Time Series Models of Volatility¶

Motivation¶

In many econometric applicaitons, model errors are heteroscedastic.

- In addition to non-constant variance, the variance of the errors may be autocorrelated through time.

- Financial time series have given rise to a rich literature in time series modeling of volatility.

- However, non-financial time series may exhibit time-varying volatility.

Motivation¶

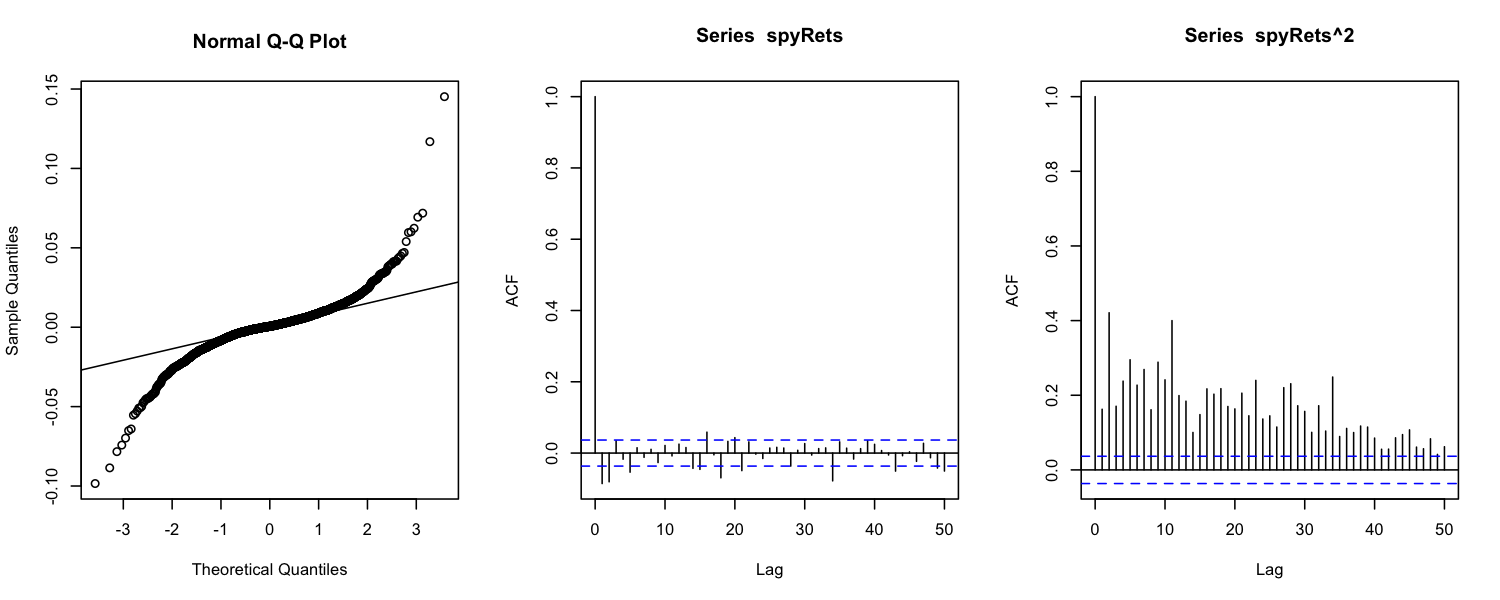

At most time scales, financial returns are known to exhibit:

- Little or no serial correlation.

- Dependence/serial correlation in the second moment.

- Heavy tails, relative to a Gaussian distribution.

Motivation¶

library(quantmod)

getSymbols('SPY')

spyRets = dailyReturn(Cl(SPY))

png(filename='spyQQACF.png',,height=4,width=10,units='in',res=150)

par(mfrow=c(1,3))

qqnorm(spyRets)

qqline(spyRets)

acf(spyRets,lag.max=50)

acf(spyRets^2,lag.max=50)

dev.off()

Motivation¶

Basic Model¶

Consider the following model

- The mean, \(\smash{\mu_t}\), may follow a linear time series process

- The variables \(\smash{\{x_{it}\}}\) are exogenous explanatory variables (e.g. the market return, for the CAPM, or dummy variables for month/week/day effects).

Basic Model¶

Time series models of volatility augment the model of the mean with a process that governs conditional volatility, \(\smash{\sigma_t}\).

- Some models specify a deterministic process for volatility (\(\smash{ARCH}\)/\(\smash{GARCH}\)).

- Others specify a random process (stochastic volatility).

The \(\smash{ARCH}\) Model¶

Engle (1982) proposed the following model for volatility

where \(\smash{\alpha_0 > 0}\) and \(\smash{\alpha_i \geq 0}\) for \(\smash{i=1,\ldots,m}\).

- Recall, \(\smash{\varepsilon_t \sim N(0,\sigma_t^2)}\).

- Alternatively, we could write \(\smash{\varepsilon_t = \sigma_t z_t}\), where \(\smash{z_t \sim N(0,1)}\).

\(\smash{ARCH}\) Order¶

Define \(\smash{\eta_t = \varepsilon_t^2 - \sigma_t^2}\).

- It can be shown that \(\smash{\{\eta_t\}}\) is an uncorrelated, zero-mean series (not necessarily i.i.d.).

- Thus the \(\smash{ARCH}\) model can be written as

- As a result, the order can be diagnosed using the tools of \(\smash{AR}\) order determination (PACF).

- This is done on the residuals, after estimating the mean equation.

Notes on \(\smash{ARCH}\)¶

- It can be shown that the \(\smash{ARCH}\) model results in excess kurthosis (relative to a Normal).

- The model parameters must be restricted in order to maintain finite unconditional variance and positive conditional variance.

\(\smash{ARCH}\) Estimation¶

Under the assumption of Normality, the conditional likelihood function is

- MLE is conducted with an interative approach:

- Compute a set of observed residuals \(\smash{\{\varepsilon_t\}}\).

- For a candidate estimate of the parameters, iteratively compute \(\smash{\{\sigma_t^2\}_{m+1}^T}\) with the variance equation and evaluate the likelihood.

- Update the parameters and repeat.

- MLE is often conducted with a \(\smash{t}\) distribution or generalized error distribution.

The \(\smash{GARCH}\) Model¶

Bollerslev (1986) proposed the following extension to the \(\smash{ARCH}\) model:

where \(\smash{\alpha_0 > 0}\), \(\smash{\alpha_i\geq 0}\), \(\smash{\beta_j\geq 0}\), and \(\smash{\sum_{i=1}^{\max(m,s)} (\alpha_i+\beta_i) < 1}\) for \(\smash{i=1,\ldots,m}\).

Notes on \(\smash{GARCH}\)¶

- \(\smash{GARCH}\) is often preferred to \(\smash{ARCH}\) because it requires far fewer parameters.

- MLE is conducted in a similar fashion, but requires an initial condition for \(\smash{\{\sigma_t\}_{m-s+1}^m}\).

- As with \(\smash{ARCH}\) models, \(\smash{GARCH}\) models feature excess kurtosis.

- Many refinements of the \(\smash{GARCH}\) model have been developed to account for asymmetry in volatility and other features.

Stochastic Volatility¶

Stochastic volatility models are an alternative to deterministic models of volatility (\(\smash{ARCH}\)/\(\smash{GARCH}\)).

- Consider the simple model of Taylor (1986):

- \(\smash{u_t}\) may be correlated with the return innovation \(\smash{\varepsilon_t}\).

Stochastic Volatility Estimation¶

The Kalman filter can be used to estimate the stochastic volatility model above.

- Consider the state-space system of Nelson (1988):

- The Kalman filter cannot be used for other, nonlinear stochastic volatility models.

- Hamilton (1989) developed a nonlinear filtering method, similar to the Kalman filter, for such problems.