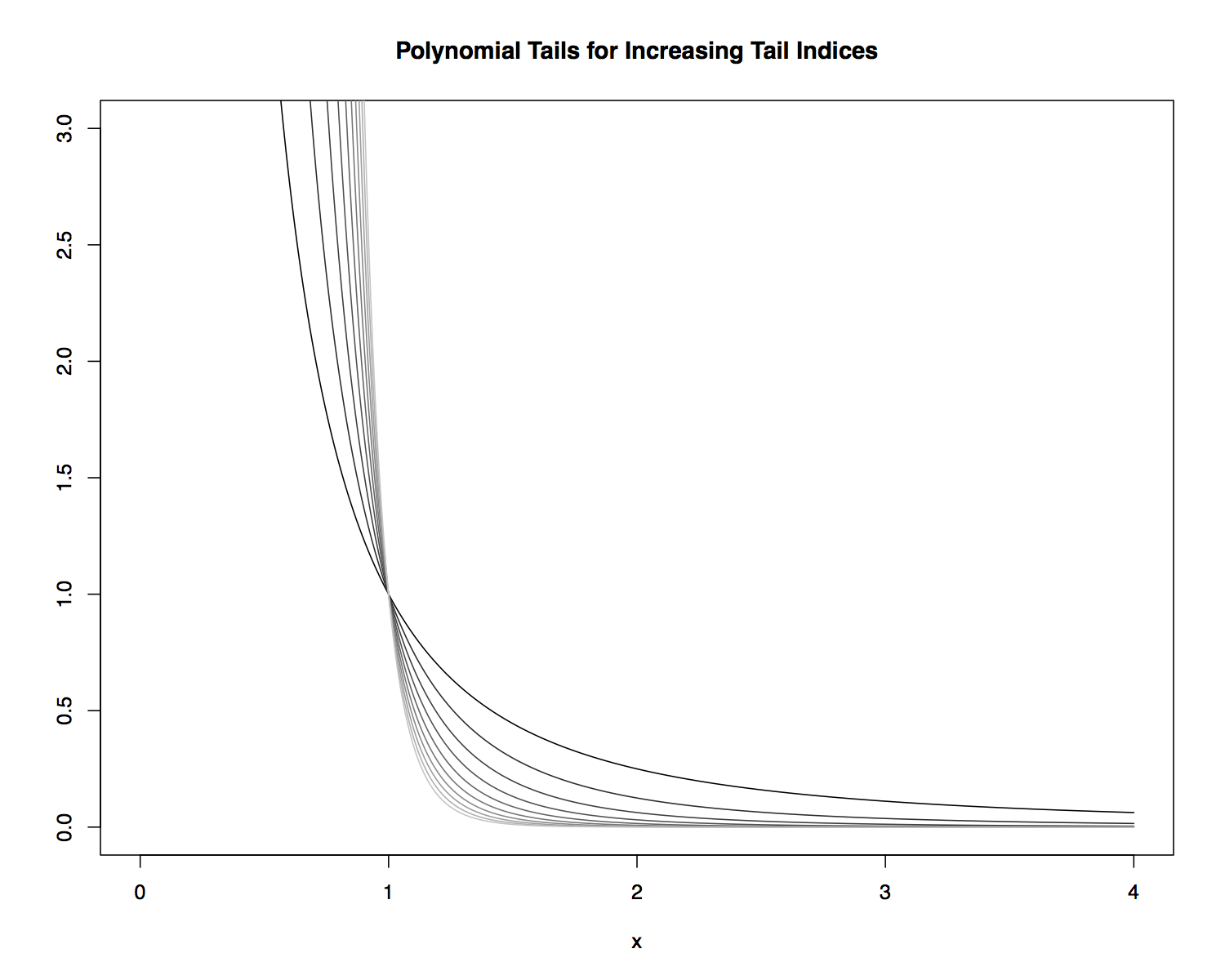

Power-Law Distributions¶

Suppose that \(X\) follows a Power-Law Distribution with shape parameter \(\alpha: \,\, X \sim PL(\alpha)\).

- Then for \(x \in (-\infty, \infty)\),

- \(A\) is chosen so that the density integrates to unity.

- \(\alpha > 0\), otherwise the density will integrate to \(\infty\).

- The power-law distribution has a polynomial tail, because the tails diminish at a polynomial rate as \(x \to \infty\) and \(x \to -\infty\).

Polynomial Tails¶

The parameter \(\alpha\) is referred to as the tail index.

- As \(x \to \infty\), \(x^{-(1+\alpha)} \to 0\) faster for larger values of \(\alpha\).

- This means that larger values of \(\alpha\) correspond to lighter tails and smaller values to heavier tails.

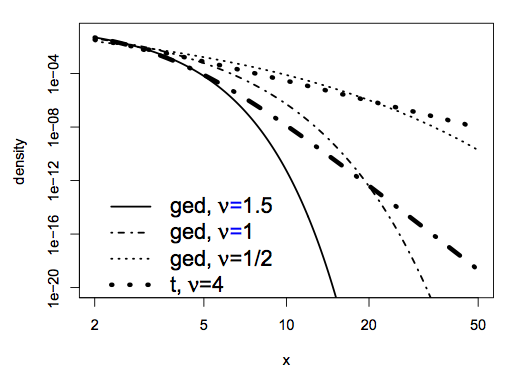

- A power-law distribution has heavier tails than a generalized error distribution:

Polynomial Tails¶

\(t\)-Distribution¶

The density of a \(t\) -distribution is

where

\(t\) -Distribution¶

Note that for large values of \(|y|\),

- This means the \(t\)-distribution has polynomial tails with tail index \(\nu\).

- Smaller values of \(\nu\) correspond to heavier tails.

Discrete Mixtures¶

Consider a distribution that is 90% \(\mathcal{N}(0,1)\) and 10% \(\mathcal{N}(0,25)\).

- Generate \(X \sim \mathcal{N}(0,1)\).

- Generate \(U \sim Unif(0,1)\), with \(U\) independent of \(X\).

- Set \(Y = X\) if \(U < 0.9\).

- Set \(Y = 5X\) if \(U \geq 0.9\).

Discrete Mixtures¶

We say that \(Y\) follows a finite or discrete normal mixture distribution.

- Roughly 90% of the time it is drawn from a \(\mathcal{N}(0,1)\).

- Roughly 10% of the time it is drawn from a \(\mathcal{N}(0,25)\).

- The individual normal distributions are called the component distributions of \(Y\).

- This random variable could be used to model a market with two regimes: low volatility and high volatility.

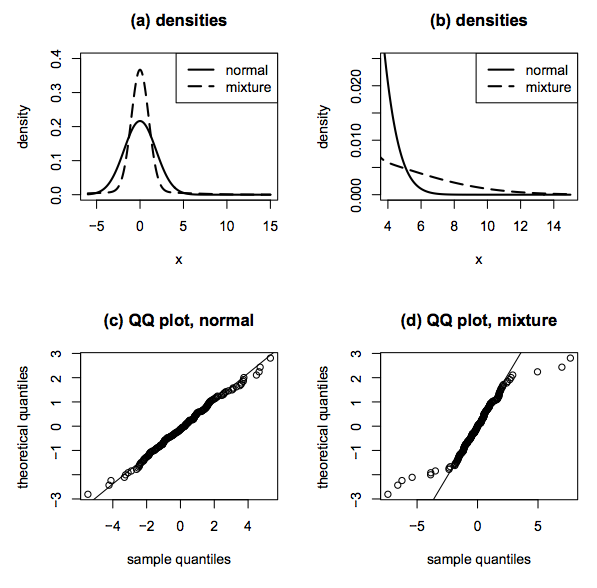

Discrete Mixtures¶

The variance of \(Y\) is

- Consider \(Z \sim \mathcal{N}(0,\sqrt{3.4}) = \mathcal{N}(0,1.84)\).

- The distributions of \(Y\) and \(Z\) are very different.

- \(f_Y\) has much heavier tails than \(f_Z\).

- For example, the probability of observing the value 6 (3.25 standard deviations from the mean) is essentially zero for \(Z\).

- However, 10% of the time, the value 6 is only 6/5 = 1.2 standard deviations from the mean for \(Y\).

Continuous Mixtures¶

In general, \(Y\) follows a normal scale mixture distribution if

where

- \(\mu\) is a constant.

- \(Z \sim \mathcal{N}(0,1)\).

- \(U\) is a positive random variable giving the variance of each normal component.

- \(Z\) and \(U\) are independent.

Continuous Mixtures¶

- If \(U\) is continuous, \(Y\) follows a continuous scale mixture distribution.

- \(f_U\) is known as the mixing distribution.

- A finite normal mixture has exponential tails.

- A continuous normal mixture can have polynomial tails if the mixing distribution has heavy enough tails.

- The \(t\) -distribution is an example of a continuous normal mixture.