Finance Preliminaries¶

Introduction¶

Our objective is to learn the theory and application of time series methods.

- We will focus on financial time series applications.

- The methods in this course are broadly applicable to any type of time series.

- We will use the R programming environment to work with financial time series data.

- The quantmod library will be especially useful:

> install.packages("quantmod")

Time Series Example¶

Let’s plot the historical prices for Facebook (FB).

> library(quantmod)

> getSymbols("FB",src="google", from="2012-01-01", to="2014-12-31")

> png(filename="fb.png")

> chartSeries(FB)

> dev.off()

Plot of Facebook Price¶

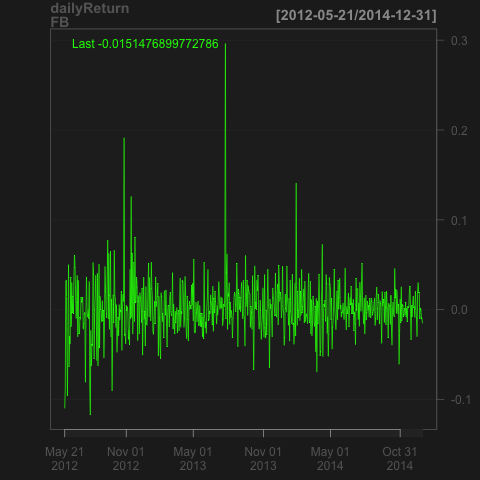

Facebook Returns¶

To plot just the closing prices:

> chartSeries(Cl(FB))

> chartSeries(FB$FB.Close)

Or daily returns:

> chartSeries(dailyReturn(Cl(FB)))

Plot of Facebook Returns¶

One-Period Return¶

Let \(P_t\) be the price of an asset at time \(t\).

- The gross return of the asset between dates \(t-1\) and \(t\) is:

- The net return is:

- Note that the return can be computed between any two dates (i.e. daily, weekly, monthly, etc).

Multi-Period Return¶

The \(k\) -period gross return between dates \(t-k\) and \(t\) is:

- The \(k\) -period net return is:

Logarithmic Approximation¶

In general, for any small value \(\smash{\varepsilon > 0}\):

Thus,

Furthermore, by the definition of gross returns,

Approximation for Multiperiod Returns¶

A similar relationship holds for the \(k\) -period net return:

Time Intervals¶

The interval of time for returns is of vital importance for understanding the data.

- Daily returns are very different from weekly, monthly, annual, etc. returns.

- Intra-day returns at various time scales (millisecond, second, minute) are very different from each other.

Aggregating Trading Intervals¶

When aggregating returns, we consider the following.

- There are approximately 250 trading days in a year.

- There are approximately 22 trading days in a month.

- There are 5 trading days in a week.

- U.S. equities markets are open from 9:30 am to 4:00 pm Eastern time - 6.5 hours each day.

- Thus there are approximately 6.5 hours, or 390 minutes or 23,400 seconds or 23,400,000 milliseconds in a trading day.

- Similarly, there are approximately 1625 trading hours, 97,500 trading minutes, 5,850,000 trading seconds and 5,850,000,000 trading milliseconds in a year.

Aggregating Returns¶

To aggregate net returns, we simply add them:

For example, to annualize daily returns,

Example of Aggregating Returns¶

Get Exxon Mobile equities data for the week of March 23rd, 2015.

> getSymbols("XOM", from="2015-03-23", to="2015-03-27")

[1] "XOM"

> XOM

XOM.Open XOM.High XOM.Low XOM.Close XOM.Volume XOM.Adjusted

2015-03-23 85.02 85.78 85.01 85.43 17163200 85.43

2015-03-24 85.30 85.78 84.50 84.52 10099500 84.52

2015-03-25 85.05 85.57 84.77 84.86 11816000 84.86

2015-03-26 85.30 85.57 84.09 84.32 14388500 84.32

2015-03-27 84.04 84.05 83.33 83.58 11094600 83.58

- What are the daily returns?

- What is the weekly return?

Asset Classes¶

There are several broad classes of assets traded in financial markets.

- Equities.

- Futures.

- Options.

- Bonds.

- Currencies.

Indices¶

Indices are synthetic portfolios of assets that are not typically traded.

- The S&P 500 index is a portfolio of 500 equities and is not traded.

- To hold the S&P 500 index, one can:

- Purchase the 500 component equities in the correct proportions.

- Purchase shares in a mutual fund that tracks the index.

- Purchase shares of the SPY exchange traded fund (ETF).

- Purchase futures contracts on SPX.

Important Indices¶

- S&P 500 (SPX).

- VIX - portfolio of S&P 500 options which represents the expected value of a one-standard deviation move in the S&P 500 index over the next month (in annual terms).

- On March 30th, 2015, the closing value for VIX was 14.51 and the closing value for SPX 2086.24.

- Hence, the market expects the standard deviation of the SPX to be \(14.51/\sqrt{12} = 4.19\) percent or \(\smash{0.0419\times 2086.24 = 87.39}\) index points.

Important Assets¶

- SPY - SPX ETF.

- E-mini - Futures contract on the SPX.

- SPX Options.

- SPY Options.

- VIX Options.

- VIX Futures.

Near-Month VX Futures¶

> install.packages("Quandl")

> library(Quandl)

> VX1 = Quandl("OFDP/FUTURE_VX1",type="xts")

> chartSeries(VX1)

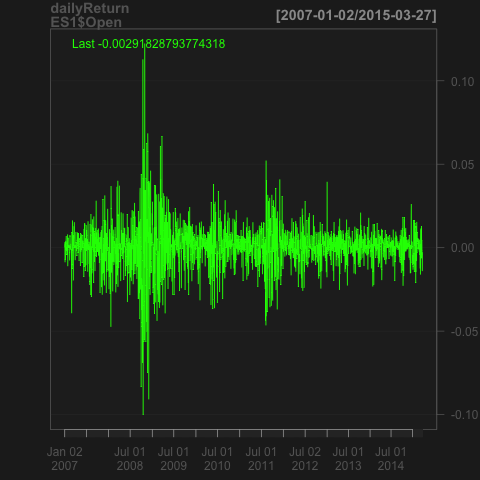

E-mini Near-Month Returns¶

> ES1 = Quandl("OFDP/FUTURE_ES1",start_date="2007-01-01",end_date="2015-03-27",type="xts")

> chartSeries(dailyReturn(ES1$Open))

Important Features of Returns¶

What do you notice about the E-mini returns?