Moving Average Processes¶

\(MA(1)\)¶

Given white noise \(\{\varepsilon_t\}\), consider the process

where \(\mu\) and \(\theta\) are constants.

- This is a first-order moving average or \(MA(1)\) process.

\(MA(1)\) Mean and Variance¶

The mean of the first-order moving average process is

\(MA(1)\) Autocovariances¶

\(MA(1)\) Autocovariances¶

- If \(j = 0\)

- If \(j = 1\)

- If \(j > 1\), all of the expectations are zero:

\(MA(1)\) Stationarity¶

Since the mean and autocovariances are independent of time, an \(MA(1)\) is weakly stationary.

- This is true for all values of \(\theta\).

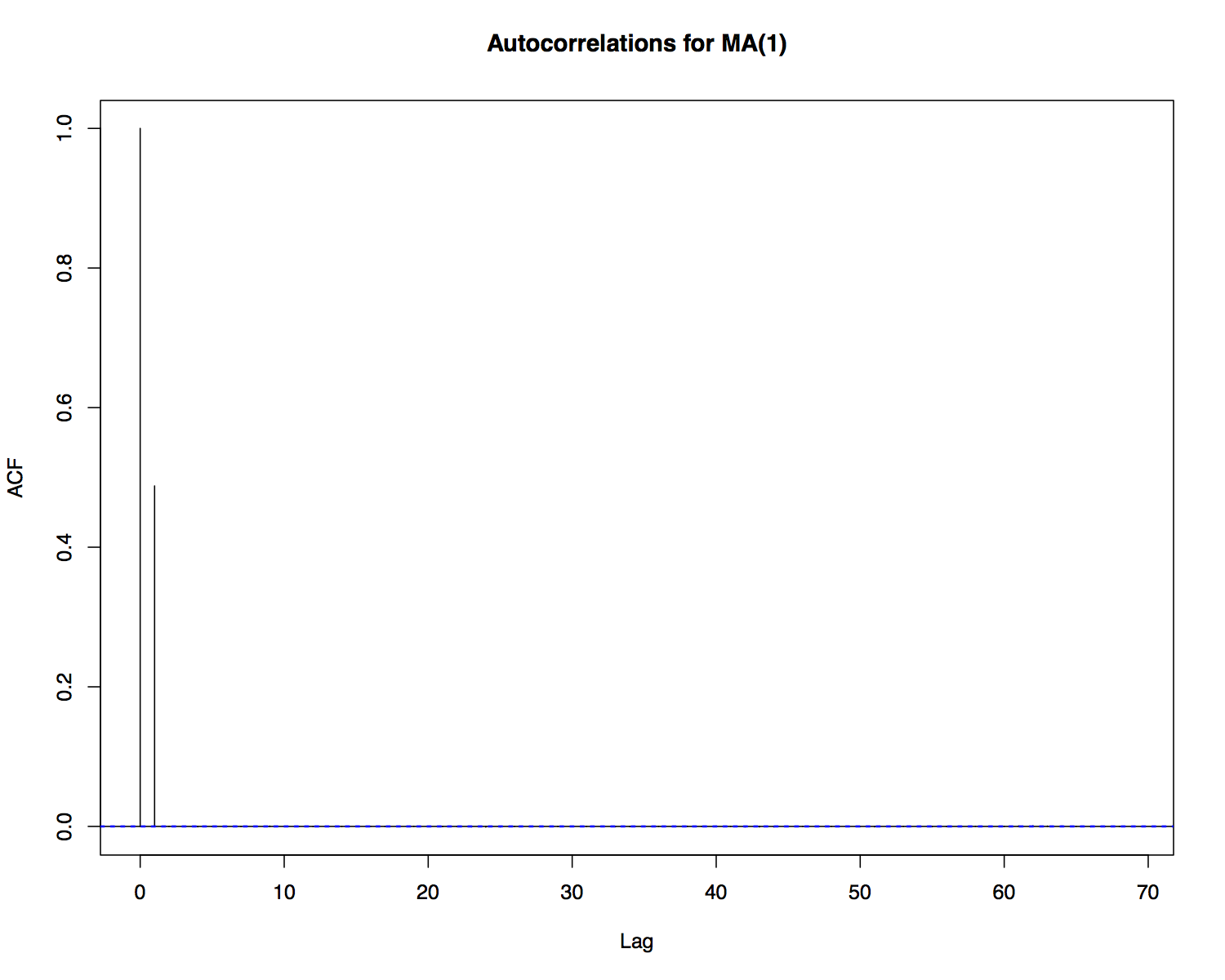

\(MA(1)\) Autocorrelations¶

The autocorrelations of an \(MA(1)\) are

- \(j = 0\): \(\hspace{0.7in} \rho_0 = 1\) (always).

- \(j = 1\):

- \(j > 1\): \(\hspace{0.72in} \rho_j = 0\).

- If \(\theta > 0\), first-order lags of \(Y_t\) are positively autocorrelated.

- If \(\theta < 0\), first-order lags of \(Y_t\) are negatively autocorrelated.

\(MA(1)\) Autocorrelations¶

\(MA(q)\)¶

A \(q\) th-order moving average or \(MA(q)\) process is

where \(\mu, \theta_1, \ldots, \theta_q\) are any real numbers.

\(MA(q)\) Mean¶

As with the \(MA(1)\):

\(MA(q)\) Autocovariances¶

- For \(j > q\), all of the products result in zero expectations: \(\gamma_j = 0\), for \(j > q\).

\(MA(q)\) Autocovariances¶

- For \(j = 0\), the squared terms result in nonzero expectations, while the cross products lead to zero expectations:

\(MA(q)\) Autocovariances¶

- For \(j = \{1,2,\ldots,q\}\), the nonzero expectation terms are

The autocovariances can be stated concisely as

where \(\theta_0 = 1\).

\(MA(q)\) Autocorrelations¶

The autocorrelations can be stated concisely as

where \(\theta_0 = 1\).

\(MA(2)\) Example¶

For an \(MA(2)\) process

Estimating \(MA\) Models¶

Estimation of an \(MA\) model is done via maximum likelihood.

- For an \(MA(q)\) model, one would first specify a joint likelihood for the parameters \(\{\theta_1, \ldots, \theta_q, \mu, \sigma^2\}\).

- Taking derivatives of the log likelihood with respect to each of the parameters would result in a system of equations that could be solved for the MLEs: \(\{\hat{\theta}_1, \ldots, \hat{\theta}_q, \hat{\mu}, \hat{\sigma}^2\}\).

- The exact likelihood is a bit cumbersome and maximization requires specialized numerical methods.

- The MLEs can be obtained with the \(\mathtt{arima}\) function in \(\mathtt{R}\).

Which \(MA\)?¶

How do we know if an \(MA\) model is appropriate and which \(MA\) model to fit?

- For an \(MA(q)\), we know that \(\gamma_j = 0\) for \(j > q\).

- We should only fit an \(MA\) model if the autocorrelations drop to zero for all \(j > q\) for some value \(q\).

- The \(\mathtt{acf}\) function in \(\mathtt{R}\) can be used to compute empirical autocorrelations of the data.

- The appropriate \(q\) can then be obtained from the empirical ACF.

Which \(MA\)?¶

- After fitting an \(MA\) model, we can examine the residuals.

- The \(\mathtt{acf}\) function can be used to compute empirical autocorrelations of the residuals.

- If the residuals are autocorrelated, the model is not a good fit. Consider changing the order of the \(MA\) or using another model.

Which \(MA\)?¶

The \(\mathtt{auto.arima}\) function in \(\mathtt{R}\) estimates a range of \(MA(q)\) models and selects the one with the best fit.

- \(\mathtt{auto.arima}\) uses the Akaike Information Criterion (AIC) or the Bayesian Information Criterion (BIC) to select the model.

- Minimizing AIC and BIC amounts to minimizing the sum of squared residuals, with a penalty term that is related to the number of model parameters.